.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

This is a refresh of an article originally published on September 11, 2024 with new information added to reflect recent changes in the industry.

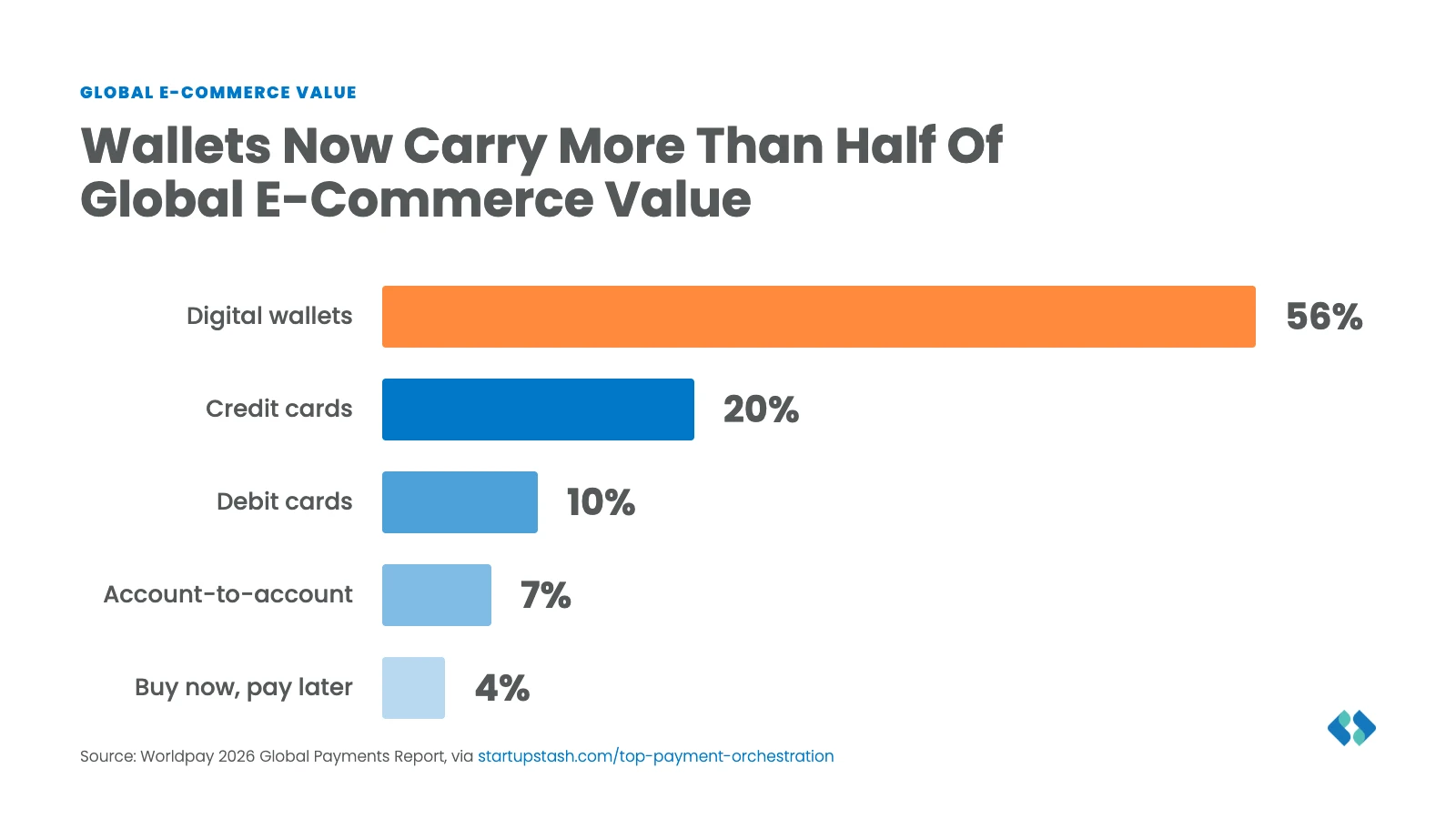

Digital wallets now account for 56% of e-commerce value. Credit cards sit at 20%, with debit at 10%, account-to-account payments at 7%, and buy-now-pay-later at 4%. Two years ago, cards were still the default. Now they're a minority payment method, and the gap keeps widening.

That shift is why payment orchestration keeps showing up in more merchant conversations. A checkout built around one or two acquirers can't keep up when customers expect Apple Pay, Pix, SEPA Direct Debit, and a growing list of local wallets all to work the same way. Merchants need a layer that can add and swap payment methods without a rebuild every time preferences change.

The mechanics that made orchestration valuable, card-on-file tokenization, rules-based routing, 3DS management, haven't changed. What's new in 2026 is who initiates the payment. AI agents are starting to complete purchases on their own, and the businesses that own their payment data are the ones who can adapt to that without renegotiating their entire stack.

The 2026 payment mix: wallets pull ahead of cards

The numbers above come from Worldpay's 2026 Global Payments Report, and they explain a lot about why "add a payment method" requests have gotten more frequent and more varied. A merchant that only supports cards is turning away a majority-share segment of global buyers before checkout even loads.

The vendor side is consolidating to match. This year alone has seen a cross-border payments acquisition valued at $2.75 billion, aimed at bundling multi-currency accounts, real-time settlement, and stablecoin processing into a single relationship. The pitch is convenience: one vendor for everything. The tradeoff is the same one merchants have run into before with single-acquirer setups, just at a larger scale. When your payment methods, your token vault, and your settlement all live inside one bundled platform, switching any piece of it later gets expensive.

Card on file, routing, and 3DS: the mechanics haven't changed, but the stakes have

These three areas were the technical core of payment orchestration in 2024, and they still are. What's different is how much more traffic runs through them now that wallets and alternative methods dominate the mix.

This isn't theoretical. US Trans Corp runs its payment stack on Spreedly's orchestration today, and that stack sits inside Microsoft Dynamics 365, giving Microsoft customers a modern, open payments layer for accounts receivable and collections.

Card on file needs more than a stored token

Embedded payments are the default in e-commerce checkout, and card-on-file flows are the foundation. The hard part was never storing a PAN. It's that every card network has its own rules for telling customer-initiated transactions apart from merchant-initiated ones, and getting that distinction wrong causes declines and disputes.

Orchestration handles this by vaulting the network transaction ID and any authentication tokens alongside the payment method itself, and by standardizing field mapping across providers. That combination is what keeps recurring billing and one-click checkout working reliably as a merchant adds more gateways.

Smart routing and cascading solve different problems

These two get lumped together, but they do different jobs. Smart routing decides where a transaction goes in the first place, using BIN data, geography, and real-time provider performance to pick the best gateway before the transaction is even attempted. Cascading kicks in after a decline, retrying the same transaction on a second gateway to recover it.

A merchant running only cascading is treating every decline the same way, regardless of whether it was a soft decline worth retrying or a hard decline that won't change on a second attempt. Pairing upfront smart routing with targeted cascading for soft declines is what actually moves the recovery rate. Automatic failover during an outage and rules-based re-routing for cost or strategic reasons both build on the same routing logic.

3DS still needs to work across regions differently

3DS supports SCA requirements under PSD2 in the EEA, but it's also used elsewhere purely for fraud mitigation and liability shifting. Orchestration lets a merchant run one integration and one API call to manage 3DS outcomes across both SCA and non-SCA markets, and to store authentication results for reuse in later transactions, whether they're customer-initiated or merchant-initiated.

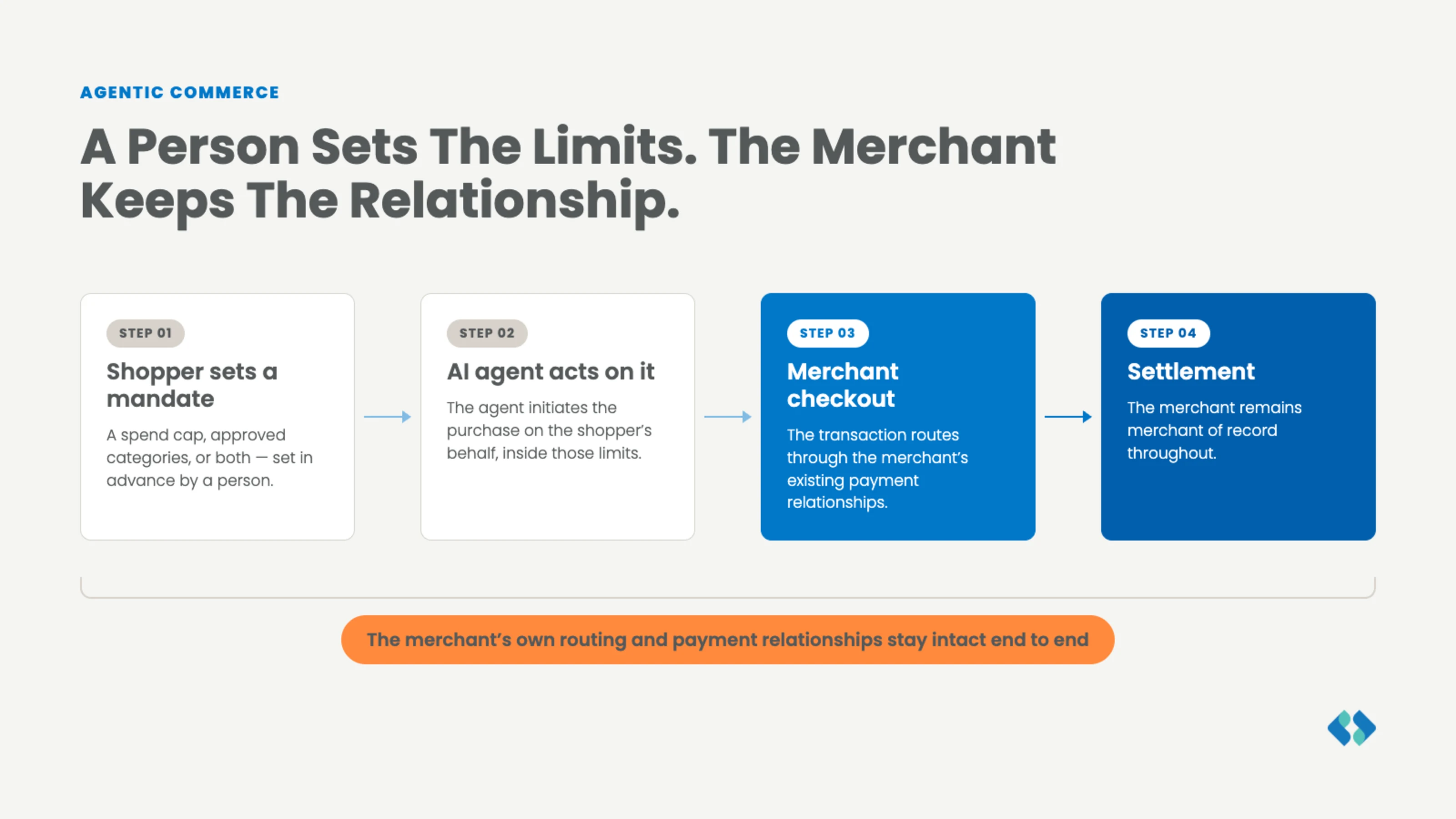

Agentic commerce is live, and it changes who initiates the payment

The newest complication isn't a payment method. It's a new kind of buyer. In July 2026, a live proof-of-concept ran on Visa's rails where an AI agent completed a purchase on a shopper's behalf, authorized across multiple issuers and constrained by spend caps the shopper had set in advance. That's a meaningful jump from AI as a shopping assistant to AI as the party actually completing checkout.

Visa, Mastercard, and American Express are all building this into their core payment infrastructure now rather than treating it as a future project. Getting there requires merchants to identify, govern, and route machine-initiated payments separately from standard e-commerce traffic, since an autonomous agent's mandate and an individual shopper's checkout aren't the same request even when they end in the same charge.

The trust question is still open. Consumers are more comfortable with AI recommending what to buy than they are with AI actually paying for it, and closing that gap needs its own framework: verifiable mandates, identity checks, and reputation scoring for agents, not just for the humans behind them.

This is exactly what Model Context Protocol support is built for. Spreedly's agentic commerce work lets agent-initiated transactions flow over a merchant's existing payment relationships, so the merchant stays the merchant of record and keeps its routing logic intact rather than handing that off to whatever platform the agent runs on. If you're setting up MCP for the first time, our developer's guide to MCP covers the implementation details.

Why token ownership decides how fast you can move

Incredibly, 93% of companies don't actually own their payment tokens. Their tokens live inside whatever PSP issued them, which means switching providers later means re-tokenizing an entire customer base, a project most merchants avoid until they're forced into it.

A provider-agnostic vault solves this by separating token ownership from any single processing relationship. The token belongs to the merchant, not the gateway that happened to generate it, so adding a new acquirer or dropping an underperforming one doesn't require touching stored payment methods at all. That portability is what makes multi-acquirer routing possible in practice instead of just in theory, and it's the same reason agentic commerce needs a merchant-owned vault: an AI agent's mandate should attach to a payment method the merchant controls, not one locked to a single processor.

Getting ready for PSD3 and PSR before mid-2026

The EU's Payment Services Regulation is in its final legislative stages, with publication expected around mid-2026, and it turns several best practices into requirements. Verification of payee, an IBAN-to-name check, becomes mandatory for account-to-account flows to cut down on authorized push payment scams. Fee transparency rules get stricter, requiring clear, itemized cost breakdowns rather than bundled totals. And merchants need to preserve a path to human customer support rather than routing every dispute through an AI chatbot.

None of this is a reason to panic, but it is a reason to treat fraud controls and compliance workflows as something you can audit, not just something you configured once and left alone. Merchants running orchestration with built-in reporting are better positioned here, since the reconciliation and audit trail requirements assume you can produce clean records across every provider, not just your primary one.

What you need to know today

The fundamentals of orchestration, tokenized card-on-file, smart routing paired with cascading, unified 3DS, are the same ones that mattered in 2024. What's changed is the traffic running through them: a majority-wallet payment mix, AI agents that can initiate a purchase on their own, and a regulatory deadline that turns "we should probably own our tokens" into a requirement instead of a nice-to-have.

The merchants in the best position for the next 12 months are the ones who already treat their payment data as their own asset, not something that lives inside a vendor relationship they'd have to unwind to change. If you're evaluating whether your current setup gets you there, see a demo.

What is payment orchestration and how does it help maximize transaction success?

Payment orchestration is an intelligent payment management approach that harmonizes revenue through optimized payment processing. As demonstrated by Spreedly's platform, orchestration uses data-driven optimization to ensure both compliance and revenue growth, allowing merchants to expand their payment stack reach and maximize transaction success rates.

What does it mean to own your payment tokens?

Owning your tokens means your payment methods are stored in a vault you control, independent of any single processor. If you don't own them, switching payment service providers means re-tokenizing your entire customer base instead of just redirecting traffic.

How does payment orchestration help reduce the complexity and cost of managing multiple payment providers?

Payment orchestration, as implemented through Spreedly's platform for US Trans Corp, minimizes complexity and cost by intelligently managing multiple payment providers in a unified system. This multi-provider strategy is integrated into platforms like Microsoft Dynamics 365 and helps reduce unnecessary chargebacks, system complexity costs, and PCI compliance burdens while improving communication between businesses and customers.