.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Payment behavior in Argentina is a unique patchwork of social history and economic reality. If you’re looking to scale into the region, it’s a truth you have to deeply understand.

In stable economies, payments tend to operate within systems that were built for predictability. Businesses optimize accounts payable for efficiency, and consumers comfortably use credit to spread out larger purchases. In Argentina, you’re going to need sharper timing and find a way to take more control of the situation. When inflation is elevated and currency values shift quickly, payment behavior becomes more deliberate, and you’ll find that consumers and businesses prioritize liquidity, speed, and financial stability over everything else.

Historic distrust of financial institutions, stubborn inflation, and an unstable currency have combined to create a unique environment for payments. The rapid growth and adoption of digital payments has only fueled it.

What does all of this mean for businesses? The short answer is that you need to rethink your Argentina payments setup from the ground up. The longer answer is found in the sections below.

Payment behavior is a symptom of national economics

Before I go any further, I want to be really clear about something: This isn’t a quaint drive-by cultural tour. We’re talking about the serious effects of a high-inflation, high-volatility economy. It creates a unique situation for consumers and businesses in which forward planning can’t extend beyond a few days.

Argentina has had a difficult few decades economically, starting with the 2001 corralito measures in which the government froze citizens’ accounts. By preventing withdrawals in an attempt to stave off financial collapse, the value of savings was destroyed by currency corrections. The country fell into chaos. 40 were killed in the demonstrations and a deep-seated mistrust of politicians and banks remains to this day.

Today, 31.2% of Argentina’s consumer savings and investments are held in foreign currency accounts, with over half of all adults holding such an account. These scars also show up in Argentina’s adoption of cryptocurrency, for which it ranks 20th worldwide.

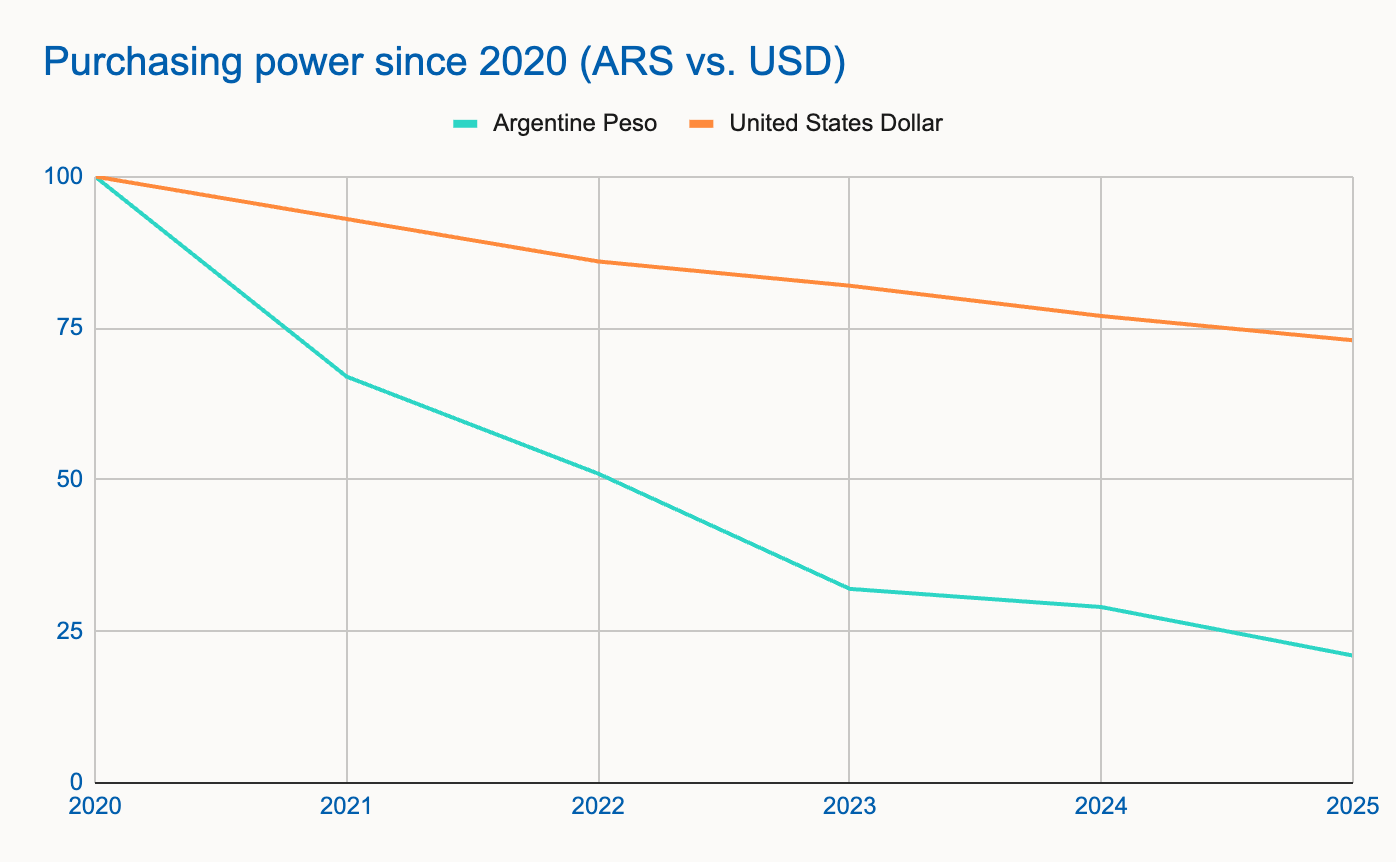

More recently, chronic inflation and currency instability has been hard to shake. The biggest single-day rise and fall in the Argentine Peso were both over 50%. They’ve also both happened in the last 18 months. Meanwhile, January 2026’s inflation rate of 32.4% might be 13x the rate in the U.S., but it’s a mellow ride compared to the dizzying highs of 292% in April 2024.

Using CPI and inflation as a way to understand purchasing power, we can see the scale of the problem for Argentinians. The table below explains the decrease in purchasing power, from a baseline of $100 for each respective currency, starting in 2020.

Broadly speaking, inflation’s effect on consumer behavior usually leads to fewer purchases and greater price sensitivity. When people do spend, however, they do so faster than usual. When you’re managing that much volatility, payment timing behavior has nothing to do with marginal gains or even convenience; it’s about staying afloat, keeping liquidity, and surviving unpredictability.

I totally understand it. If I had to make a big purchase with inflation at 30%, I’d rush to pay for it before it got any more expensive. The inevitable pressure that follows on liquidity and cash flow is its own problem to manage.

Payment behavior in Argentina is driven by larger forces

Keep perspective and consider the macroeconomic context of Argentina. When currency volatility and inflation are out of control, your influence is understandably limited.

Digital rails drove a shift in payment culture

Product development can drive behavior or respond to behavior. Every now and again, they dovetail at the perfect time.

When the value of your currency and inflation are out of control, speed is of the essence and debt can quickly become impossible to manage. This is why digital and real-time payments have taken off, far exceeding short-term credit in popularity.

In Argentina, 25% of adults have used a credit card in the last 12 months. 72% had made or received a digital payment.

You only have to look at the scale of mobile adoption to see how it intersects with the growth in instant payments. 90.6% of the population is believed to be online, well above the global average of 70.2% and South America’s average of 83.8%. In the space of 10 or 15 years, a brand-new medium has become the default for most citizens.

Digital wallets and other instant payment systems are so desirable because they move funds quickly, keep cash liquid, and can transact in more stable currencies. At a time when macroeconomic pressures have squeezed citizens, these platforms have provided breathing room.

The demand for close control over payments in Argentina was already clear; the development of digital and real-time payment infrastructure in LatAM has accelerated it.

A perfect storm for digital payments

It’s rare that consumer needs, product maturity, and platform adoption converge simultaneously. That’s where Argentina is with digital payments right now.

Payment urgency shows up in the numbers

This mix of political, macroeconomic, and social factors shows up clearly in payments data for Argentina.

From 2019-2024, LatAm’s payments revenue grew faster than any other region in the world (11% vs. 7% global average). Argentina, however, is ahead of the already impressive curve. In 2021, digital payments accounted for around 30% of all e-commerce spending in Argentina. That was triple the level seen in Brazil, which had the next highest usage.

At the same time that digital payment usage in Argentina has soared, use of credit trails behind other nations. Across Argentina’s population, 37.4% of adults have a credit card compared to 81% of Americans and 65% of UK citizens. Brazil and Argentina are often held up as South America’s two leading economic forces, but 51.6% of Brazilians use credit cards.

With digital wallets offering features like instant payments and multi-currency accounts, the attraction is clear. For a population that has very recent scars from the central banking system, international providers beyond governmental control offer an important safe haven.

Global payment architecture doesn’t fit in Argentina

Holding consumer debt when inflation is in the double-digits and your currency moves like it’s dancing the tango is basically unthinkable. If your payments system fails to reflect this, you’ll be holding your business back from success in Argentina.

A business that wants to succeed in any foreign market has to meet the unique needs of the consumer base there. In Argentina, much of this comes down to payment methods – for all the reasons explained above.

When your checkout only accepts Visa, Mastercard, and American Express, your Argentinian customers are going to bounce. The solution is an adaptable payment system that responds to customer geography, not company geography. In this case, that looks like multi-rail checkout, instant payment options, and contextual fraud awareness.

The secret of an effective global payment system is a foundation of deep local expertise.

Fix the foundations first

Before you tweak your social ads or product pages to improve performance in Argentina, look at the basics of your payment system. No amount of decoration can cover up an architectural mismatch.

Prioritizing fast, adaptable infrastructure

Building an Argentina-ready checkout doesn’t end with you accepting payment methods like Mercado Pago and Ualá or provincial systems like Cuenta DNI. In fact, that’s only the first step.

The system behind your payment acceptance is where you can really make or break growth in Argentina. If you’re accepting local payment methods but treating them no differently than payments you receive domestically or in Europe, you’re only passing the problem further down the chain. Those payments can be flagged in card-centric fraud systems or take too long to settle over international networks (leaving either you or your customer exposed to currency risk).

Ideally, your payments infrastructure will be powered by multiple local rails, routing each transaction to the optimal path based on value, timing, geography, and other unique factors.

In most cases, you have to pick between an intelligent, dynamic system and one that moves and settles quickly. Payment orchestration, like Spreedly’s Connect, combines both to give you a genuinely global payment solution. Our concurrent products complete the system: Optimize routes and retries in real-time, while Protect embeds anti-fraud tech into your checkout and Resolve provides granular data intelligence.

Infrastructure as a conversion tool

Adaptable and flexible infrastructure is good for uptime and performance. In fast-moving markets, it goes much further and becomes a last-mile revenue engine.

The commercial value in understanding payment behavior

In stable economies with low inflation and predictable currency movement, payments are optimized for experience. Consumers care about rewards, convenience, and a seamless checkout. Credit helps smooth out larger purchases, settlement timing rarely creates urgency, and small shifts in value don’t meaningfully change behavior.

In more volatile environments, payments serve a different role. They become a way to protect liquidity and manage risk. When inflation runs high and currency values can swing dramatically, timing isn’t about convenience or earning points. It’s about preserving purchasing power and keeping control over cash flow.

In the world of e-commerce and payments, we love to focus on the marginal gains that can improve performance. Frankly, entering the Argentinian market can be humbling. No amount of UX interviews or product description tweaks can change the economic reality your customers are living in.

To meet your customers in Argentina, forget about what they might want. They need speed, flexibility, and security when making a payment or transfer. That’s not easily done when you’re transplanting U.S.- or Europe-centric infrastructure. Instead, you need intelligent and flexible payment orchestration.

Payment orchestration accommodates the unique payment behavior in Argentina, which is self-evident in global payments data. With reliable orchestration in place, you’ll be set for success in Argentina.