.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

It should come as no surprise that consumer spending trends continue to shift to online versus shopping in brick-and-mortar stores. To illustrate the point, The Balance reports that 2019 Black Friday online revenue grew by 19.6% over the previous year, and yet brick-and-mortar store sales only increased by 1.6% for the same timeframe.

This explosive growth in online transactions creates challenges for merchants looking to provide the best customer experience possible. Successful merchants are those that consider frictionless, highly secure purchase experiences that will delight their customers.

Enter network tokenization.

What is Network Tokenization?

To understand how network tokenization can improve the customer experience, we first have to understand the core benefits of network tokens.

Network tokenization involves payment networks like Visa and Mastercard replacing a primary account number (PAN) with a unique payment token, or network token. The nature of provisioning a network token is a partnership between issuers and card networks. The card network facilitates the delivery of network tokens and the issuers are responsible for the creation of network tokens. As a result, network tokens have a built in layer of validation and security. Furthermore, the token is restricted in its usage to a specific merchant or device.

Since the network tokens are validated and merchant specific, the tokens are highly secure and can be used across the entire payment ecosystem. An additional benefit of the partnership with issuing banks is that network tokens receive updates in real-time, ensuring credentials are always up-to-date, even after a physical payment method has been locked due to fraud. Expired cards, invalid account numbers, and CVV/CVC failures are no longer relevant.

While we’ve covered the merchant benefits of network tokenization in greater detail in a recent blog post, we now have foundation to discuss how secure, dynamic network tokenization provides better checkout experiences.

Automatic Payment Detail Updates

Creating a simple, fluid checkout experience is a critical part of a bigger eCommerce strategy to help combat cart abandonment. Even if merchants overcome the hurdle of initially capturing their customers’ card details, they still face the inevitability that those details will change at some point in the future.

Regardless if the customers card details change due to their card being lost, stolen, or expired, the result is that merchants risk involuntary churn if they don’t have their customers intervene directly. As a customer, this can lead to a negative experience. Repeated alerts notifying a customer of invalid card details, notifications requesting action, and the manual process of updating account credentials are just some of the touch points that can negatively impact a customer’s experience with a brand. These touch points are constructed to avoid the aforementioned loss of goods or services all together due to a missed payment.

Network tokens can prevent these customer experience headaches by automatically updating card details when changes occur. Since network tokens are created in partnership with the issuer, the initial card details can change and the token will still be valid. Furthermore, network tokens give merchants the ability to receive the updated card details so that they can be displayed directly to customers in a UI.

As a result, transacting with network tokens greatly reduces involuntary churn and unnecessary headaches that come with manually keeping your credit card details up to date.

Robust Check Out Experiences

Along with the ability to send updated credit card details to merchants, network tokens all share additional metadata that can make the checkout experience more robust.

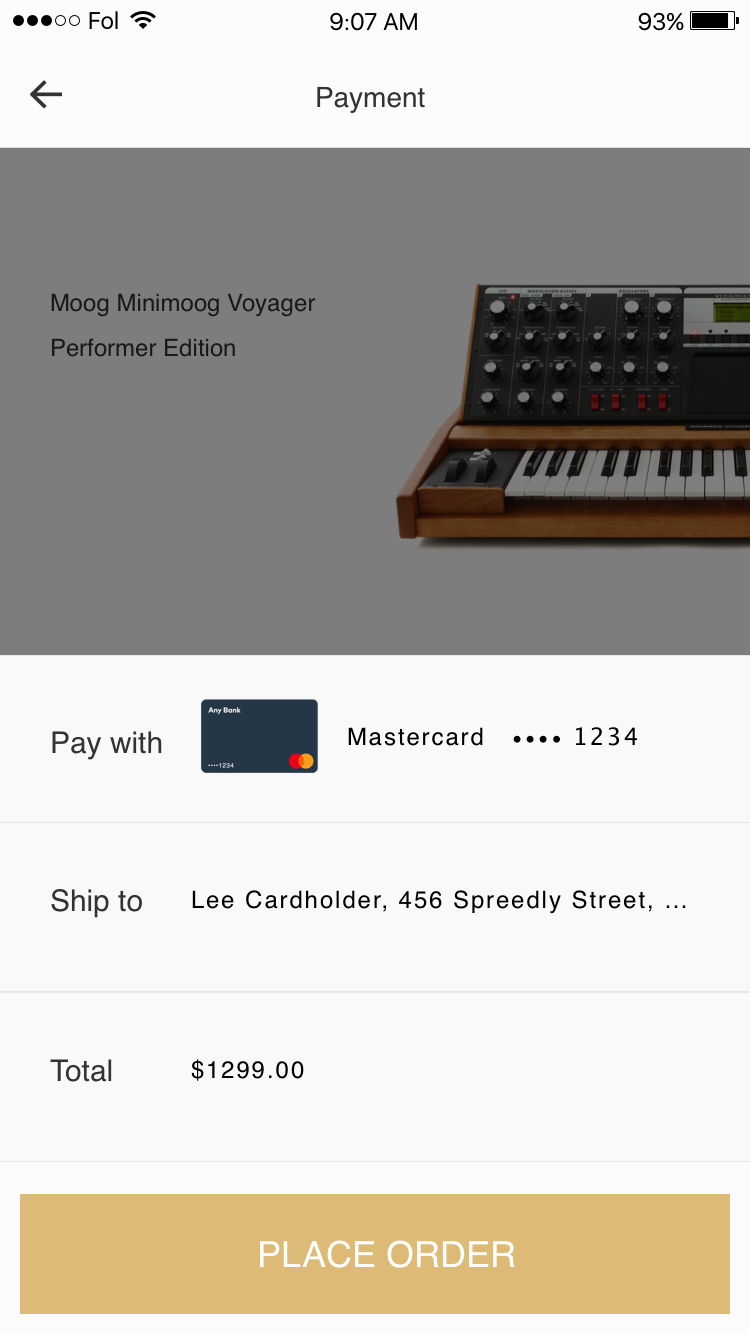

One such use of metadata is the introduction of digital card art. When a network token is provisioned, the issuer also provides detailed card art that matches the card being used at checkout. It should be noted that the provided card art will not include sensitive details such as name, PAN, or even if EMV contact chips are present.

While PAN is not displayed directly on the card art, best practice dictates that merchants should include both the network and last 4 digits of the PAN alongside the card art. We’ve illustrated this approach above. This approach also has the added benefit that the networks can easily send PAN updates through network tokens without the need to reissue card art.

The combination of card art, card network, and last 4 digits has shown to increase the customer’s confidence that they are purchasing with the correct card. In practice, this leads to higher completed checkouts for merchants.

Learn more about how Spreedly helps merchants to optimize their revenue and support tokenization. Or contact Spreedly to talk to a payments expert about your optimization efforts and how we have propelled results for our customers.

Download the Tokenization eBook