.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Navigating the complex terrain of e-commerce becomes even more challenging when businesses encounter payment declines. These declines not only affect immediate revenue but can also have long-term impacts on customer loyalty and brand image.

In this article we’ll first examine the differences between soft and hard declines and then describe how payment orchestration can reduce them.

What Is A Payment Decline?

A payment decline occurs when a payment method, typically a credit or debit card, is refused by the issuing institution or payment gateway during a transaction. This refusal can stem from various reasons, from insufficient funds to anti-fraud triggers. For businesses, comprehending these declines is important because they represent lost sales and can impact the customer experience. Differentiating between decline types, like soft and hard, aids in effectively addressing and preventing them.

The Types of Payment Declines

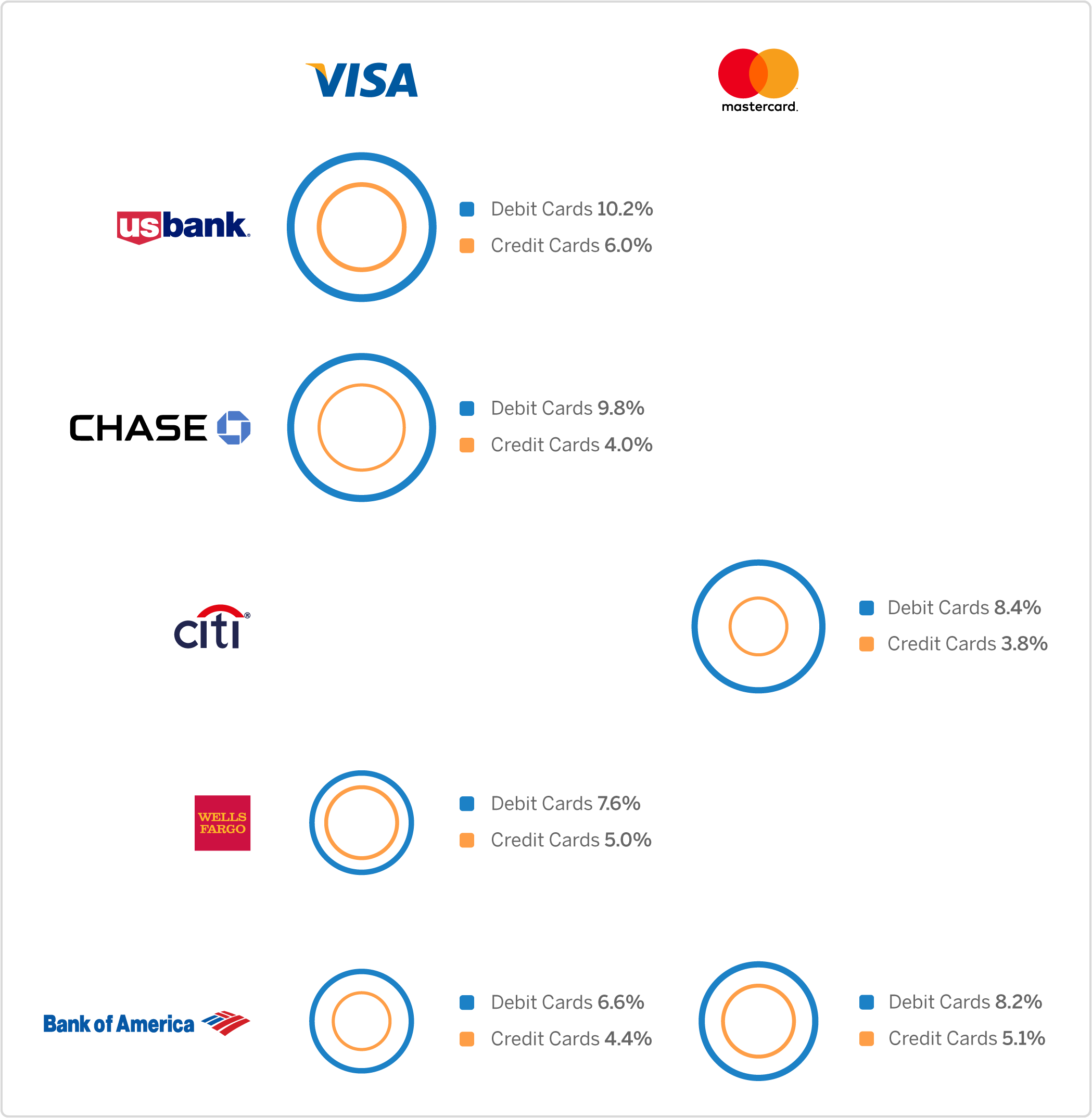

Payment declines, a source of significant friction card not present transactions, can be broadly categorized into two types: soft and hard. With an average 7.9 percent failure rate, understanding their differences allows businesses to address them more effectively.

Soft Declines

Soft declines are transaction rejections that occur due to temporary issues. Common causes include "Do Not Honor" responses, exceeded credit limits, or bank server downtimes. For instance, a "Do Not Honor" soft decline might arise when the issuing bank chooses not to approve a transaction, but without specifying the reason. While ambiguous, this decline isn't definitive; the purchase could potentially be successful if attempted later or under different conditions. Decline codes are specific codes provided by credit card networks or issuing banks when a transaction is not approved. Decline codes can also be produced by payment gateways, this is why transaction retry exists.

There are some common decline codes associated with soft declines.

- Do Not Honor: This code signifies that the bank is not willing to accept the transaction, but the specific reason isn't detailed. It's a generic response often requiring further investigation.

- Generic Decline: This is a non-specific decline where the bank does not provide additional details. Typically, the customer will need to contact their bank to get more information.

- General System Failure: This code indicates that the bank's system has experienced an error, and the transaction couldn't be processed. It's not a reflection of the customer's creditworthiness or account status.

- Card Type not Supported: The transaction is declined because the merchant does not accept the specific type of card being used, such as a particular credit card brand or a gift card.

- Currency Not Supported: This indicates that the currency of the transaction is not supported either by the merchant's setup or the card issuer. For instance, a card that only supports USD transactions being used for a EUR purchase.

Hard Declines

Conversely, hard declines are definitive rejections of transactions. They arise from more severe issues like expired cards, reported lost/stolen cards, or blocked accounts. An example might be when a card number is entered incorrectly multiple times, leading the issuing bank to decline any further attempts for security reasons. These are the most common hard decline codes.

- Do Not Honor: The issuing bank has chosen not to honor the transaction, possibly due to a suspicion of fraud.

- Invalid Card Number: The card number entered is not valid or contains an error.

- Expired Card: The card used for the transaction is past its expiration date.

- No Account: The account associated with the card number doesn’t exist.

- Security Violation: This code indicates a breach in the transaction's security parameters. It may be triggered if certain security criteria are not met, like using a card from a blocked country or IP address.

- Suspected Fraud: The transaction is flagged as potentially fraudulent by the card issuer's internal systems. This can result from unusual spending patterns, rapid successive transactions, or other fraud detection parameters set by the bank.

- Incorrect CVV: The transaction was declined because the CVV (Card Verification Value) entered did not match the one on the card. This security feature ensures that the person initiating the transaction is in possession of the physical card.

Looking to navigate these declines? Payments orchestration offers tools and strategies tailored for both.

Ways Payments Orchestration Reduces Declines

Payments orchestration is the evolved way of processing payments. It provides businesses with a nuanced approach tailored for different decline scenarios.

- Transaction Retry for Soft Declines: If a transaction encounters a soft decline due to a gateway server being temporarily down, orchestration can automatically reroute it to an alternative gateway for processing, increasing the chances of success.

- Fallback Mechanisms for All: Whether it's a soft decline from a generic decline or a hard decline due to a blocked account, having secondary and tertiary gateways and diverse payment methods means there’s always another path to attempt the transaction.

- Local Optimization: For international businesses, using local gateways can prove beneficial to accept specific payment methods. A card from a specific region might face hard declines when processed internationally but could be successful through a local gateway.

- Using Multiple Token Formats: Retry strategies can incorporate different token formats (e.g. retrying with the PAN, a PSP-token or a network token) to complement multiple gateway integrations and increase authorization rates.

Intelligent Analysis for Soft Declines

Soft declines, being temporary, can be addressed by studying patterns. With intelligent analysis, payments orchestration platforms can predict the best times or methods to re-attempt a transaction, turning potential declines into successes by using the following strategies.

- Dynamic decision-making based on real-time data.

- Reducing friction points leading to soft declines.

- Advanced security measures that identify and mitigate soft decline causes.

Strategizing for Hard Declines

Hard declines require a different proactive approach, demanding businesses to swiftly react and provide alternative solutions. With payments orchestration, the power to preemptively address these declines lies at one's fingertips. The platform can:

- Suggest alternative payment methods immediately to the customer.

- Provide instant feedback, so customers are aware and can use another card or payment method.

- Automate the process to prompt users for updated card details if their card is nearing expiry.

- Update stored-card information automatically through card lifecycle management (especially useful for recurring payment models)

The Payment Agnostic Approach

Payments orchestration is not just about addressing declines. It's about offering a flexible, efficient, and user-friendly payment process that isn't tied to a single payment method or provider, ensuring businesses and their customers always have a range of transactional options.

For an online retailer with a global audience adopting a payment agnostic approach can ensure that a customer in Japan using JCB Card, another in the Netherlands preferring iDEAL, and another in the U.S. using PayPal, all have a seamless and satisfactory checkout experience. This adaptability can lead to increased sales and happier customers.

Stay Ahead Of Declines

The intricacies of payments can be complicated, especially with hurdles such as soft and hard payment declines. However, by leveraging payments orchestration, businesses can optimize their strategies to address both types of declines head-on. It's important to forecast the future and capitalize on the present.

Ready to increase your transaction success rate? Learn more about how payments orchestration and elevate your e-commerce game.

Download the Payments Orchestration eBook Below

What is the difference between soft and hard declines?

Soft declines are transaction rejections due to temporary issues such as 'Do Not Honor' responses, exceeded credit limits, or bank server downtimes. These declines aren't definitive and the purchase could potentially be successful if attempted later or under different conditions. Hard declines, by contrast, are permanent rejections that cannot be retried because they indicate fundamental issues with the transaction or account.

What are some common decline codes associated with soft declines?

Common soft decline codes include: 'Do Not Honor' (bank unwilling to accept transaction without specifying reason), 'Generic Decline' (non-specific decline with no additional details), 'General System Failure' (bank's system error), 'Card Type not Supported' (merchant doesn't accept the specific card type), and 'Currency Not Supported' (transaction currency not supported by merchant or card issuer).

How can payment orchestration help reduce decline rates?

According to the blog post, payment orchestration can reduce both soft and hard decline rates. By understanding the differences between decline types and implementing strategies through payment orchestration, businesses can more effectively address and prevent payment declines, thereby reducing the average 7.9 percent failure rate and improving revenue and customer experience.