.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

It’s in there. Somewhere in your payments stack, right now, a customer's actual card number is sitting in a database doing absolutely nothing useful except waiting to be stolen. Network tokenization fixes that problem, and as a very compelling added bonus it recovers authorization revenue you didn't know you were losing.

We’re going to explain how the technology works, why it outperforms both PCI tokenization and encryption for payment credentials, and how to build a token strategy that sets you on a winning track.

What is tokenization of data?

Tokenization of data is the process of replacing a sensitive value with a non-sensitive stand-in, called a token, that has no exploitable value outside the system that issued it. Maybe you could think of it like a coat-check ticket: it's worthless to anyone who steals it because the only coat it retrieves is at the specific coat check where it was issued, and that coat check has a bouncer and, well, you’re just not getting in.

In payments, the sensitive value being swapped out is the primary account number on a card, the PAN, a 16-digit string that has caused more sleepless nights in more security teams than any other piece of data in commerce.

Tokenization replaces it with a surrogate that your systems can store, reference, and route without ever touching the actual card number, which is a genuinely elegant solution to a problem that previously required either trusting everyone in your data pipeline or building a very expensive wall around all of them.

The PCI DSS compliance benefit lands on top of all that: properly tokenized data isn't classified as cardholder data at all, which means the systems handling only tokens can fall entirely outside PCI scope. Your auditors probably won't send flowers to celebrate, but they'll have considerably less to audit, which is the next best thing.

Tokenization vs encryption: the difference that actually matters

Both encryption and tokenization protect sensitive data, and distinguishing between them has launched approximately ten thousand earnest LinkedIn posts, none of which quite sticks the landing. They're related concepts that solve different problems, and the difference between them is the difference between a lock that can be picked and a door that isn't there.

Encryption transforms data mathematically using a key, producing scrambled ciphertext that can be unscrambled by anyone who has that key. The protection is only as durable as the key management, which is a polite way of saying the key is the whole game. Lose it to the wrong person and every piece of data it was protecting is now readable.

Tokenization does something else entirely. It replaces sensitive data with a reference value that has no mathematical relationship to the original whatsoever, meaning there's no transformation to reverse and no key to steal. The mapping between token and original data lives in the vault, and without vault access the token is a completely meaningless string that does nothing for anyone who finds it.

For PCI DSS compliance, the difference between these two approaches isn't a technicality. Encrypted cardholder data is still cardholder data under PCI DSS, which keeps every system touching it firmly inside your audit scope. Tokenized data, implemented correctly, can be classified as out of scope entirely, which is the compliance equivalent of discovering that a significant portion of your annual audit anxiety was optional. That scope reduction translates directly into lower security overhead, simpler vendor assessments, and an engineering team that isn't spending weeks every year answering questionnaires about systems that no longer handle the data in question.

There’s something we should make clear before we move on: an "encryption token" in the hardware and software security world refers to a physical or software device used in cryptographic authentication, which is a completely different concept from a payment token. If you searched for "encryption token" expecting payment tokenization content, you've arrived at the right place by the wrong road, and we're glad you made it. Welcome!

Network tokenization vs PCI tokenization: same word, very different plumbing

PCI tokenization and network tokenization are both called tokenization, which isn't quite as helpful a naming convention as whoever coined it probably thought it was.

PCI tokenization lives inside a closed ecosystem, typically a gateway or processor vault, and it does a solid job of reducing compliance scope within that environment. The problem arrives when your infrastructure changes, which it will, because every business that grows eventually outgrows its original gateway relationship.

A PCI token issued by one gateway means nothing to another, which means your stored credentials stay behind every time you want to move, like a phone number that only works on one carrier and can't be ported.

Network tokenization is issued by the card network itself and recognized across the entire acquiring ecosystem. It's domain-restricted to your merchant context, lifecycle-managed by the network when cards are reissued, and carries authentication signals that issuers trust considerably more than a static card number arriving from parts unknown. Universal issuer support isn't yet complete, and merchants often still need to maintain the PAN to facilitate optimal processing, which is precisely why Spreedly's payment vault stores network tokens, processor tokens, and vaulted PANs together, routing to the best available credential automatically rather than making that a manual decision for your engineering team.

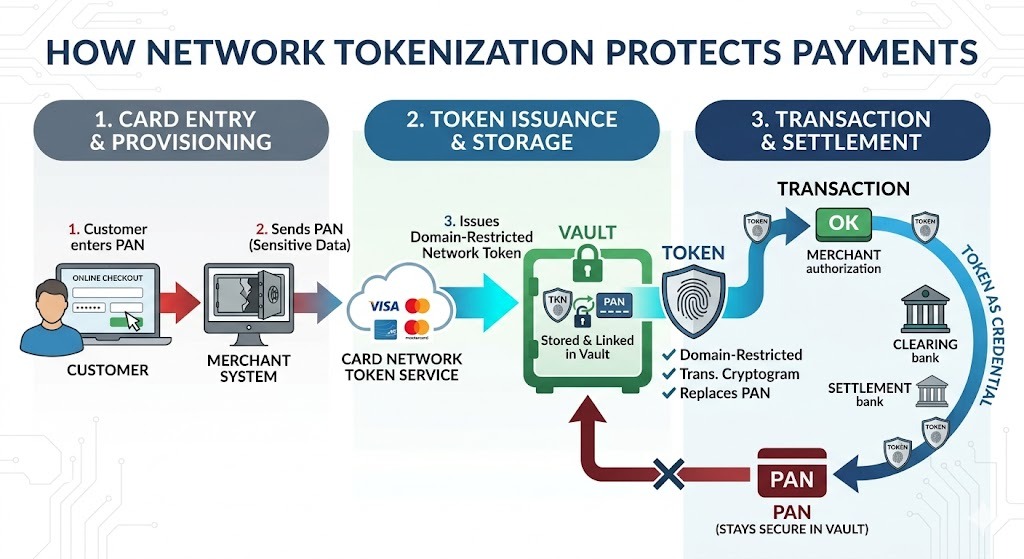

How network tokenization works in production

When a customer enters their card details at your checkout, the provisioning process kicks off. Your system sends the PAN to the card network's token service, which issues a network token in return. That token is domain-restricted to your merchant context, carries a transaction-specific cryptogram for authentication, and gets stored in your vault linked to the underlying PAN. From that point forward, the token is the credential that travels through authorization, clearing, and settlement, while the actual card number stays in the vault like a very important document that nobody needs to look at on a regular basis.

The lifecycle management piece is where most of the revenue recovery actually lives, and it deserves more than a passing mention. When a card is reissued because it expired, was reported lost, or was compromised at some entirely unrelated merchant, the card network updates your token automatically.

The customer gets a new card number in the mail, considers it mildly annoying, and gets on with their life. From your systems' perspective, nothing's changed. The subscription keeps billing. The repeat purchase completes. The saved payment method in your checkout just keeps working, which sounds like it should already be true of all payment systems and is, in fact, the exception rather than the rule for anyone relying on static card credentials.

Spreedly's payment optimization layer sits above this process and applies routing and retry logic at the credential level, selecting the best token type for each transaction based on provider acceptance, real-time performance data, and cost. The network maintains the credential. You decide how it moves through your business, which is a considerably more comfortable arrangement than the alternative.

Reduced fraud exposure, or: why a stolen network token is a remarkably bad score

When a fraudster compromises a card number at another merchant, that number is effectively gone. Every merchant storing that PAN is now holding a credential that's been passed around the dark web like a bad secret, and the only question is who tries it first.

Network tokens are domain-restricted to your merchant environment, which means a breach somewhere else in the ecosystem doesn't touch yours. A token that only works at your checkout is about as useful to a fraudster operating elsewhere as a library card for a library they're not a member of, in a country they've never visited, for books that don't exist.

According to 2025 industry data, over 70% of financial institutions reported a reduction in payment fraud after implementing tokenization, and the reduction works in two directions simultaneously. Tokenized credentials have no exploitable value outside their authorized domain, which removes stolen data reuse as an attack vector entirely. The stronger authentication signals that network tokens carry to issuers also mean fewer legitimate transactions get flagged as suspicious and declined, which is a different version of the same revenue recovery story wearing a security hat.

Who benefits most, and who should have started yesterday

Subscription and membership platforms

For any business that bills on a recurring schedule, the most insidious failure mode isn't fraud and it isn't pricing and it isn't even churn in the traditional sense. It's the slow bleed of customers who fully intended to stay but whose card expired while your vault was asleep at the wheel, triggering a failed renewal that becomes a cancellation that becomes a customer you now have to spend actual money to reacquire.

Network tokens eliminate that failure mode entirely because the credential updates when the card does, automatically, without your customer doing anything or your engineering team writing a single remediation script, which means the subscriber never notices the problem that would have cost you their business six months ago.

Marketplaces and platforms

Platforms operating across multiple sellers, regions, and acquiring relationships have a structural problem with PCI tokens: the credential that works with one processor doesn't travel to another, so every time you add a local acquirer or shift volume for performance or cost reasons, you're working around your own stored payment data like someone who packed their suitcase and then discovered the zipper only works in one hotel. Which would be weird, but is still a solid analogy.

Network tokens are portable across the acquiring ecosystem, which turns provider strategy from a credential management headache into a straightforward performance decision, and Spreedly's payment vault makes that portability operational across your entire provider network from a single integration.

Travel, ticketing, and hospitality

These industries store a card at booking and charge it weeks or months later, by which point the card may have been reissued, the customer may have forgotten which card they used, and your settlement system is about to have a conversation with an issuer that nobody scheduled and nobody wants.

Network tokens close that gap because the credential stays valid across the card's entire lifecycle, regardless of what happens to the underlying card number between the booking date and the capture date, which removes one of the more embarrassing failure modes in high-value transaction processing.

Enterprise ecommerce and retail

At high transaction volumes the authorization rate argument adds up fast, and Visa's tokenization research documents a 4.6% global authorization lift for tokenized transactions compared to PAN, which means a one-point improvement in approval rates at $50 million in monthly volume is $500,000 per month in recovered revenue that was previously evaporating into the decline column without so much as a farewell. The fraud reduction benefit runs the same direction, with 2025 industry data showing over 70% of financial institutions reporting fraud reduction after implementation, because the more transactions you process, the more valuable it is to hold credentials that are worthless to anyone operating outside your merchant context.

Network tokenization and agentic commerce: the reason this section didn't exist in last year's version

A year ago, agentic commerce was a conference topic that made people nod thoughtfully and then return to their existing roadmaps with their existing priorities intact. Today it's a live channel where AI agents complete purchases on behalf of consumers with minimal human input, and if you've ever watched someone's AI assistant confidently buy the wrong size of something in the wrong color with overnight shipping, you already understand why the payment infrastructure underneath this channel needs to be extremely good.

According to NMI's 2026 payments predictions, network tokens represent the critical infrastructure for emerging payment technologies like biometric checkouts and agentic online shopping, and the card networks have already built the programs to prove they mean it. Visa's Intelligent Commerce and Mastercard's Agent Suite are both built around "Know Your Agent" frameworks that use network tokens to distinguish legitimate agents from malicious bots, ensuring authorization stays within established rails, as detailed by the IMF's 2026 analysis of agentic AI in payments.

The underlying logic here is the same domain restriction that makes network tokens fraud-resistant in traditional commerce, except now the threat model includes not just criminals with stolen card numbers but also AI agents that have decided your entire holiday shopping list needs to be completed before lunch.

A merchant without a mature network token strategy is a merchant who can't participate cleanly in this channel, and given that according to Checkout.com's 2026 payments trends, multiple competing agentic protocols are actively gaining traction with no clear winner yet decided, the merchants building flexible token infrastructure now are the ones who won't be scrambling to retrofit it when the standard firms up.

Spreedly's payment orchestration layer ensures network tokens flow correctly across providers regardless of which agent protocol initiates the transaction, which is exactly the kind of infrastructure decision that looks obvious in hindsight and costs considerably more to fix after the fact than before it.

How Spreedly operationalizes network tokenization

Most merchants who decide to implement network tokenization promptly discover that the decision was the easy part. Integrating independently with Visa's token service, Mastercard's Digital Enablement Service, and American Express's token infrastructure is the kind of project that looks reasonable on a roadmap in January and is still "nearly done" when the leaves turn. Spreedly removes that problem entirely.

Spreedly's payment vault provisions network tokens from Visa, Mastercard, and American Express, stores them alongside processor tokens and vaulted PANs, and makes them available across your entire provider network through a single integration. The vault is also the system of record that manages the token lifecycle, so when a card is reissued and the network updates the token, the vault keeps both linked automatically without your team doing anything that could be described as work so they can just sit at their desk and eat popcorn. Or actually work on making sure people find and buy your product. Up to you, really.

Smart payment routing applies logic above the credential level, selecting the best token type for each transaction based on provider acceptance, real-time performance data, and cost, which means network tokens compete on merit rather than infrastructure constraints forcing the decision.

Performance reporting ties outcomes back to credential type, routing decisions, and provider performance, so the impact of your token strategy is visible and measurable rather than something you have to take on faith. The architecture is designed so that as network token support expands across issuers and regions, your stack improves without a replatforming project, which is exactly the kind of sentence your engineering team would very much like to hear more often.

Network tokenization is a revenue strategy with excellent security included

Here's a sentence you don't read often enough in payments infrastructure content: this one actually pays for itself, and then keeps going.

Merchants who treat network tokenization as a security project are leaving money in the decline column, customers in the churn bucket, and agentic commerce on the table while they wait for a better time to deal with it. There's no better time. Transaction volume is projected to double by 2029, the networks are building the mandates, and the AI agents are already out there shopping whether your token infrastructure is ready for them or not, which in this industry is its own kind of miracle.

Spreedly's payment vault provisions and stores network tokens across Visa, Mastercard, and American Express alongside your existing processor tokens and vaulted PANs, smart routing selects the best credential for every transaction, and performance reporting shows you what it's all worth in numbers you can put in a deck.

What is network tokenization and how does it differ from PCI tokenization?

Network tokenization is a credential issued and managed by the card networks themselves, Visa, Mastercard, and American Express, and recognized across the entire acquiring ecosystem. PCI tokenization is created inside a closed ecosystem, typically a single gateway or processor vault, and doesn't travel outside it. The practical difference is portability: PCI tokens bind your credentials to the provider that created them, while network tokens move with you as your payments strategy evolves.

What is the authorization rate improvement from network tokenization?

Visa's data shows a 4.6% authorization rate lift globally for tokenized card-not-present transactions compared to PAN-based transactions. The improvement comes from the stronger authentication signal a network token sends to issuers: it identifies a known merchant in a known transaction context, which issuers trust considerably more than a static card number. At meaningful transaction volumes, that lift translates directly into recovered revenue that was previously sitting in the decline column.

Do I need to integrate separately with each card network to use network tokens?

No. Spreedly's payment vault provisions network tokens from Visa, Mastercard, and American Express through a single integration, storing them alongside processor tokens and vaulted PANs. Routing logic selects the best available credential for each transaction automatically, which means you get the performance benefits of network tokens without a separate integration project for each network.