.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Merchant payment providers grow more numerous and sophisticated each year - while services self-identifying as “payments” -related seem to chart a similar expansion. Textbook services around accepting, securing, and transacting payments still form the core of services provided, but they sit alongside billing and invoicing, loyalty, lending, targeted advertising, as well as nuanced services provided to specific verticals.

For the last decade, digital companies like SaaS providers have examined and/or executed on embedding payments on top of their existing offering, fueled by fears they were leaving revenue and greater control of the customer experience on the table. A healthy industry of providers has grown around enabling this. There are more layers here too: new tech is built onto old payments architecture, and broad white-label capabilities may obscure the real service providers. Further complicating this picture is the growth of global payment methods, whether card-based, or otherwise (e.g. BNPL, real-time payments, wallets, and bank-debits).

Digital payment volumes will continue to grow, but in an environment that seems harder to understand every day - impacted as it is by the triple impact of:

- Layering of services

- More services being marketed as part of “embedded payments”

- New payment innovations and payment methods

What Would You Say You Do Here?

It’s no wonder that merchants, service providers, or even curious individuals have a hard time orienting and educating themselves on the components that make up a payment stack. A large part of the trouble is that our terminology in describing payments just hasn’t kept pace. I wear both the teacher and student hats for my job - part of being successful in payments today (or really anywhere) is being able to embrace both, often in the same conversation. Any time I have tried to map the payments environment I described above along terms like “gateway”, “processor”, or “acquirer” I have gotten into trouble. Why do these terms get confusing?

How can we provide context and clarity? While staying specifically with the merchant/acquiring side of payments, let’s loosen our grip on these labels and think instead about the jobs being done.

At Spreedly, we think it’s important to clearly define our terms. To help everyone who has ever felt on the back-foot in understanding “acquiring services” I suggest we focus not on these insufficient labels, but on who is doing what jobs to keep a customer and merchant (or platform) happily engaging in commerce.

By focusing on the roles played, we can see through the labels and understanding how many of these services are wrapped up with a single provider. Let’s start with a few terms that get wrapped up in “acquiring.”

- Gateway: Any eCommerce payment needs to be submitted, secured, transmitted through the payments chain, and relayed back to a cardholder purchasing goods or services. This is the essential technology layer that begins the transaction process. It’s often compared to a point-of-sale device for ecommerce payments. Today it is rare to see a sole gateway provider, though this is how Braintree and Cybersource/Auth.net were originally structured. “Gateway” today is often used, (like “PSP”) as a catch-all term for a payment provider bundling a gateway offering alongside payment processor (see below) services.

Fun fact: Spreedly is not a gateway provider. But by offering secure transacting across different gateways providers, we offer security and flexibility in much the same way old standalone gateway providers would.

- Payment Processor: A Payment Processor (aka Acquiring Processor) performs a number of jobs that we will go into below. Using our “jobs” framework. Let’s think about it in 2-parts:

1. At Transaction

Payment processors during a transaction, receive the secure payment information from the gateway and relay it throughout the system of card-networks and over to the issuing side before receiving their response.

2. Outside of Transaction

Beyond everyday transacting, a processor also needs to coordinate many tasks such as chargebacks, settlement, and items like tax-reporting for merchants.

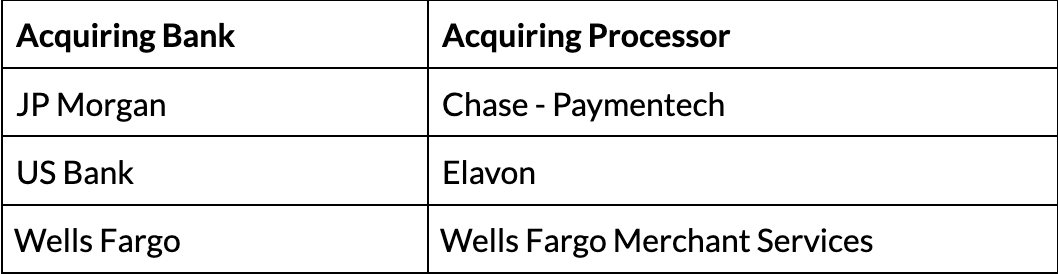

- Acquiring Bank: The Acquiring Bank (aka Merchant Bank) is responsible for maintaining the merchant’s bank account that funds will settle into. This may be a prominent bank with a strong, visible partnership with the processor, or its role may be downplayed, but it is subject to banking regulations and network rules. Processors working in partnership with acquiring banks are some of the largest names in payments:

- Payment Facilitators: Managed and wholesale payment facilitators (or “Payfacs”) can take many different forms. Chiefly, they allow merchants to accept payments quickly without needing the resources to get a merchant account directly with a processor.

They may be nearly invisible to a cardholder, or be a ubiquitous modern provider, like Square. Essentially PFs are “deputized” to take on key payment responsibilities in partnership with a processor/acquiring bank. After a thorough approval process, they act with authority from processors to underwrite and board merchants, offer customer support, and may offer their own gateway or other services.

Their payment services may be offered standalone or be wrapped into a larger ecosystem of non-payment offerings. Firms like Finix and Stax operate as payment facilitators among many others. Perhaps the best known organization that operates as a payment facilitator today is Stripe.

Payment facilitators often identify with the term “PSP” (“payment service provider”).

Roles in eCommerce / Jobs to be Done Framework

Astute readers will spy a few caveats to my descriptions and terms above (there are a lot of those in payments). But, coming back to the “payment jobs” framework will always help you break down the services being provided, however your provider self-identifies. Here are a number of key jobs. Here is a sample of key responsibilities and where they are owned:

During Transaction

Outside Of Transaction

When it comes to your own business, think about the jobs you need to do and what would take your payments environment to the next level. Coming back to the services being provided and the individual jobs being done simplifies a complex system of services and providers where the common terminology can confound as often as it clarifies.

So Where Does Spreedly Fit In?

Spreedly operates outside of the direct payment jobs, streamlining integrations and giving clients the flexibility to operate smoothly across payment providers. Leveraging our integrations across gateways, processors, and geographies grants clients all the flexibility of a diverse provider network, with none of the complexity of maintaining individual integrations.

The increasing complexity of payments has a direct correlation to the value payments can provide a company. Spreedly captures that value for clients, while managing out the complexity of building and maintaining individual connections. Our commitment is to give all the features and functionality of the best providers out there, without subjecting you to the “movie theater concessions” effect of being limited to the features of any single providers.

Want to see how Spreedly makes these jobs easier? Reach out today.

Download the Payments Orchestration eBook Below

Why is it becoming harder to understand the merchant payments landscape?

The merchant payments landscape is becoming more difficult to understand due to three main factors: the layering of multiple services on top of core payment functions, an increasing number of services being marketed as part of 'embedded payments,' and the continuous introduction of new payment innovations and payment methods like BNPL, real-time payments, wallets, and bank debits.

What is a payment gateway according to the Jobs to Be Done framework?

A payment gateway is the essential technology that handles the submission, security, transmission, and relay of eCommerce payments through the payments chain back to a cardholder who is purchasing goods or services.

Why does the blog post suggest moving away from traditional payments terminology like 'gateway,' 'processor,' and 'acquirer'?

The blog post suggests moving away from these traditional labels because they haven't kept pace with the evolution of the payments industry and cause confusion. Instead, it recommends focusing on the roles and jobs being done by different service providers, which allows for clearer understanding of how multiple services are often wrapped up with a single provider.