.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Your fraud rate is falling, your chargeback numbers look reasonable, and somewhere in a quarterly business review, someone is about to put a green checkmark next to fraud prevention.

Meanwhile, your authorization rate has quietly dropped two percentage points, a segment of your most loyal customers have not returned since their last declined transaction, and your engineering team is managing three separate fraud integrations that do not talk to each other.

The green checkmark is technically accurate. The picture it represents is not. Payment fraud analytics that only measures the fraud it stopped is counting the wrong thing.

Merchants lose as much as $448 billion annually to payment fraud, false declines, and returns and refund abuse, and that number only makes sense when you account for both sides of the ledger. Most fraud teams are only watching one.

Is your fraud rate actually telling you anything useful?

A fraud rate tells you the outcome, not the combination of routing decisions, filter configurations, customer behaviors, and issuer risk models that produced it. A team can tighten fraud rules, watch the fraud rate fall, and be completely blind to the fact that their overly aggressive filters are now declining legitimate customers at a cost that exceeds the fraud they stopped.

As Spreedly's own payment analytics research puts it: if a fraud strategy is tuned for safety over precision, you can improve the fraud rate while making real revenue worse. You can win the fraud metric and lose the customer.

Decline codes make this worse, because they tell you the category of the failure, not the cause. They originate from issuers, processors, and networks, which makes them accurate labels for reasons that are rarely actionable on their own. A team treating decline codes as its primary diagnostic layer is doing autopsy work on patients it could have saved.

The outcome of payment fraud analytics is not the dashboard. It is the decisions your team makes with that information, and decisions made without the full picture produce outcomes that look like success until the revenue report arrives.

The two costs that never appear on the same report

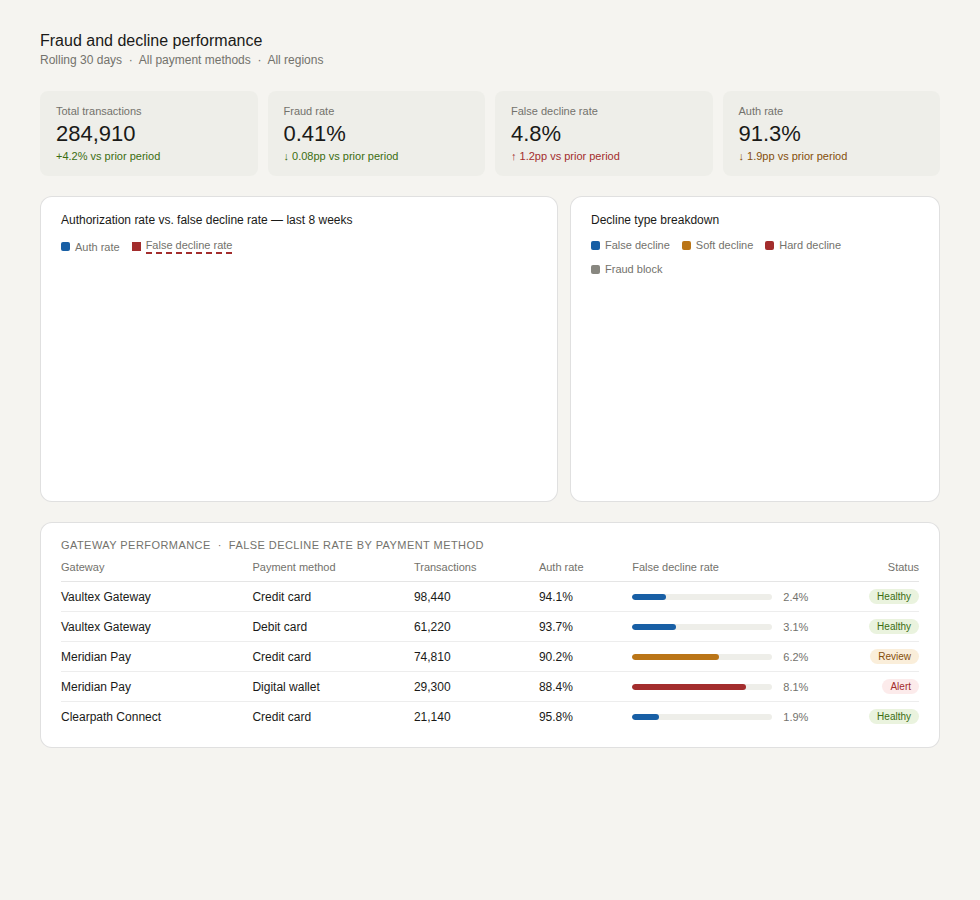

Most fraud teams are optimizing for one side of a two-sided equation. Actual fraud losses are visible, tracked, and reported. Chargeback rates go into reviews. Fraud incidents trigger post-mortems. The other cost, the one that does not show up in fraud reporting at all, is the revenue that walked out the door because your fraud system held it open for the wrong reason.

Nearly half of merchants estimate that up to 5% of legitimate orders are wrongly declined as fraudulent, representing an estimated $50 billion in lost revenue industrywide. Global false decline losses are estimated to have exceeded $443 billion, which is, according to Aite-Novarica data cited by Riskified, nearly nine times larger than projected fraud losses from actual ecommerce credit card fraud in the same period.

The fraud system is generating more revenue damage than the fraud itself, and that damage doesn’t show up as a fraud loss. It shows up as silence: an abandoned cart, a lapsed subscriber, a customer who completed the same purchase with a competitor 20 minutes later.

Your fraud dashboard looks clean while your revenue dashboard bleeds quietly in the next tab.

What does a false decline actually cost a merchant?

The industry has spent years treating false declines as a conversion problem, which significantly undersells the damage. According to Signifyd analysis, after a false decline, 27% of customers do not return at all, and those who do return place 65% fewer orders with a 16% drop in average order value. For loyal customers who had already proven their value by purchasing three or more times, the impact is even more pronounced.

Among customers who experienced a decline, 57% were repeat buyers, people whose purchase history had already established their legitimacy before the fraud filter fired anyway. And 42% of declined customers abandon the cart entirely rather than try again with the same merchant. A merchant who spent to acquire a customer, converted them, retained them through two more purchases, and then lost them to a fraud filter that fired incorrectly has not just lost a transaction.

The entire value of that customer relationship, built carefully over multiple purchases, evaporated at the moment of highest return. Calling that a fraud prevention cost is generous. Calling it a design failure is closer to accurate.

Why payment fraud analytics misses all of this

The structural reason most fraud reporting produces an incomplete picture is that fraud analytics and payment analytics sit in different systems, managed by different teams, accountable to different metrics. When fraud tools and payment orchestration platforms report to separate dashboards, there is no native way to correlate fraud filter decisions with authorization rate outcomes. A fraud tool can show zero fraud incidents while the payments platform shows a steady decline in approval rates, and without combining those data streams, no one makes the connection.

The Spreedly State of Checkout 2025 found that 36% of merchants added redundant fraud tools to counter provider outages, a finding that points not to intelligence but to fragmentation. Every separately integrated tool adds another data stream that does not communicate with the others.

Payment method abandonment compounds this further, because when a customer's preferred payment method is unavailable or fails silently, that drop-off does not register as a decline at all. It registers as nothing, and the checkout looks fine while a real customer disappears.

AI anomaly detection research from payments analytics specialists highlights the same structural blind spot: your aggregate authorization rate can look stable while a specific fraud rule quietly destroys approvals for a card segment in a particular market. Without granular, correlated analytics, small deviations compound into material revenue leakage before anyone notices them.

What payment fraud analytics should actually measure

The first thing to measure is the false positive rate, with the same rigor applied to the fraud rate. Most fraud teams are accountable for the fraud metric and nobody owns the false decline metric. That ownership gap is where the hidden cost hides. A fraud tool that reduces chargebacks by 10% while increasing false declines by 15% is a net revenue loss, and it will never appear that way in a single-metric view.

Authorization rate correlated with fraud tool configuration is the second critical layer. If fraud checks run pre-authorization, teams should be able to see directly how authorization rates shift when specific fraud rules change, segmented by geography, card type, and transaction amount.

Tightening a rule in one market may improve the fraud rate while depressing authorization rates in a customer segment that generates disproportionate lifetime value, and without that correlation layer, teams are adjusting controls without knowing what else they are turning off.

Customer journey signals, rather than transaction signals alone, represent the third layer that most analytics stacks are missing. Spreedly's fraud prevention platform provides behavioral data across the full customer session, from browsing behavior and account creation patterns through to device signals and purchase history.

A synthetic identity and a loyal returning customer can look identical at the moment of transaction. Across a session, they do not look identical at all, and that distinction is where accurate fraud decisioning lives.

Gateway and route-level performance segmented by fraud outcomes rounds out the picture. When transactions route dynamically across gateways, fraud outcomes vary by provider, region, and payment method. Analytics that does not segment false decline rates by routing path will obscure performance differences that translate directly into recoverable revenue.

Three questions worth asking your payment and fraud teams right now

Each of these points to a gap in how most fraud and payments teams currently operate, and each one has real revenue implications.

Can you correlate a change in your fraud tool configuration to a change in your authorization rate within the same reporting view? If answering that question requires pulling data from two systems and reconciling them manually, the hidden cost is actively accumulating in the gap between those two spreadsheets.

Do you know your false positive rate, and does it live in the same report as your fraud rate? If the fraud team is only accountable for the fraud metric, the revenue damage from false declines has no owner and no structural incentive to be fixed. That metric needs an owner before it will move.

Does your analytics layer include pre-transaction customer journey data? If fraud decisions are made using only transaction-level signals, the behavioral patterns that would identify fraud earlier in the session, and protect legitimate customers from misidentification, are invisible to your detection models entirely.

The cost of fighting the wrong fraud

The hidden cost of fighting the wrong fraud is not just the false declines themselves. It is every decision made without the data to distinguish a fraudster from a loyal customer with an unusual shipping address.

Merchants who treat fraud prevention as a single-metric discipline will keep winning the fraud rate and losing the customer, and the ones who close the gap between fraud analytics and payment performance data will find that the revenue they thought they were protecting was never in as much danger as the revenue they were quietly turning away.

Get The Complete Guide to Payments Orchestration

Payments orchestration gives you a single control layer to connect providers, optimize performance, and scale into new markets without rebuilding your payments stack. This guide breaks down what orchestration is, how implementation works, and where it drives measurable impact across approvals, costs, compliance, and customer experience.

Download the White Paper here >>

What is a false decline in payment fraud?

A false decline occurs when a legitimate transaction is rejected by a fraud filter that misidentifies a real customer as a bad actor. Unlike actual fraud losses, false declines don't show up in fraud reports. They show up as abandoned carts, lapsed subscribers, and customers who complete the same purchase with a competitor. Research from Signifyd found that 27% of customers who experience a false decline never return to that merchant.

Why do fraud analytics miss false declines?

Most fraud tools and payment orchestration platforms report to separate dashboards, managed by separate teams, accountable to separate metrics. Without combining those data streams, a fraud tool can show zero fraud incidents while authorization rates quietly fall. The gap between those two systems is exactly where false decline costs accumulate without anyone owning them.

How should merchants measure fraud prevention effectiveness?

Effective payment fraud analytics measures the false positive rate with the same rigor applied to the fraud rate. Authorization rate should be correlated directly with fraud tool configuration, segmented by geography, card type, and transaction amount. Customer journey signals, not just transaction-level signals, should feed fraud decisions. And gateway-level performance should be segmented by fraud outcomes to surface recoverable revenue that aggregate reporting obscures.