.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

At the risk of stating the obvious, credit card acceptance rates are vitally important for merchants. Credit card acceptance rates can differ based on a number of variables, one of which is geographical region. In this post, we compare acceptance rates across three regions: Europe, the US and Latin America.

There are two helpful approaches when sharing data like this: a completely aggregated abstract view, or a very specific merchant view. For this exercise, we'll focus on the former.

A few important notes about our data: First, we're using roughly 6 months of data from the second half of 2019. Next, we concentrated on Visa, Mastercard, and American Express card brands. As a last point of reference: we looked at domestic vs international transactions, in addition to credit card vs debit card transactions .

Ok, on to the data!

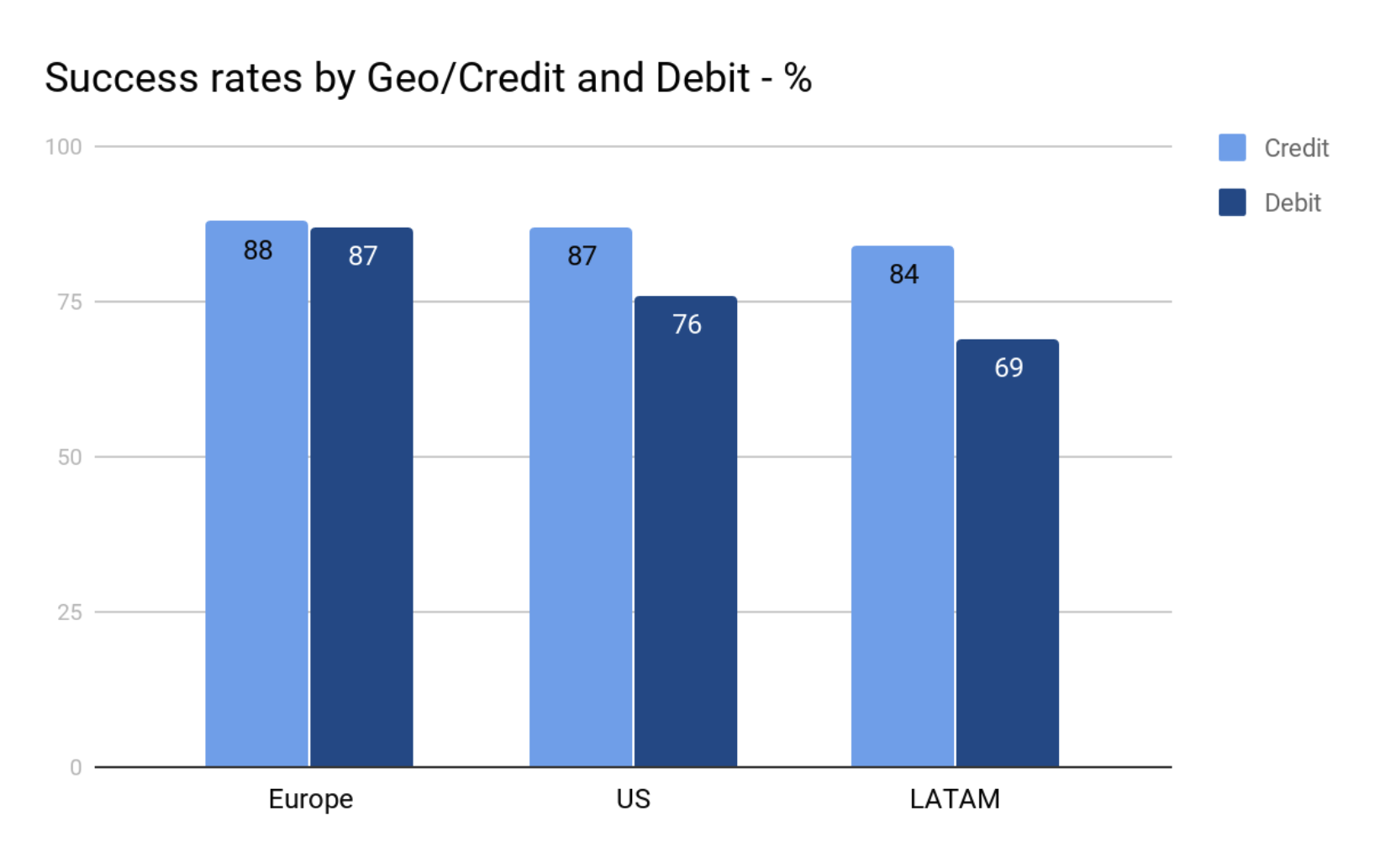

Here is a big picture of success and failure rates by credit and debit across the three regions:

We see impressive consistency at the credit card level, and meaningful variation at the debit card level.

Next, let’s look at card type success rates across the three regions.

Visa and MasterCard are largely similar, except in Europe. AMEX is consistently higher, which is not uncommon to see. As an aside: I always think of this when I see merchants who refuse to accept AMEX due to perceived higher transaction costs.

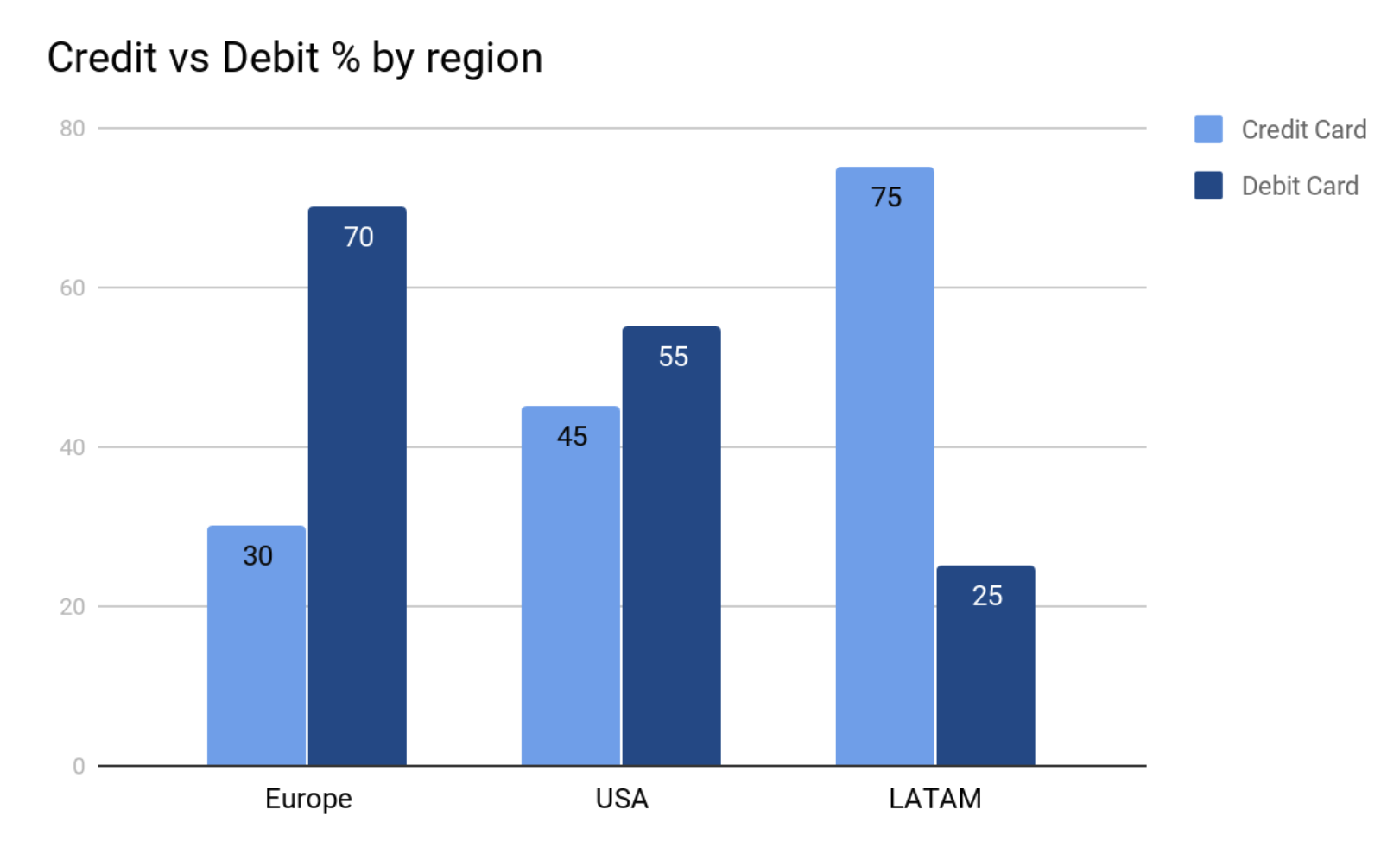

Finally, let’s focus on the mix between regions, specifically as it relates to debit vs credit card usage.

What’s most noticeable is that Europe and LATAM switch places in regard to the transaction volume on credit cards vs debit cards.

These findings also present more questions to answer in the future. For example: if we analyzed each country in Europe to compare credit vs debit - what would we find? If we took a deeper look at LATAM countries, would we see large variations across the region? We'll set out to answer those questions future posts. We're also planning to show the difference between in-country (domestic) card transactions and international (cross-border) ones.

Have questions about this research? Reach out to us at datascience@spreedly.com with questions and we’ll get back to you.

Download the Payments Orchestration eBook Below

What time period and card brands were included in this 2019 regional breakdown?

The analysis used approximately 6 months of data from the second half of 2019 and concentrated on three card brands: Visa, Mastercard, and American Express.

What were the key findings regarding credit card acceptance rates across Europe, the US, and Latin America?

The data showed impressive consistency in credit card acceptance rates across the three regions, while debit card acceptance rates showed meaningful variation. Additionally, AMEX consistently had higher acceptance rates compared to Visa and Mastercard.

What notable difference was found between Europe and Latin America regarding payment types?

Europe and Latin America switched places in regard to transaction volume on credit cards versus debit cards, meaning one region had higher credit card usage while the other had higher debit card usage.