.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Do you know which payment methods your customers want access to most?

Alternative payment methods (APMs) and local payment methods (LMPs) have grown immensely in recent years, largely due to the increasing use and global availability of e-commerce.

One recent EY survey reveals that more than 85% of merchants plan to increase their acceptance of APMs in the next one to three years. Meanwhile, LPMs continue to gain regional traction, especially within geographic locations where access to traditional banking is limited.

As you build and expand your business, considering which APMs and LPMs to add to your payment mix is crucial for growth. However, these terms are often used interchangeably, leading to confusion about which type of payment methods you need and which your customers prefer.

To reduce this confusion, let’s define APMs and LPMs, and discuss how they impact your business.

What is an APM?

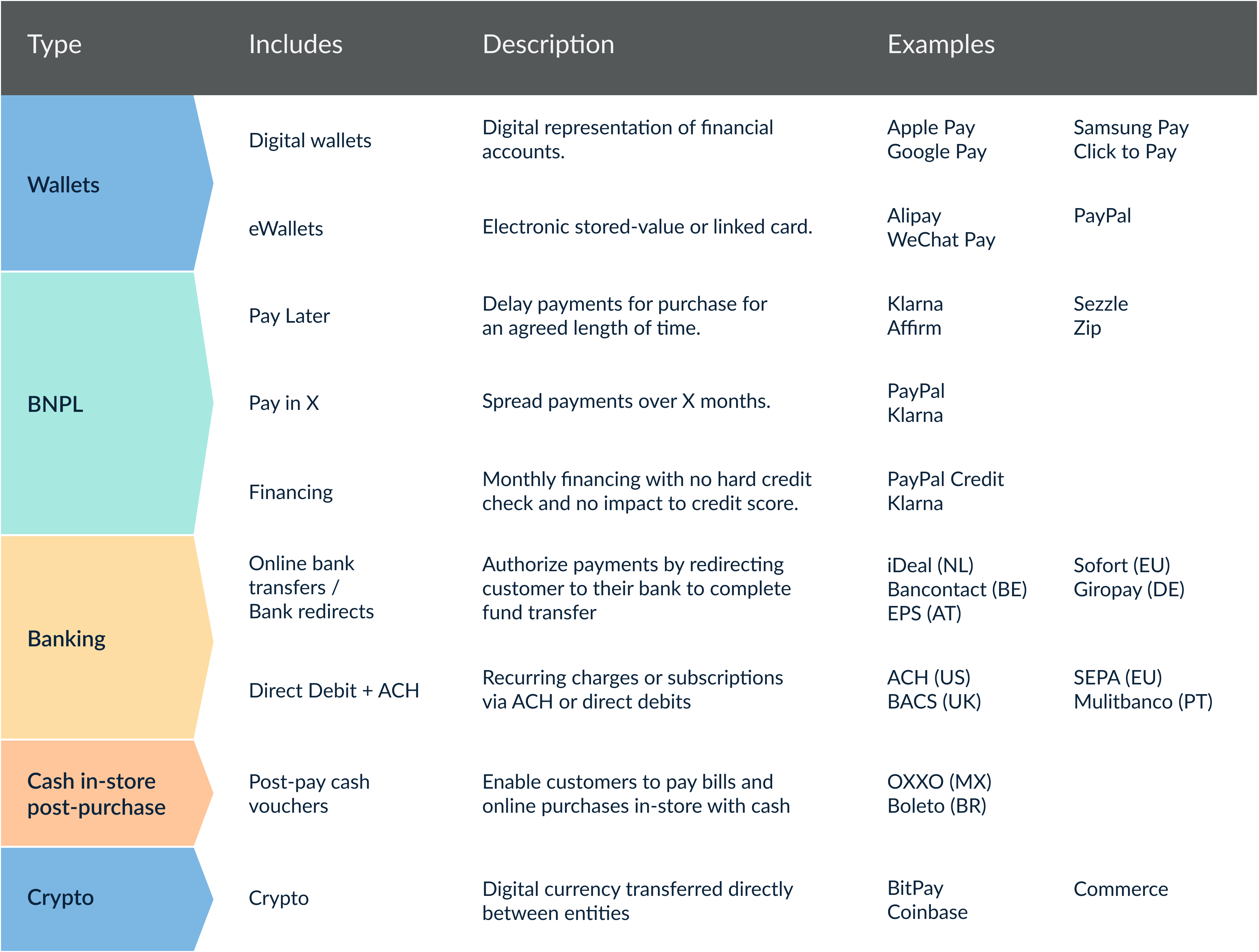

An alternative payment method, or APM for short, is a payment method that does not involve traditional cash or card transactions. APMs can take many forms, from digital wallets to installment loans (commonly known as Buy Now, Pay Later loans).

- Account-to-account (A2A) payments

- Direct bank transfers

- Cash voucher payments

- Cryptocurrency

As e-commerce and online shopping have grown in popularity, APMs have risen to prominence. One of the major advantages of APMs is that they allow your business to connect with more customers around the world by enabling customers to select from a wider range of payment methods.

Although the term “alternative payment methods” suggests there is a generally agreed-upon definition of what standard payment methods are. However, these standard viewpoints have grown immensely outdated in recent years, failing to take into account the development of digital payment technologies and localized payment methods designed for use in specific regions of the world.

As a result, failing to enable alternative payment methods can not only hinder your business’s growth but also demonstrate a lack of understanding of future markets you plan to expand into.

What is an LPM?

A local payment method, or LPM for short, is a payment available only within specific regions.

While the term “alternative payment methods” suggests there is an agreed-upon, or “correct” point of view as to what standard payment methods are, this is simply not the case, and can be construed as lacking understanding of your intended market.

LPMs account for the merchant and customer locale, giving equal weight and credibility to the regional approach to online payments. Engaging with customers in different regions requires an understanding of what payment methods are trusted and how the consumer interacts with online payments, as they may be significantly different from customer preferences in your home region.

Many local payment methods offer lower costs to merchants, making cost efficiency a major factor and advantage to consider when enabling LPMs. Popular examples of LPMs include:

- iDeal: The Netherlands’ iDeal is a bank redirect and account-to-account payment method available specifically within the Netherlands, accounting for over 55% of all online transactions. Entering the NL market without this payment method would be a major mistake as a merchant.

- OXXO: In Mexico, only around 37% of adults have bank accounts, creating a clear need for alternative payment methods that side-step traditional banking channels. OXXO, a Mexican convenience store chain, offers payment vouchers that can be used to pay bills online and make online purchases in-store with cash — no card or bank account required.

- PIX: Brazil has pushed forward with PIX, a countrywide and mandated initiative for instant payments for account-to-account transfers, leading to a shift in the Brazilian market of online payments. As a whole, PIX aims to lower financial costs, increase security, improve customer experiences, increase market competition, and expand financial inclusion.

Looking to add an APM or LPM to your payment stack? Get in touch with Spreedly today.

How Geographic Location Impacts Your APM & LPM Strategy

Both APMs and LPMs have a role to play in the global expansion of your business.

If you are based in the U.S. or UK, payment methods in Latin America or Eastern Europe may be largely unfamiliar to you. In turn, you may believe it is unnecessary to enable such payment methods.

Yet, if your payment strategy doesn’t include consideration for how locals want to make purchases, your expansion will likely be hindered by your lack of payment methods. Even customers in your home region may be experiencing changes to their payment preferences, making it a necessity to consider which alternative payment methods may be overtaking traditional cash and card payments in your home region.

In a 2021 PaymentsFN presentation, Spreedly’s Peter Mollins sat down with Pete Kovacs, a senior product manager at HBO Max. Kovacs remarks on the crucial importance of considering the needs of local customers when launching payments in new markets and measuring the success of payments.

Once you understand the significance of enabling APMs and LPMs, the next key task is determining how to facilitate these payment methods within your payment system.

To do so, you must start by integrating multiple payment gateways.

Why You Need Multiple Payment Gateways to Enable APMs & LPMs

Integrating multiple payment gateways can be either an immensely difficult or incredibly simple task — it all comes down to the optimization of your payment stack.

Here at Spreedly, we believe payment orchestration to be the key to integrating multiple payment gateways with ease. A payments orchestration layer can facilitate your management of APMs and LPMs, all while providing a broader set of global payment options and services that will best suit your business model and the regions in which you operate.

Choosing your payment gateways wisely is arguably equally important to researching which payment methods your customers demand most. By selecting and integrating the right payment gateways for your business, you can optimize your payment system by ensuring higher transaction approvals and streamlining the payment experience.

As such, you need a payment infrastructure capable of leveraging payment gateway products from multiple vendors, allowing you to enable payment methods based on tailored geographic requirements.

Spreedly Helps You Enable APMs and LPMs with Ease

Through our single point of integration, Spreedly provides you with the capability to easily integrate multiple payment gateways in your payment infrastructure. This capability, along with Spreedly’s wealth of payment expertise and resources, helps you expand your business effectively by taking into account the many different payment needs and preferences of your target customers.

Contact Spreedly today to get started with our payment orchestration platform.

Download the Payments Orchestration eBook Below

What is an Alternative Payment Method (APM)?

An Alternative Payment Method (APM) is a payment method that does not involve traditional cash or card transactions. APMs include digital wallets, Buy Now Pay Later loans, account-to-account (A2A) payments, direct bank transfers, cash voucher payments, and cryptocurrency. APMs have risen in prominence with the growth of e-commerce and allow businesses to connect with more customers worldwide by offering a wider range of payment options.

What is a Local Payment Method (LPM)?

A Local Payment Method (LPM) is a payment method available only within specific regions. LPMs account for the merchant and customer locale and give credibility to the regional approach to online payments. Understanding LPMs is crucial because consumer preferences and trusted payment methods can vary significantly between regions, and many local payment methods offer lower costs to merchants.

Why should merchants consider adding APMs and LPMs to their payment mix?

According to an EY survey, more than 85% of merchants plan to increase their acceptance of APMs in the next one to three years. Adding APMs and LPMs is crucial for business growth because it demonstrates understanding of future markets, enables access to customers in different regions where traditional banking may be limited, and prevents hindering your business's expansion by failing to offer payment methods your customers prefer and trust.