.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

In our past article, Cash me if you can: simple steps to lower your credit cards decline rate, we extensively discussed the problem of declined transactions. We discussed that when factors such as the lifetime value of a customer and abandoning a credit card are taken into account, the consequences of declined transactions go way beyond a lost sale.

In the same article, we also discussed the complexity of payment processing; from a customer's lack of funds, payment gateway settings, and fraud predictions to technical issues, there are many things that can make transactions decline.

To fight this problem, we explained that there are few things merchants can control, including adjusting their gateway settings and making sure the credit cards stored in the card vault are valid (not stolen, lost or expired). We introduced Account Updater as a main tool to make sure the account information is up to date.

But how does AU perform in real world?

What does Account Updater (AU) do?

Simply put, AU is a service provided by credit card brands that updates customers’ account information stored in their card vault. According to MasterCard:

[AU] helps reduce card-not-present (CNP) transaction declines caused by changed account numbers and expiration dates resulting in a better customer experience.

VISA states that AU benefits merchants by reducing service cancellation, simplifying and securing account-on-file transactions, strengthening customer relationships, lowering churn and cutting customer service costs. It also benefits customers by eliminating the need for direct action, facilitating uninterrupted service and reduces the negative experience of declines.

How impactful is AU?

Spreedly started offering AU service to its customers almost a year ago. From the beginning, we were curious about how impactful this service has been on the cards stored in our card vault. To answer this question, in this blog post we look into payment methods updated by AU and compare the decline rate changes before and after the update.

By studying the transactions before and after the update we show how AU can lead to a significant improvement in decline rates, consequently leading to increase in revenue and stop loss. In particular, we use the data for two example customers in different industry segments and show how they have each benefited from this service.

What happens after AU?

According to Spreedly documentation, one of the following messages are returned with any AU update:

MessageCard Updated?What's Next?% of TotalReplace Payment MethodYesEnjoy!44Invalid Replace Payment MethodNoEither a new card number or expiration date are invalid1Close Payment MethodNoThe account is no longer open and should no longer be used.13Contact Card HolderNoContact the cardholder for a new number, and/or expiration date.43

The first column in the table above is the message, the second column indicates if the card was actually updated with new updated information, the third column recommends the next step, in particular if the card failed to be updated, and the last column is the ratio of each message in Spreedly's vault. For example, 44% of the cards have been successfully updated with new information while 13% of the accounts have been closed.

As you can see from the table above, merchants can immediately benefit from AU by simply stopping processing the cards that are tagged by either InvalidReplacePaymentMethod, ClosePaymentMethod and ContactCardHolder in the card vault as the accounts are invalid, closed or require contacting the card owner. In fact, 55% of messages received compose one of these three types. Making sure they are not processed before further action can save many potential declines.

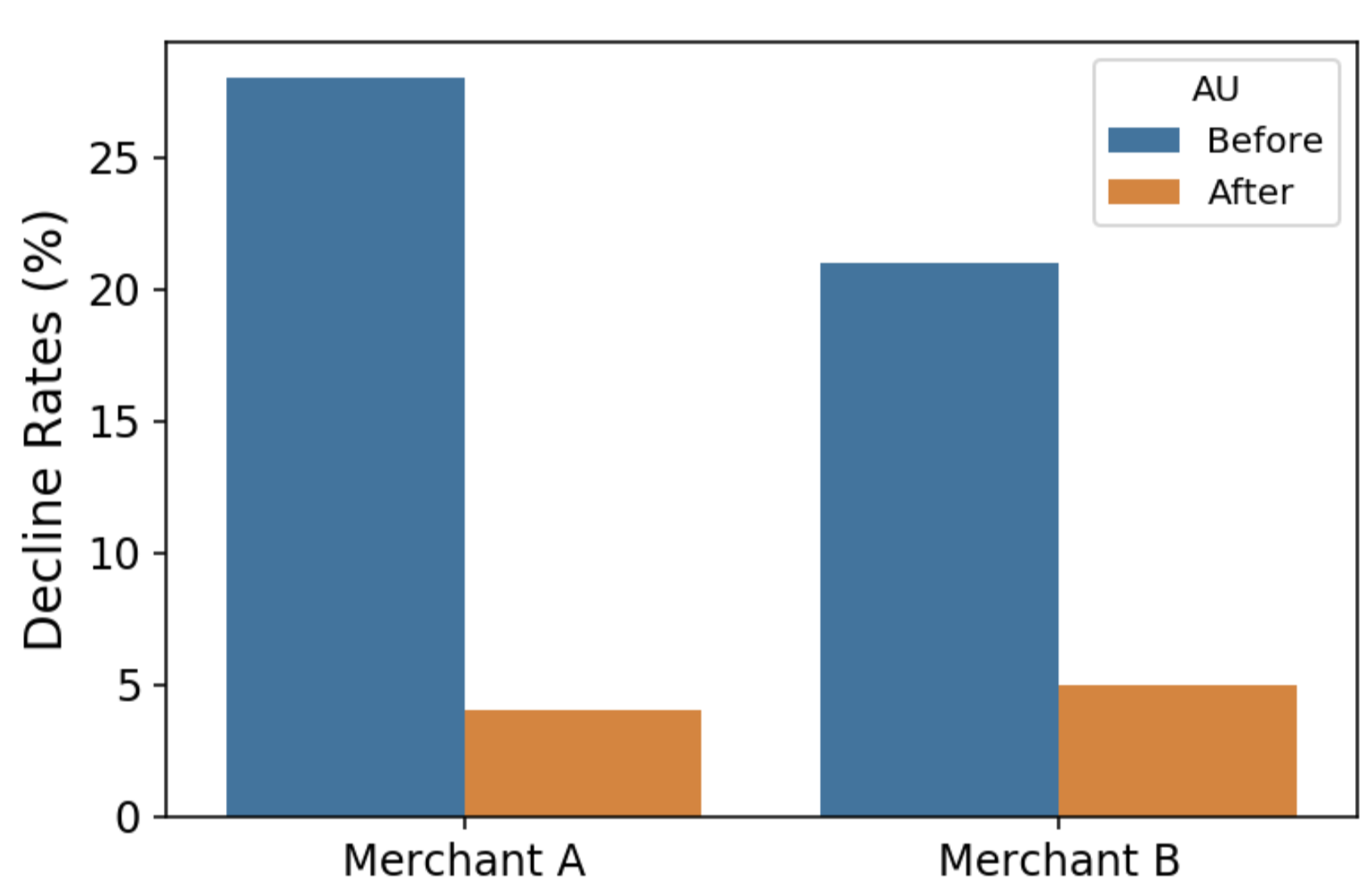

A tale of two merchants

Here we compare the decline rates between the last transactions made by cards before AU and their first transactions after AU. We limit this part to the payment methods that were updated successfully, ReplacePaymentMethod.

The data from two of our customers that belong to different industry segments are used. While these two business are different, they both store payment methods on Spreedly's card vault to use for one-time or recurring transactions.

The table below shows the changes in the decline rates for purchases made on these two platforms before and after accounts were updated (only updated payment methods are considered here):

Both merchants observe a significant decrease in their decline rates, which as we mentioned above saves revenue and at the same time customer satisfaction and avoids redundant friction in the payment process.

While the results may vary for different organizations, based on how old their card vault is and how often you update your customer's accounts the decline in a decline rate is a trend we observe among the transactions from the payment methods that have been updated by AU.

Download the Payments Orchestration eBook Below