.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

The way that merchants process credit cards has come a long way. We started with the kerchunk! of the earliest “knuckle busters” that imprinted credit card information onto paper, to swiping the magnetic strips on early vendor POS systems, to chip cards, and have gotten all the way to contactless & mobile payments via NFC.

With all of that said, the speed at which credit card processing develops is entirely dependent upon merchant adoption. It took decades for chip cards to be embraced on a global scale!

The technology that makes it easier for us to pay for goods and services at brick-and-mortar shops has been a big part of how we’re beginning to process payments online.

But now there’s more work to be done, especially in the ways that merchants accept credit card payments online.

So what’s being done, and who’s leading the charge? We’re going to take a look at a popular way of processing credit card transactions online, and show you, the merchant, how you can get involved. But first, let’s take a look at the problems a lot of you are facing right now.

There is a disconnect between the physical and digital payment worlds

In the world of physical payments, Tap to Pay is—to channel Ron Burgundy for a moment—kind of a big deal. According to Mastercard, two out of three in-person transactions on their network are contactless.

It’s not just in the consumer’s wallet—it’s on their phones, and their watches. It’s an ever-present solution to a problem merchants and payment processors have been trying to solve for several decades now. “It’s in your wallet,” is now, “It’s on you somewhere, that’s for certain.”

The process of paying for something in person is remarkably simple. Wave a card or device over the machine that accepts the payments and it’s all done. You take your stuff and leave.

But when we look at online solutions for simple payments, the efficiency of this process for real-world users starts to look more complicated, less trustworthy, and about as fun as standing in a long line at the DMV.

Frustration and friction is to online payments as a tax audit is to a lottery win.

So what’s the problem? Why are we still making it so difficult for people to make transactions online? According to Grand View Research, e-commerce accounted for $25 trillion in 2023. What kind of opportunities are merchants losing, and why is that happening?

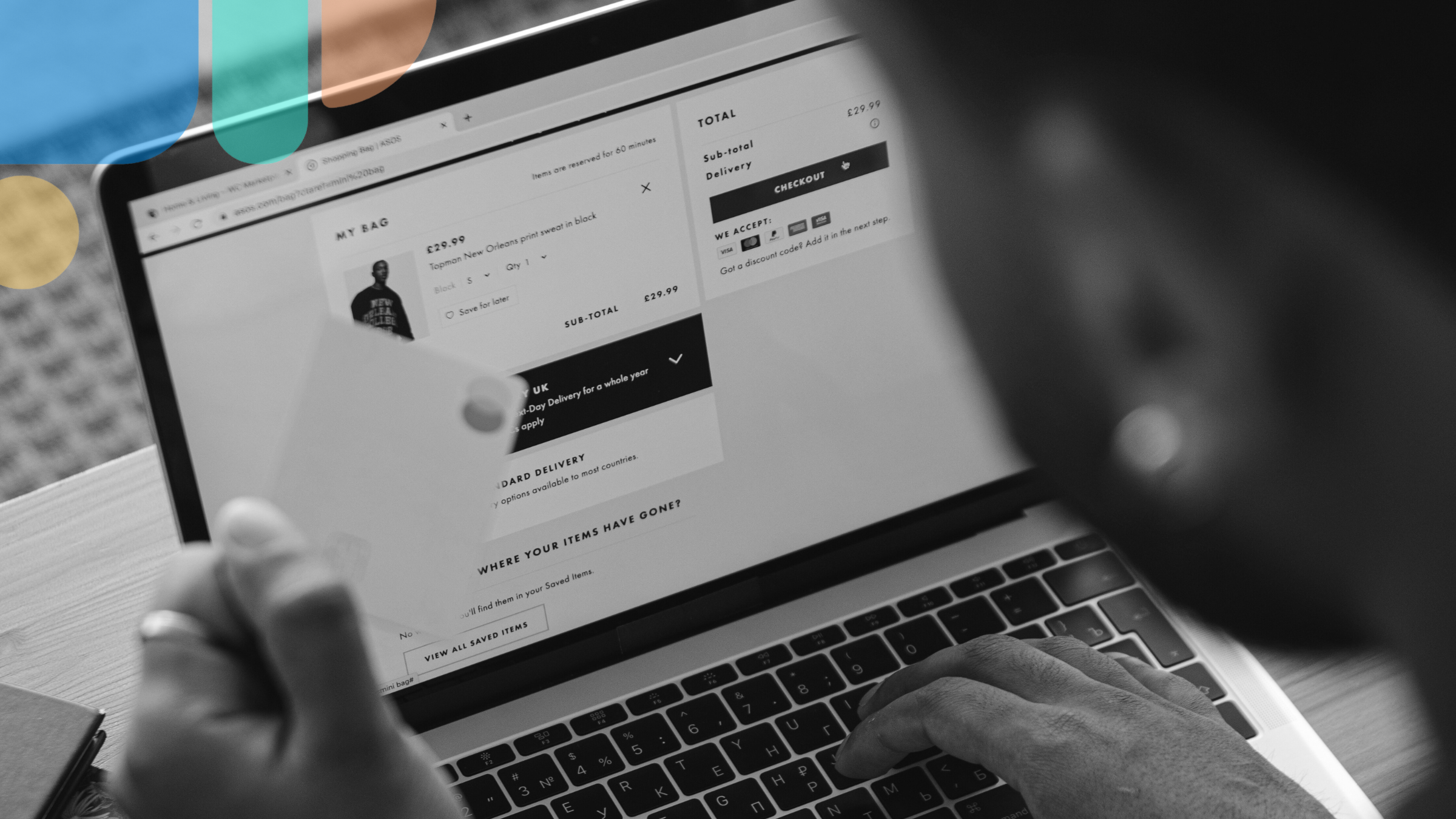

A real-world example of cart abandonment

Although I’m just a sample size of one, I see this happen in my life all the time. For example, I have a package coming from Texas that will eventually be delivered to me in Montreal.

In order for this package to clear customs, I have to pay duty on the item. I get an email from the delivery company advising me that this is the case (no, it’s not a phishing email, but, seriously, thank you for your concern), and I click through to a payment page.

My information wouldn’t autofill on their form, so I had to go get my wallet with my credit card in it. Which is something I haven’t done for a total of three days now.

Am I lazy, or am I a perfect case study of exactly what it is that we’re talking about here? Maybe a bit of both?

The fact is, there’s a payment waiting to be done that included just enough friction to get me to abandon the process.

So, the question now is, is that an incredible amount of friction?

All that’s really required of me is to stand up, walk to where my wallet is (I’m pretty sure I know where it is, but, like, what if it’s not?), take out my credit card, and then use my fingers and press keys to put numbers and letters onto a form. Once done, my package will be on its way. But, again, I’ve not done it.

Is it an incredibly monumental time-consuming task that I have ahead of me? No, not really. The whole process should take less than a minute. Is this incredibly inconvenient? Again, not really.

What’s really happening here is an expectation-vs-reality event. I have been trained by the real world to expect a certain amount of convenience, and because I’m not getting it in this process, I’m just not doing it. And I’m not alone.

The real cost of digital disconnect

We’ve looked at the problem of friction in online payments, but let’s dig deeper. Because this is a lot more than just a frustrating thing that merchants deal with—it’s something that could be catastrophic to a business.

According to data from the Baymard Institute that they sourced from 49 different studies, a staggering 70% of all shopping carts are abandoned at the checkout process. If seven out of ten people brought two pairs of slacks and a blouse to your counter, looked at you dead in the eye, and then just walked out of your store, it’s likely you’d attempt to figure out what’s going on.

The good news is that we know the reasons why people are abandoning carts because people like you are concerned about what’s happening. And they want to find ways to fix it.

Three reasons your shopping cart is being abandoned like a New Year’s resolution in February

These are three of the biggest reasons behind shopping cart abandonment.

1. Manual Entry

In the example above, Yours Truly decided to wait a while before filling out the information necessary to complete the checkout. That’s friction and it causes cart abandonment. Which means fewer sales, which means less money.

However, an absolutely staggering 72% of online shoppers still have to input their payment information manually for every single purchase. Not everyone is either savvy enough, or trusting enough to keep their info handy for autofill.

This goes even a little ways beyond friction and into the realm of unmovable obstacles. Entering that information takes time, is prone to errors, and can be downright frustrating.

If we’re really thinking about the user journey, we know that our customer got to that payment page because they’re excited about making a purchase. Now, suddenly, there are a dozen blank fields in front of them.

They go get their card, start inputting information (if they decided to go that far) and they click on the purchase button.

Oopsy daisy! They entered one digit incorrectly. Now they have to start over again. And at this point, they must just decide to not even bother.

Forcing customers into tedious, manual processes adds seconds of unnecessary friction and, as a result, you’ll drop sales like a Yankees second baseman.

Complicated checkout processes are the single greatest cause of shopping cart abandonment. And when we factor in the previously mentioned abandonment rates of 70% already, this process can cost you more than a trip to Vegas.

2. Security Fears

We’re a long way from the early days of online transactions where it seemed like no one was willing to part with their credit card information online. But building trust is still an essential aspect of business for every online merchant.

You can work on your brand reputation, you can improve your products, and you can even give your customers amazing customer service. But all that effort can be wiped out if your customers don’t trust your checkout process.

The reality is that most customers still don’t feel great about giving up their payment information to online merchants.

One study shows that 19% of online shoppers abandoned carts because they didn’t trust the site with their credit card information. And it doesn’t come out of nowhere. It’s people responding to headlines about data breaches, hacks, and identity theft that they come across as they’re doomscrolling for the fourth time that day.

They’re reading about information being stolen. They’re reading about how there were more than 3,000 data breaches in 2024 alone. These breaches exposed billions of consumer records that could, and probably were, used for all kinds of nefarious purposes.

When people read about things like this, it gives them a very real reason to be fearful. Storing credit card information on a vendor site represents a very real risk. And we see that fear manifest as friction at the payment stage.

Now you find yourself in a difficult position, don’t you? How many of your customers will choose “Guest Checkout” in order to avoid storing their information with you?

It’s nothing short of a paradox for merchants. You want to provide fast, easy checkout, but consumers may actively avoid the very means by which they can complete their checkout process faster.

It’s a problem that can’t be solved by manual entry and basic payment gateways. A solution is required that rebuilds consumer trust from the ground up.

3. Speed & Convenience

It doesn’t matter what your main focus is, if you’re someone who wants people to look at things and take actions online, then speed and convenience are non-negotiable aspects of the deal. You may have the cutest, most adorable cat videos, but if they’re not loading instantly, folks will look elsewhere for their cuteness fix.

You love statistics, so let’s make sure you get this one. A 2024 survey by Statista showed that 55% of consumers are going to abandon a purchase if the checkout process is too slow, or too inconvenient.

When we look at the effect of speed and convenience on mobile, we’re getting to a whole new level of urgency. Another study found that mobile cart abandonment rates can be as high as 85%. Add a slow connection to a tiny screen, add in environmental distractions, and you may find yourself with abandonment issues that your therapist isn’t going to be able to help you with.

If shoppers have to zoom in, scroll scroll scroll for what they’re looking for, or manually enter their details, they’re quite likely to just move on.

It’s a measurable loss of revenue you’d rather not have to add to your bottom line, given all the hard work you’ve done to get them to that cart in the first place.

In order for the payment industry to thrive in the coming years, we’ll need to provide consumers with speed, security, and simplicity.

Click to Pay is cutting through the noise

With all of the above in mind, it’s no surprise that there are a lot of people working on solving all these problems. And what would be easier than making the online shopping experience as simple as what we get in person?

Enter EMVCo, a global technical body owned by Visa, Mastercard, American Express, and others. They developed a technology called Secure Remote Connection (SRC). You’ll know it as its more common name: Click to Pay.

The goal was simple: create a payment button that is familiar, fast, and secure. And it should operate across all devices and for all merchants.

Mastercard has been a big champion of this solution since the very beginning. With Click to Pay, you get a device-agnostic, interoperable solution that works across all major card networks. Its singular goal is to make paying online as effortless as tapping your card in person.

Here’s how Click to Pay works

What if you could replace your tedious manual entry process with a single button that everyone recognizes and trusts? Click to Pay does that very thing. The implementation is simple, and we’ll look at that further down. But first, let’s look at the two foundational technologies that provide both you and the consumer with security and convenience in equal measure.

Network Tokenization

Most of you understand the idea of Network Tokenization, but let’s fill in the blanks for everyone here. What it is, at its core, is a technology that solves a critical vulnerability point: the transmission and storage of a customer’s Primary Account Number (PAN).

A PAN is a 16-digit number that everyone has on their credit or debit card. And to say that it’s a highly sensitive data element is as understated as saying that the internet is a series of tubes.

Network tokenization mitigates this risk by replacing the PAN with a unique, encrypted token that is useless outside of its designated purpose. This process is managed directly by card networks. When a consumer's card is tokenized, the network generates a token that is digitally linked to the PAN but contains no sensitive account information.

For a merchant, this means that instead of processing and storing the real card number, they are only ever handling a token. This token is designed to be useless if stolen because it cannot be used for any other purpose or with any other merchant.

The direct benefit for you, as the merchant, is a drastic reduction in your PCI DSS compliance scope. You’re not storing sensitive cardholder data, so the burden of meeting the rigorous requirements of PCI DSS are substantially decreased.

Now you’re investing less of your time, resources, and finances towards compliance audits and data security management. That’s a huge win!

To sum up, network tokenization removes the burden of storing sensitive payment data from the merchant entirely. Instead, that responsibility is on the card network. You’ve got better security, as well as more time to focus on core business operations. And you’re giving your customers a secure and simple payment experience that decreases all of the friction points you’re trying to avoid.

Intelligent Recognition

Click to Pay offers another huge advantage for merchants: the system remembers returning users, making their checkout experience even more simple.

Once a user has signed up with Click to Pay, all they need to do when they return to your site is enter their mail or phone number. The platform recognizes the user, then presents the information they’ve saved and, voila, one-click confirmation. No need to find a wallet, no need to manually enter data. They can just find the product they want and buy it with one click.

It’s taking the payment experience we’ve come to expect and recreating it online. By leveraging the inherent trust and security of card networks, merchants like yourself are able to get rid of the most significant barrier to conversion: manual entry.

You now have a better shot at repeat business with your new effortless checkout experience, but you’re also building consumer confidence. Your customers know their payment information is securely stored and instantly accessible, and now they’re happy to return to make purchases via your frictionless experience.

Do merchants really benefit from Click to Pay?

We’re not going to beat around the bush answering this question. The answer is resounding “Yes!” Click to Pay is a lot more than just a convenient way for consumers to process their payment. You’ll see a direct impact on your bottom line almost immediately.

According to Mastercard, data from early adopters is showing significant improvements over other payment technologies for three specific reasons.

1. Increased sales and conversions

We’re fighting the good fight against cart abandonment, and Click to Pay addresses the root causes, not just the symptoms. With reduced friction and a faster checkout process, merchants are seeing significant increases in conversion rates.

According to Mastercard, Cinepolis, a major Latin American cinema concern, has already seen a 6% uplift in successful transactions since implementing Click to Pay. Making checkout an easier process is turning browsers into buyers.

2. Reduced costs and chargebacks

Chargebacks are a giant pain in the butt for your business. You lose revenue, you have to pay fees, and you pay more for operational costs than you wish you had.

A lot of the chargebacks that take place come from the ironically named “friendly fraud,” in which a customer doesn’t remember that they used their card for something. When network tokenization is in place, there is a clear, trusted checkout.

The result of that is that Click to Pay can lead to an absolutely astounding 50% reduction in chargebacks, according to JustEatTakeaway.com. You’re saving more money and freeing up more resources.

But why stop here? Let’s keep going!

3. Higher approval rates

You know that there are few things that will put a bee in your bonnet faster than a declined transaction. You end up losing a sale that you worked hard to get and the customer leaves feeling like they’ve had a bad experience.

There are a lot of different things that can cause a card to decline, but the most preventable of those is outdated card information.

A customer might have a new expiration date or a new security code from a recently reissued card. Their browser might have stored old details, or they might have simply mistyped the information in their rush to check out.

Network tokenization eliminates this problem at the source. With the process being managed right at the network level, customers’ payment details are automatically updated. There is a token dynamically linked to the most current version of their card on file.

That means that every transaction is processed with accurate, up-to-date information, regardless of what your customer has stored on their device or in their browser.

If you’re interested in decreasing those decline rates, this is the way to go about it. Your average credit card transaction can have a decline rate as high as 15-20%. But by using network tokenization, you may be able to increase approval rates by three to six percentage points.

This one is the final boss of online sales, and crucial to making sure that the experience you’ve put together to get people to your checkout page actually results in a successful transaction.

Getting started with Mastercard Click to Pay

Merchants like yourself are already implementing this technology. It’s a great way to create an excellent experience for your customers, whether they’re new to your site, or are returning visitors.

To get started, you should start by assessing your current infrastructure. This will give you the information you need to look at the most efficient integration path.

Once that’s done, get in touch with us so we can show you how you can integrate Click to Pay without having to rebuild your entire checkout page. You can also use the Spreedly Advanced Vault to store and manage payment sources in a single, secure, PCI-compliant location.

Ready to future-proof your payments strategy? Get in touch with our team today.

Download the Payments Orchestration eBook Below

What is the main disconnect between physical and digital payment experiences?

While physical payments have become remarkably simple through Tap to Pay technology (with two out of three in-person Mastercard transactions being contactless), online payment processes remain complicated, less trustworthy, and cumbersome by comparison. Physical payments can be completed by simply waving a card or device over a machine, whereas online payments create friction and frustration that often resembles standing in a long line at the DMV.

What example does the blog post provide to illustrate cart abandonment and payment friction?

The author describes needing to pay duty on a package being delivered from Texas to Montreal. After receiving an email with a payment link, the author had to physically retrieve their wallet and credit card because their payment information would not autofill on the merchant's payment form, demonstrating unnecessary friction in the online payment process.

Why should merchants care about improving their online payment processes?

E-commerce accounted for $25 trillion in 2023, and merchants are losing significant opportunities due to cart abandonment caused by complicated and frustrating online payment experiences. By adopting solutions like Mastercard Click to Pay, merchants can reduce friction and better align their digital payment experience with the simplicity customers already enjoy with contactless physical payments.