.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

For merchants who accept card payments, interchange fees can often be a costly factor to consider.

In 2021 alone, merchants in the U.S. paid a total of $137.83 billion on processing and interchange fees — resulting in a more than 24% increase compared to the year prior.

Interchange fees can be a major expense for merchants, especially those who have not optimized their payment systems. Keeping interchange fees low requires a combination of best payment practices, optimized checkout experiences, and a trustworthy payment system.

This article aims to dissolve some of the mystery surrounding interchange fees, including what they are, how they are calculated, and why merchants need to pay them.

Keep reading to learn how Spreedly can help lower your interchange fee expenses.

What are Interchange Fees?

An interchange fee is a fee a merchant must pay to a bank when a credit or debit card payment is processed. Banks charge these fees to help cover the costs of payment processing, which includes payment acceptance and authorization as well.

According to Bankrate, interchange fees can range in average costs between $0.20 to $0.65 per transaction. However, these fees depend on which type of card you are using, as well as whether or not the transaction is covered by the interchange fee standard.

The interchange fee standard is a standard put forth by the Federal Reserve Board to regulate interchange fees and ensure fees are not overly expensive. Exemptions to the interchange fee standard are available to debit card issuers with assets that total less than $10 billion.

On the topic of the interchange fee standard, the Federal Reserve states:

“The Board’s Regulation II provides that an issuer subject to the interchange fee standard (a covered issuer) may not receive, for any electronic debit transaction, an interchange fee that exceeds $0.21 plus 0.05 percent multiplied by the value of the transaction, plus a $0.01 fraud-prevention adjustment, if eligible.”

Factors that Impact Interchange Fee Costs

Numerous factors come into play in determining the cost of interchange fees for a merchant. In general, interchange fees are typically worth 1% to 3% of the total transaction. The rate includes a flat rate, as well as a percentage of the payment value.

Some of the key factors that can impact the cost of an interchange fee include:

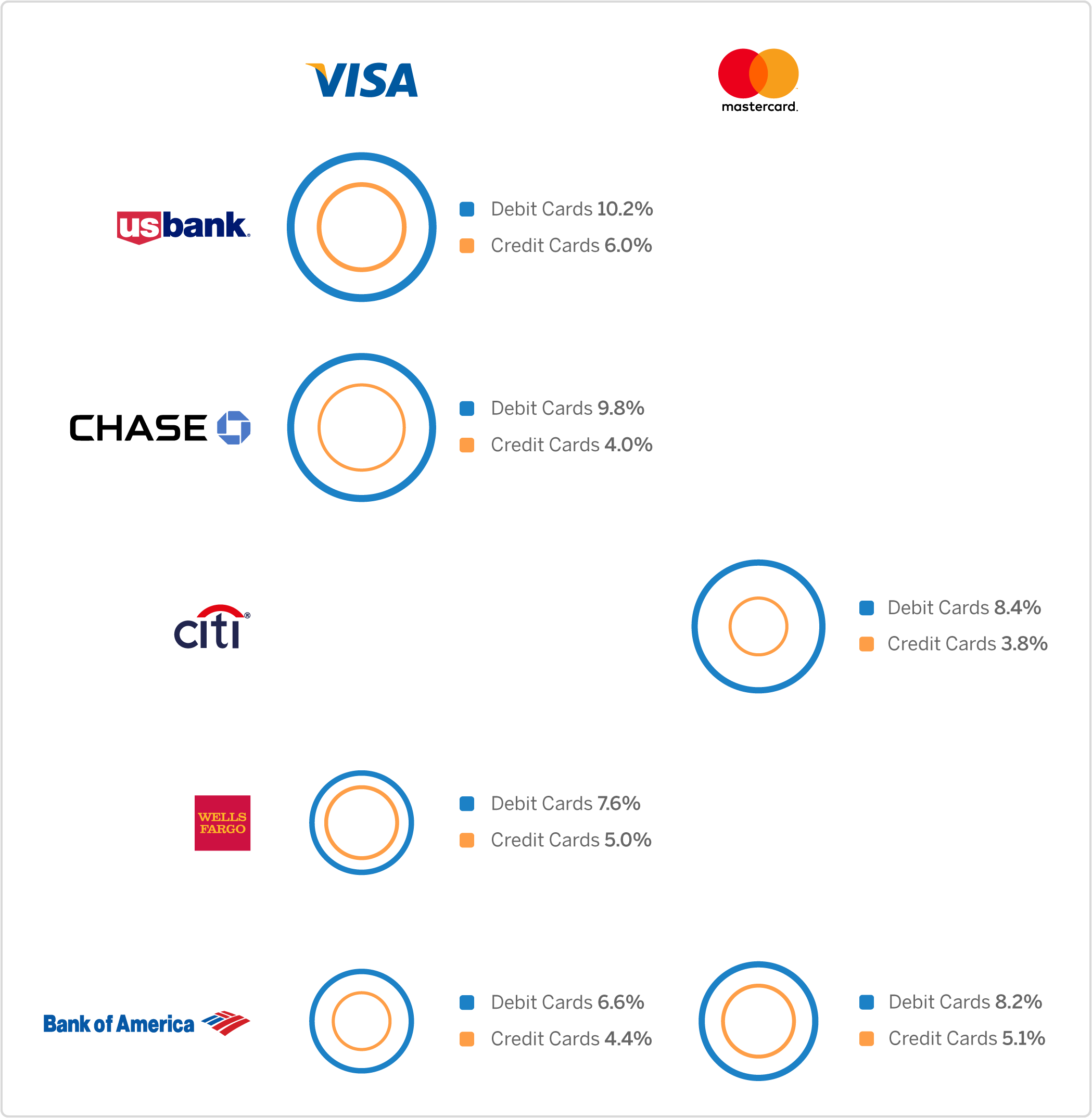

- Transaction Type: Interchange fees vary depending on if a payment is made with a credit or debit card, with credit card transactions typically accruing heftier interchange fees. These fees can also vary depending on the card type as well. For instance, Visa is known for having lower interchange fees thanks to the widespread accessibility of Visa payments.

- Online vs. Offline Processing: The type of processing involved in a transaction impacts the interchange fee, as different tools and resources are needed for different types of processing. Online processing almost always offers lower interchange fees, as a greater portion of the process is automated and requires less manual intervention.

- Merchant Industry: Certain industries are subject to higher interchange fees due to an increased risk of fraud, chargebacks, and other payment problems. Examples of industries that may face higher chargeback fees include nightclubs, cannabis, and gambling.

- Payment Frequency: Some card issuing companies charge varying interchange fees depending on whether a transaction is a one-time payment or whether it is a recurring payment. Generally, recurring transactions have lower overall interchange fees.

Why Do Merchants Have to Pay Interchange Fees?

When a transaction is processed, many behind-the-scenes activities take place.

As mentioned earlier, interchange fees are charged by banks to help cover the costs of payment processing. These costs can also include fees from the card payment network (MasterCard, Visa, etc.) and the payment gateway that the merchant is working with.

Although interchange fees include a flat rate, they can vary in total costs due to also charging for a percentage of the total sale. Additionally, the interchange fee a merchant has to pay is dependent upon the interchange fee rates of the specific card company.

In a broad sense, paying interchange fees is simply a part of business in which merchants pay financial service providers for their services. However, in recent years, regulators have worked to reduce interchange fees and prevent financial service providers from charging outlandishly expensive fees.

Additionally, most financial service providers will offer varied fee programs that offer different pricing models in exchange for key benefits, such as discounts or memberships.

Optimizing Interchange Fees as a Merchant

Interchange fees have long been a burden on merchants. Even as regulators work to make interchange fees more affordable for merchants, many merchants still feel as though they are losing out.

However, there are ways to optimize your interchange fees as a merchant.

- Optimizing Checkout: As a merchant, you have little control over whether or not a customer uses a debit or credit card. Despite this, there are ways to encourage customers to use debit cards, particularly by way of optimizing the checkout experience. By focusing on streamlining checkout processes into a frictionless experience, merchants can better encourage the use of debit cards and enjoy lower overall interchange fees.

- Following Provider Requirements: The payment network you are working in will publish its rates, fees, and requirements for interchange fees (for example, look at The Visa System webpage for Visa’s interchange fee information). These requirements will often include specific authorization and identity verification activities that are essential for ensuring secure transactions and are required for lower interchange fees.

- Avoiding Downgrades: Whenever a merchant fails to follow the requirements of their payment network, a transaction can be downgraded — and downgrades result in increased interchange fees. Some of the top reasons why a transaction can be downgraded include a lack of Address Verification Service (AVS) to verify the cardholder’s identity, a faulty POS terminal, and a lack of additional required data.

- Including More Data: Speaking of data, it can often be in the best interests of a merchant to provide more data than is required of them for a transaction. Merchants can reduce the costs of interchange fees by including Level II and Level III data with each submitted transaction. This additional data can include information such as sales tax, accounting codes, dates, and more.

- Settling the Same Day: Many merchants opt for batching transactions for settlement to streamline their settlement process. However, it is crucial to always settle transactions within the same day to maintain lower interchange fees.

Spreedly Helps Lower Interchange Fee Expenses

As a merchant, working to optimize and lower interchange fees takes extra time and resources that you may not have readily available.

Spreedly’s payment orchestration services utilize network tokens to optimize payment transactions and provide merchants with the ability to work across multiple payment service providers. Plus, merchants have the flexibility to choose between a network token or a secure, vaulted PAN token with Spreedly.

Using Spreedly’s network tokens, merchants can not only lower interchange fees but also drive higher authorization rates, improve security, and reduce fraud.

Accelerate your growth as a merchant today by getting started with Spreedly.

Download the Multiple Payment Gateways eBook Below

What is an interchange fee and why do merchants have to pay them?

An interchange fee is a fee that a merchant must pay to a bank when a credit or debit card payment is processed. Banks charge these fees to help cover the costs of payment processing, which includes payment acceptance and authorization. According to the blog post, interchange fees can range in average costs between $0.20 to $0.65 per transaction, depending on the type of card and whether the transaction is covered by the interchange fee standard.

What was the total amount U.S. merchants paid in processing and interchange fees in 2021?

In 2021 alone, merchants in the U.S. paid a total of $137.83 billion on processing and interchange fees, which represented a more than 24% increase compared to the year prior.

How do credit card and debit card transactions differ in terms of interchange fees?

Interchange fees vary depending on whether a payment is made with a credit or debit card, with credit card transactions typically accruing heftier interchange fees. The fees can also vary depending on the specific card type—for example, Visa is known for having lower interchange fees thanks to the widespread accessibility of Visa payments.