.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Most businesses use payment service providers to power their financial systems.

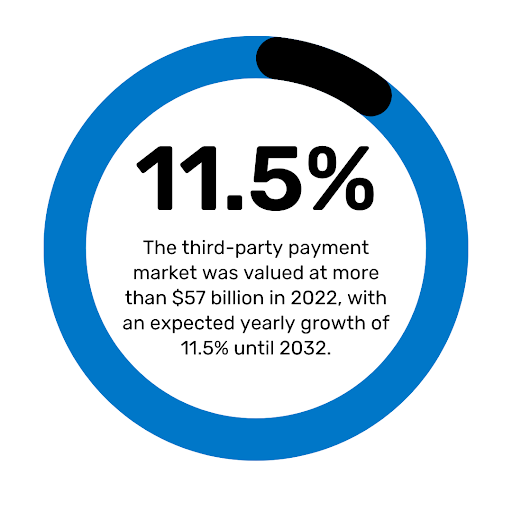

The third-party payment market was valued at more than $57 billion in 2022, with an expected yearly growth of 11.5% until 2032. Growing popularity of online transactions and convenient payment solutions are key drivers of this increasing demand for third-party providers.

Merchants and marketplaces often use third party payment processors for efficient intermediary services that make the payment process smoother and more approachable for customers. Escalating diversity in this market has given companies more options than ever when it comes to choosing the right payment processor for their needs, and in many cases, merchants are now opting for a multi-provider approach.

Third Party Payment Processors Definition

A third party payment processor allows you to accept payments without setting up a merchant account.

Funds are transferred from one account to another using the third-party provider’s technology, which acts as a technical link between the customer’s payment account and your business’s bank account. You can accept more payment methods with this type of solution as a result.

The processor securely captures and transmits customer payment details after a payment is initiated. With these details, the payment processor can verify the transaction and manage the authorization process via the relevant card networks or digital wallets. Upon approval of the transaction, the funds are settled into the merchant or marketplace’s bank account minus any processing fees the provider may charge.

Processing payments this way allows merchants to avoid having to build and maintain complex payment systems. They are also spared of having to negotiate fees directly with banks and card networks. Such negotiations are instead handled by the payment processor themselves, who also manages more complicated tasks like fraud detections and chargebacks.

Marketplaces dealing with a multi-vendor environment can rely on a third party payment processor to simplify different procedures, such as payouts. E-commerce platforms, for example, can set up automatic distribution of funds to multiple sellers without having to take on additional technological burdens. Some processors even offer extra features, like dashboards and APIs, to make payment systems even simpler and reduce the administrative overhead required from businesses.

Are They The Same as a Normal Payment Processor?

Working with a third party can be more convenient than opening a dedicated merchant account. You can accept card payments and complete onboarding much faster.

These providers pool multiple companies into a shared account structure. This aggregated approach eliminates the need for extensive administrative management and can be appealing to small-scale merchants or marketplaces.

Payment facilitators (Payfacs) offer yet another avenue for merchants to access payment services without a direct relationship with an acquirer or processor, but can have different requirements and limitations from third party processors or direct payment processors.

The differences between merchant account providers and third party payment processors

Traditional merchant account providers assign individual accounts to each business. This process often includes a more time-consuming vetting process that can take several days or weeks depending on the merchant’s risk profile and any relevant bank policies in place. The tradeoff for this slower onboarding is typically a more stable setup that can be customized precisely to the merchant’s needs.

The choice between the traditional and third-party models for merchants can influence nearly every aspect of how their payments operate.

Third parties can offer more consistent, flat-rate pricing and fees for greater cost transparency. This can become problematic if a merchant or marketplace experiences a sudden rise in sales. A traditional merchant account can offer a more tailored approach that suits a fluctuations in your payment volume.

Merchant account providers often base their pricing on factors like merchant size, payment volume, and risk profile. There may be setup fees and monthly costs to contend with but a custom pricing model can be helpful in times when you need to scale quickly.

Operational control and risk management are also key points of distinction to consider.

Businesses using a third party payment processor benefit from an all-in-one platform that handles fraud monitoring, PCI compliance, payment gateway services, and other risk management procedures.

These processors tend to have a low risk tolerance because they manage payments for thousands of merchants simultaneously. Sudden account freezes or even unexpected termination can occur if the processor detects activity that alerts their automated risk rules.

This makes account stability a notable concern for businesses in higher-risk industries or those experiencing rapid growth that outpaces their competitors.

When you opt for a merchant account provider, you typically experience fewer disruptions of this kind. They have already performed rigorous due diligence during onboarding and view you as an established client. In turn, you are less likely to face sudden restrictions or funding delays.

Third party payment processors also often use standardized online channels for customer support. These can be sufficient for simple troubleshooting but may fall short for businesses needing hands-on assistance or urgent issue resolution.

Larger payment processors can offer comprehensive documentation and scalable tools, but their personalized services may be limited. Traditional merchant account providers assign dedicated account managers that makes them better suited to businesses in need of live support.

Another significant advantage of third-party processors is their global orientation. Many of these platforms support cross-border transactions and offer built-in multi-currency support. Merchants can accept and settle payments in their preferred currencies. This feature is especially attractive to e-commerce businesses that operate in or plan to expand into multiple different regions.

Choosing between a third-party processor and a traditional merchant account really comes down to assessing factors like your business’s size, growth stage, risk profile, and operational complexity. Third-party processors excel at reducing entry barriers and enabling rapid deployment, especially for marchants and marketplaces testing new products and regions. As we’ll discuss later, the most profitable and operationally efficient solutions often come from adopting a multi-provider approach.

Third Party Payment Processors Examples

Third party payment processors come in all shapes and sizes.

Different providers offer distinctive services and capabilities. It’s important to consider your options before locking in with any specific brand.

For example, Stripe offers both payment processing and payment gateway functions. Both capabilities are integrated into the Stripe platform from which merchants and marketplaces can access these services. Stripe also supports a large mix of payment methods and currencies that can facilitate expansion efforts.

Another provider offering both payment processing and payment gateway capabilities is PayPal. PayPal is a preferred provider for many global businesses. The provider offers very broad support across more than 200 countries and regions. PayPal has even earned the title of most popular digital wallet in the U.S.. CapitalOne Shopping Research reveals 71% of U.S. adults have used PayPal.

Further reading: Check out our full comparison of Stripe and PayPal.

Other Types of Payment Processors

We’ve already discussed third-party payment processors and merchant account providers.

To recap, third-party processors allow merchants to accept payments without the need for a dedicated merchant account. This offers an easy setup and low barrier to entry but can come with higher transaction fees and less overall control of funds. Merchant account providers offer dedicated accounts for accepting card payments, giving more control and stability in exchange for more complex onboarding and administrative processes compared to the alternative.

These two options are not the end-all, be-all for payment processing, however.

Modern advancements in payment technologies have paved the way for full-stack processors that can offer both payment gateway and payment processing services, like we detailed above with Stripe. A full-stack process can integrate these capabilities into a unified platform that simplifies the management of a payment system and can consolidate administrative processes like reporting.

Sometimes, payment aggregators can also offer payment processing services, though aggregators are typically more focused on the settlement and fund transfer processes.

The best type of payment processing solution might just come from open payments platforms.

Open payments platforms offer some of the best payment processing solutions because they prioritize flexibility and scalability. They do not limit integrations to a specific provider and are designed to work with as many APIs and third-party services as you need. You can add custom checkout experiences and connect to multiple providers without committing to a specific processor.

An open payments platform allows developers to build new features and integrations without the need for a single provider’s roadmap. You can create a payment stack that precisely matches your needs and business goals.

Growing merchants and marketplaces with complex requirements benefit greatly from the level of control and interoperability that open payments platforms can provide. Such platforms enable efficient adaptability when it comes to payment processing.

Why You Can’t Rely On Just One Payment Processor Alone

Relying on a single payment processor can expose merchants and marketplaces to significant operational and strategic risks. While using one provider may simplify setup and management, it also creates a single point of failure. If that provider experiences technical outages, service disruptions, or policy changes, it can directly impact revenue flow and customer experience.

This level of dependency limits a merchant’s ability to negotiate terms, adapt to changing market conditions, or serve a broader customer base with diverse payment preferences.

A multi-processor strategy offers greater resilience and flexibility. The ability to integrate multiple payment service providers allows merchants to route transactions intelligently based on criteria such as the cost, approval rate chances, or geographic location for each individual transaction.

Much like the multi-provider payment gateway strategy, choosing a solution that lets you integrate multiple payment processors can exceptionally improve your global coverage and give you the support you need as a growing company. You can meet the changing expectations of customers in different regions with ease without having to rework your entire payment setup.

This not only optimizes transaction performance but also improves redundancy and protects your business continuity in the event of a processor outage. It enables you to tap into local processors that may offer better acceptance rates or regional payment methods.

A diversified payment stack also greatly strengthens your negotiating power.

With a multi-provider approach, you are not locked into the policies or pricing of a single provider and can make data-driven decisions for your business. For marketplaces in particular, supporting multiple processors also allows for more tailored onboarding flows for sellers in different countries or risk profiles.

Spreedly Helps You Connect Multiple Processors to Your System

At Spreedly, we’ve built our open payments platform around the concept of connectivity.

Our Connect solution gives you the freedom to integrate as many tools and providers as you want from our wide selection of partners. Connect adds a layer of payment orchestration to your tech stack that simplifies the configuration and management of your chosen payment services.

The Spreedly platform as a whole is built on a single and normalized API that is easy to integrate. Best of all, you can experiment with different providers to find what works best for each of your business and payment scenarios without ever disrupting the customer experience.

We also streamline your administrative workflows by providing a unified view of your payment services. From our platform, you can access, monitor, and manage your connections from one place.

Contact our team today to get started.

Download the Payments Orchestration eBook Below

What is a third party payment processor and how does it work?

A third party payment processor allows you to accept payments without setting up a merchant account. It acts as a technical link between the customer's payment account and your business's bank account. The processor securely captures and transmits customer payment details, verifies the transaction, manages authorization through card networks or digital wallets, and settles approved funds into your bank account minus processing fees.

What are the advantages of using a third party payment processor instead of a normal payment processor?

Third party payment processors are more convenient than opening a dedicated merchant account because you can accept card payments and complete onboarding much faster. They pool multiple companies into a shared account structure, which eliminates the need for extensive administrative management and is particularly appealing to small-scale merchants or marketplaces.

Why would a marketplace use a third party payment processor?

Marketplaces dealing with a multi-vendor environment can rely on a third party payment processor to simplify different procedures, such as payouts. E-commerce platforms, for example, can set up automatic distribution of funds to multiple sellers without having to take on additional technological burdens. Some processors even offer extra features like dashboards and APIs to further reduce administrative overhead.