.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

In my role as a data scientist focused on payments, I often hear from merchants with questions about their transaction success rates. Sometimes these questions are from customers — and often they are from other merchants that aren’t yet clients.

I recently heard from an Australian merchant that is not currently a Spreedly customer. He was experiencing extremely high decline rates of credit cards. As a result, his company was losing revenue. They were frustrated at not being able to resolve the issue which had put the entire business at risk. While his company’s issue with declines was not a payment gateway problem, nevertheless, it encouraged me to take a closer look at the payment infrastructure in the land down under.

As part of this analysis, I was curious to learn the number of gateways handling domestic and international transactions in AUD currency, whether decline rates differ among them, the average latency, brands and popular brands and banks among card holders that transact in AUD.

Gathering Data

Spreedly supports virtually any payment service, including more than one hundred gateways. We often see that different services have different latencies, success rates, and other metrics. We process over $10B in annualized transactions, so we have lots of data on transaction successes. And because our customers often use Spreedly to expand their international presence, we have excellent data around the world. Therefore what I needed to do was to look into Spreedly transactions data in AUD currency in the past 6 months.

To determine if a transaction is international or domestic, I compare the transaction’s currency with the payment card’s country of issuance currency. When the two match, it is domestic. Otherwise, it is international.

The country associated with the card is found via the BIN (Bank Identification Number) database and I use DataHub for the country-currency data. One issue that may arise here is that, sometimes multiple countries use the same currency. According to DataHub’s country-currency code, Cocos Island, Nauru and several more use AUD as their main currency, therefore any transactions between these countries in AUD is counted as domestic. In our case, this is not a huge issue since the ratio of transactions made by these countries are relatively small.

Brands & Expiration Dates

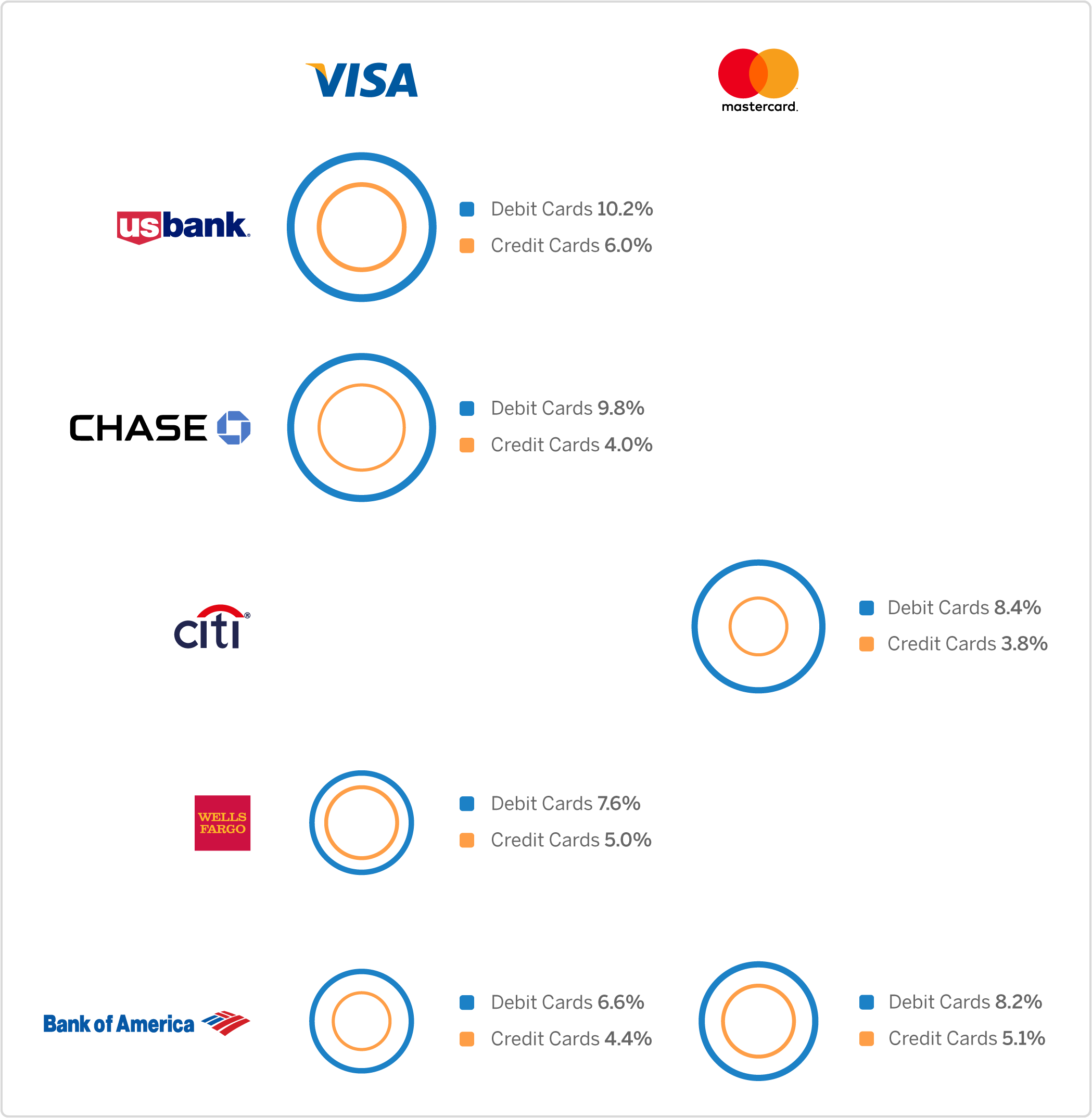

The hundreds of thousands of transactions analyzed in this study were handled by 30 gateways. 96% of these transactions are domestic and only 4% are international. Visa (55%) and MasterCard (34%) are the major card brand players. American Express made only 2% of cards in our data selection. Other brands did not make a significant contribution cumulatively (below 1%).

50% of the analyzed transactions are below A$75 (~ $50 USD) and 90% of them were below A$500 (~ $355 USD). Top 5 countries where the card belonged to after Australia are US, UK, New Zealand, Singapore and Canada.

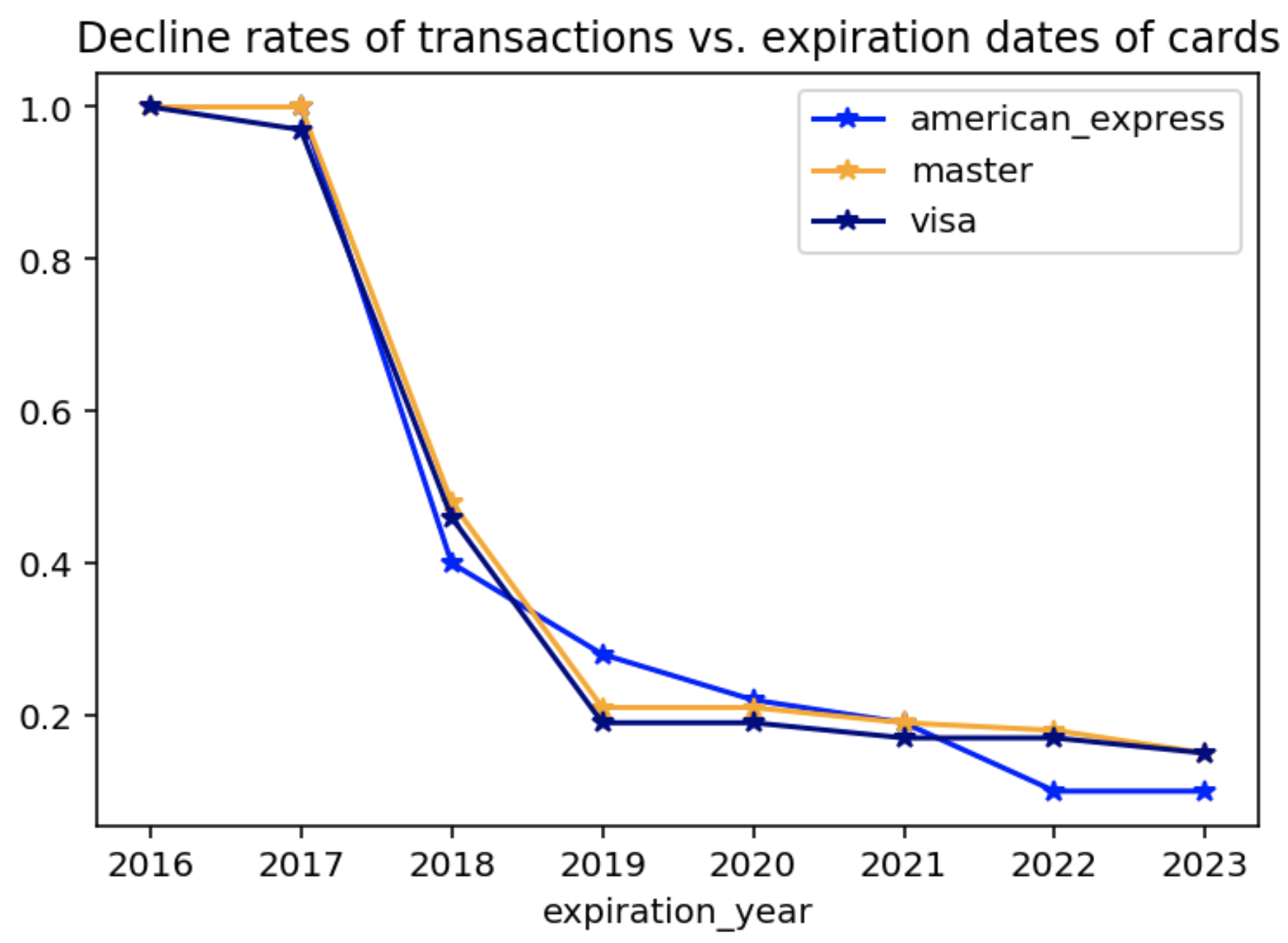

Not surprisingly, expired cards are not welcome in Australia; 97% of transactions via expired cards, with expiration dates back to 2017, were declined. For cards expired in 2018, the decline ratio among brands dropped to around 50%. The ratio of declines for 2019 cards is 21% (American Express), 21% (MasterCard) and 18% (Visa). The rate for other years has been similar to 2019.

Considering the fact that an expired card plays a vital role in success or decline of transactions made by it, merchants need to equip themselves with Account Updater (AU), a service provided by card brands to automatically keep the credit card account information up to date. In a separate blog post, I discussed how AU has helped merchants lower their decline rates.

Countries & Banks

Commonwealth Bank of Australia, Australia & New Zealand Banking Group, Westpac Banking Corporation and National Australia Bank are the major card issuers among the cards we investigated. Citi is the only international bank with a major number of issued cards.

After Australia, most of the cards belong to the United States, United Kingdom, New Zealand and Singapore. Though there are not more than a couple of hundreds of transactions from Russia, 67% of them are declines. The other highest decline rates belong to Panama and Thailand. US and UK and Canadian transactions experience reasonable 18-20% declines.

International vs. Domestic

29 gateways handled domestic and 27 gateways handled international transactions in AUD. For gateways with a substantial number of transactions in AUD, the lowest observed decline rate is 7% and the highest is 95%! These numbers for international transactions are 17% and 73% respectively.

Gateways Performance Comparison - Declines

As mentioned above, 29 and 27 gateways process transaction in AUD domestically and internationally, respectively. While 8 gateways handle the larger portion of the domestic transactions, 3-4 gateways are more popular for processing international transactions. Stripe, Payment Express and Qvalent are among the popular ones for both domestic and international.

Declines for domestic transactions ranges from the unusual rate of 95% down to 7%. The extreme case of 95% can be due to many causes including technical difficulties, lack of funds or fraudulent activities. On the other hand, the bottom range of 7% is very acceptable and compares with the decline rates for the best gateways in USD.

Decline rates for international transactions in AUD range from 85% to 11%. While for some gateways, the decline ratio for domestic vs. international varies significantly, there are some other gateways that show a prominent performance in both categories.

The following plot shows the monthly decline rate across two gateways that serve Australia. The two gateways transact in many countries and are among top go-to gateways in many currencies. While the declines across the orange gateway is very reasonably low, the declines for transactions through the blue gateway is unreasonably high. In the meantime, we need to emphasize that declines occur due to many reasons, and gateways are only one part of the Card-Not-Present payment processing.

Gateways Performance Comparison - Latency

Latency, defined in our terms as the time interval between submitting a transaction to a gateway and hearing back from them, is a metric we measure and monitor at Spreedly. It also takes into account the time it takes for the payment processor to handle the transaction and respond to the gateway.

Latency becomes important when, for instance, a ticketing organization submits tens or sometimes hundreds of thousands of transactions in a short time interval. Shorter latencies lead to faster handling of the payment and less traffic on the website. On the other hand, latencies can differentiate gateways with regards to the payment optimization.

One interesting observation is that, on average, successful transactions take more time to process! This is the case for both international and domestic transactions. For domestic (international), we noticed that successful ones take about 200 (400) milli-seconds (ms) more. Based on this piece of information, we might be able to infer where (gateway, or card processor) a transaction is declined, by comparing their latencies.

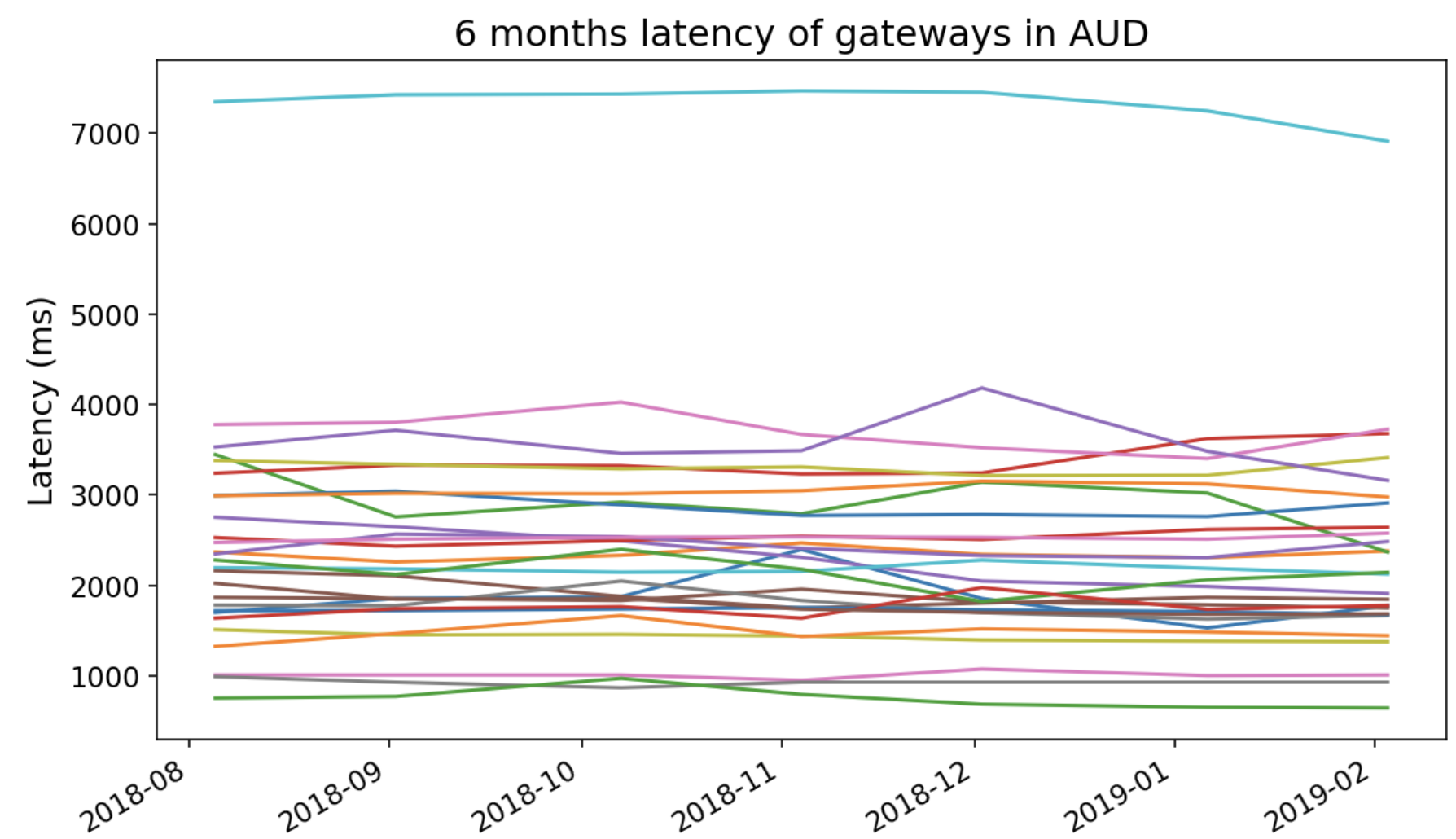

I have plotted the 6 months data latencies for successful AUD transactions per gateways. From this plot, three categories of gateways can be identified. The first one of the group of gateways that process AUD payments around of below one second. 3 gateways are in this category.

The second category, where latency varies between 1.5 to 4 seconds, comprises most of the gateways. While most of the time gateways demonstrate a consistent behavior, the observation of spikes among some of them is common, leading to temporary increase or improvement in their latencies.

And the third category has only one member that processes payments in 7+ seconds. Comparing this gateway with the best-performing ones shows it takes this gateway 7 times longer to process a payment. Customers and merchants using this gateway should be more patient than the others.

In this short post, we looked at our past 6 months of transactions in Australian Currency to learn more about domestic and international payments processed in AUD. Our findings, illustrated in the last two tables, clearly demonstrate that some payment gateways outperform the others when it comes to decline rates and the time it takes to process transactions. A wise choice of using multiple gateways along with using services such as Account Updater can lead to a smooth payment experience on the one hand, and increasing customer satisfaction on the other.

Download the Multiple Payment Gateways eBook Below