.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

With more than 100 million transactions processed across 100 gateways in 100+ currencies, Spreedly has access to a wealth of information about payment methods (credit cards, ApplePay, PayPal, etc.), transactions and gateways performance. Using this unique dataset, Spreedly is committed to using the power of data analytics to generate insights for all participants in the payment world.

In our first blog post [Spreedly blog,], we provided a general overview of the effect of expiration dates on credit card decline rates and reported our observation of longer expiration dates for American Express and Discover cards compared to VISA and MasterCard in the Spreedly vault. We suggested that the longer expiration dates might encourage subscription-based companies to facilitate American Express and Discover cards, despite the fact that they have higher transaction fees.

This article is a birds-eye view of transaction declines rates in currencies with the highest decline rates, in comparison with the transaction decline rates for the most popular currencies in our vault. Our most popular currencies are United States Dollar (USD), European Nation Euro (EUR), Great Britain Pound (GBP), Australian Dollar (AUD) and Canadian Dollar (CAD). For these currencies, as well as those with highest decline rates, the decline rate over time and amount, and the average amount of declined transactions, are studied and compared.

In a payment's journey, when the customer makes a first time purchase, we do Spreedly-side tokenization then submit the transaction information to the payment gateway of the merchant's choice (Figure 1) which is then sent to a payment processor, credit card company, merchant and customer's banks, etc.

.

There are several things including technical problems that may go wrong after the transaction leaves Spreedly, all of which could result in a decline. On the customer's side, and according to

, making an international purchase, exceeding the credit limit, expired cards, and even missing credit card payments can stop the payment from going through. The transaction may also get declined in the processing stages due to, for example, fraud prevention. First time purchases from a new merchant, unusually large amounts, international transactions and transactions from high fraud zip codes can all cause legitimate transactions to be declined. All these errors, reported to Spreedly by gateways, are categorized as payment_processing_failed in our database. The goal of this article is to study the payment processing failure for different currencies.

Zero-ing in on Currency

One of our popular use cases at Spreedly is merchants going international. There are two approaches: trying to find a single gateway that will take you global, or striking up new relationships in certain regions. Adding new currency support can expand your target customer base. However, international transactions carry new challenges too. We decided to drill in deeper and look at decline rates by currency. For the sake of simplicity, we focus on Purchases in transaction types.

Table 1 shows the percentage of successful and unsuccessful purchases among all currencies in our vault. Since not all the possibilities like pending purchases are considered, it does not add up to unity. The 25% decline rate in overall purchases in the past couple of years is a significant number. To investigate the possible underlying reasons, let's breakdown this number for different currencies and transaction amounts.

Table 2 represents the currencies with the highest ratio of failed to total purchases. With 73% of failure in processing purchases, South Africa is the top country list. Columbia, Mexico, Brazil, Peru, and Guatemala belong to Central and South America. In Asia, on the other hand, only Indonesian Rupiah (IDR) makes it to the top 10. The presence of European countries like Switzerland, Norway, and Denmark sounds surprising and need further analysis. The largest number of transaction failures, however, belongs to Mexican Peso (data not shown).

In fact MXN is the only currency with more than a million failed transactions. Comparing our list with the list of

On the other hand, with only 6% failure, United Arab Emirates currency (AED) has the lowest failed to total transaction ratio. New Zealand's Dollar (NZD) is the second after AED with 11% failure rate. (It should be noted that in this analysis, only currencies with more than three thousand transactions are considered, which most of the currencies lie well above.)

The popular currencies in the Spreedly vault, including USD, EUR, GBP, AUD and CAD, Table 3, do a good job in keeping the decline rates low. Among them, CAD, with only 13% failure rate, does a better job compared to the other competitors. EUR has a 25% failure rate while for GBP it is only 15%. After EUR, USD with 20%, has the highest failure rate.

Time

Payment systems are dynamic systems impacted by internal and external events. Seasonal shopping holidays and very large individual breaches at a large merchant are just two examples that can impact success and decline rates.

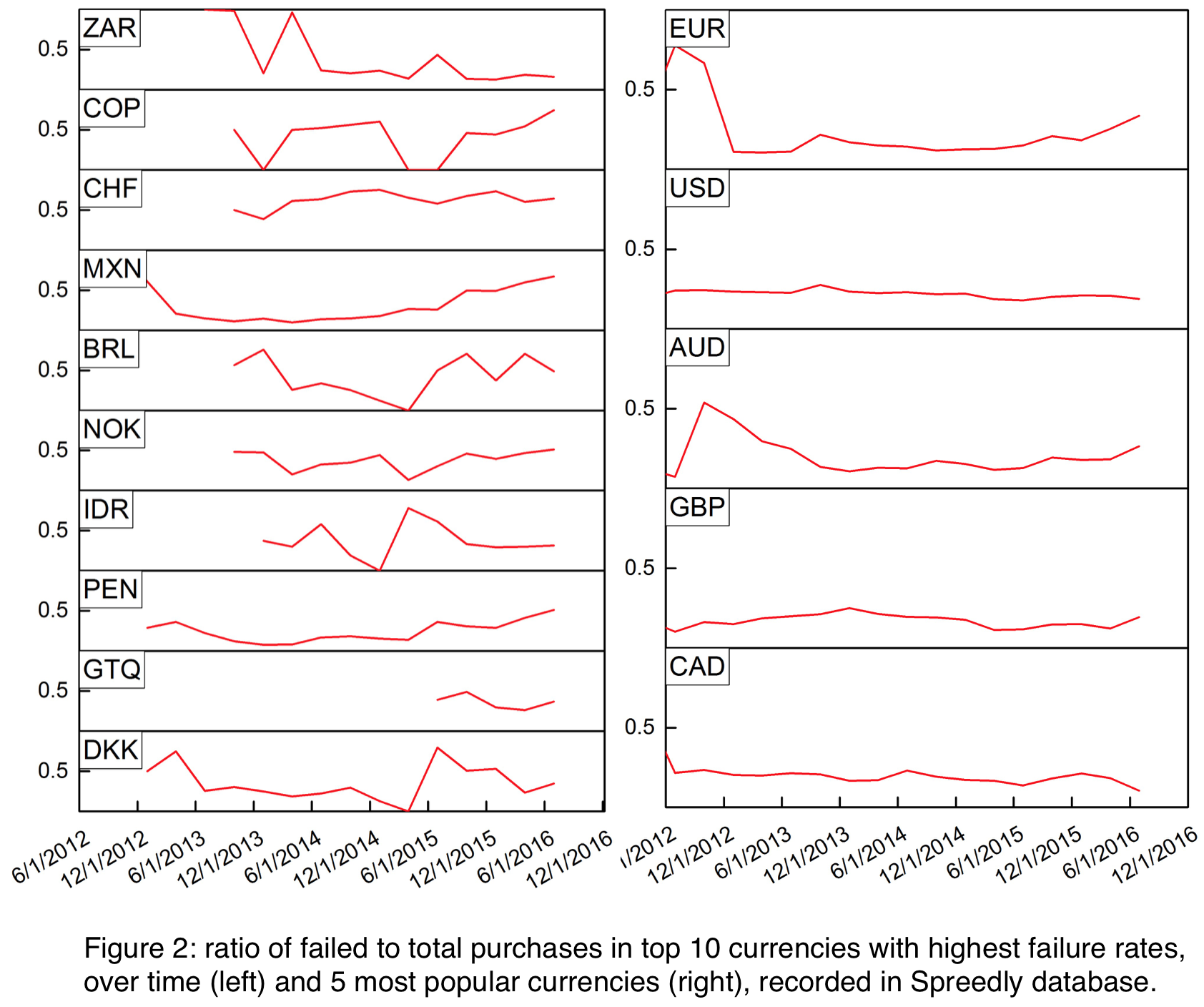

To see how the decline rates change over time, we plotted the ratio of failed vs. total purchases every three months from June 2012 to July 2016. Figure 2 will help us understand the potential improvements or regressions in payment processing over a four-year time period.

For the South African currency, ZAR, as the currency with largest percentage of failed vs. total purchases, the decline rate experiences a substantial reduction from > 90% in late 2013 to around 15% in mid-2016. Therefore, while ZAR owns the overall largest declines, its decline rate has dropped down to the decline rate of the best currencies in our database. Therefore it is safe to say ZAR has become a reliable currency for making purchases. On the other hand, as seen in Figure 2-left, the failure ratio for currencies of Peru (PEN), Mexico (MXN), Norway (NOK) and Switzerland (CHF) are upward, indicating that the ratio of successful purchases is decreasing in these currencies over time. GTQ has a short lifetime in our vault so we cannot make any conclusion about it. Also, currencies like DKK or BRL fluctuate and do not have a definitive trend in positive or negative directions.

The decline-over-time for popular currencies has a different story. USD, GBP and CAD experience very little fluctuation over time. While EUR and AUD start with a spike in their failure rates, they both drop down quickly and remain stable. All these currencies fluctuate well below 0.5, as seen in Fig. 2-right. The little fluctuations could be due to the existence of excellent infrastructure for these currencies compared to less popular currencies.

Also, Spreedly has a much larger data pool to draw on with these major currencies, meaning no one individual large merchant can impact our overall country experience. That may not always be the case with some of the other countries on our list. Among high failure transactions, Swiss Franc has the most similar behavior. The only difference is it fluctuates around 0.5 which is way higher than what more popular currencies experience.

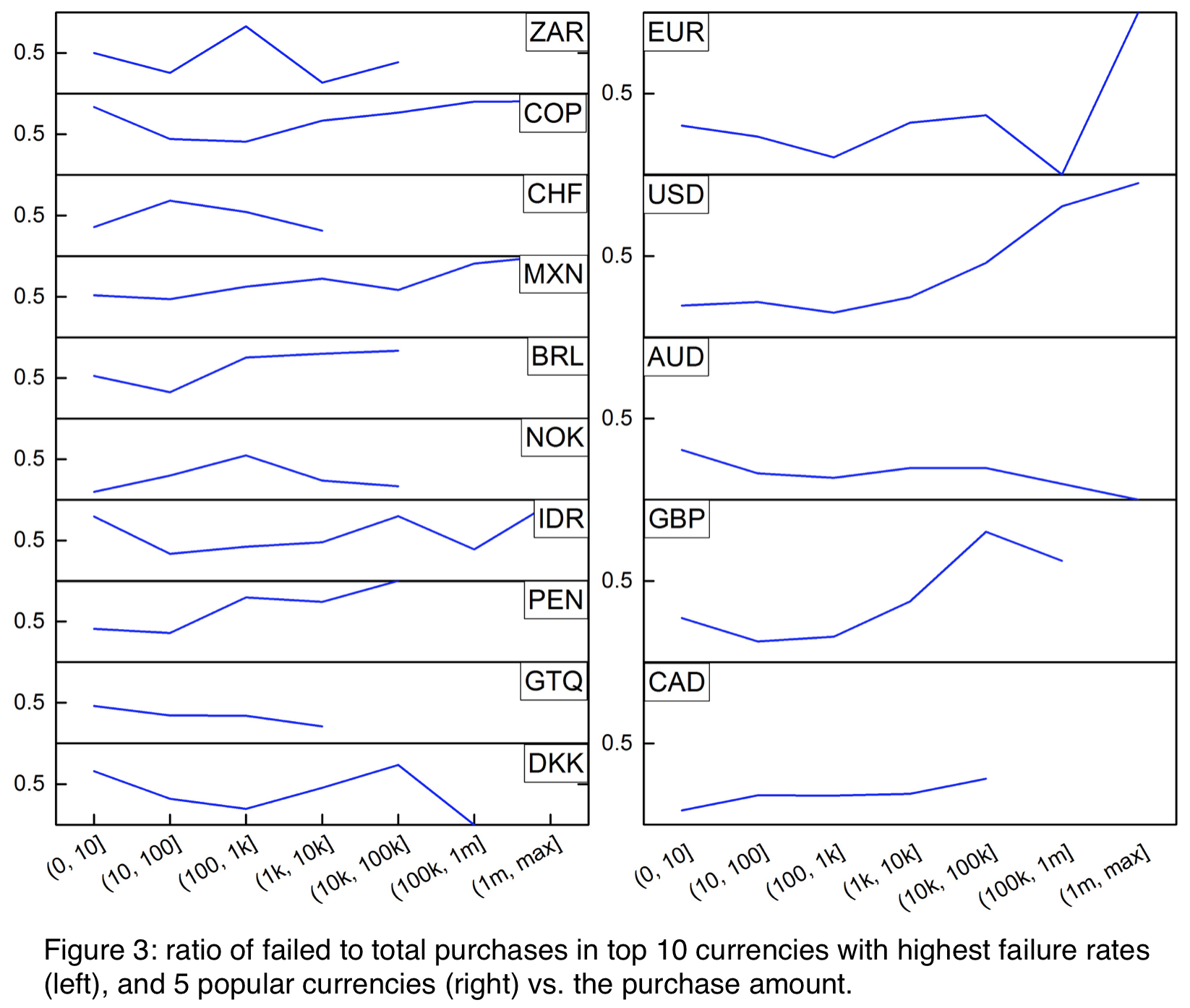

Does Basket Size impact failure rates? Are there any meaningful relationships between transaction amounts and failure rates? One may expect that the higher the amount of the transaction, the higher the chance of failure. To investigate this, we plot the ratio of failed over total purchases for amount in the ranges of 0 to 10, 10 to 100, 100 to 1k, 1k to 10k, 10 k to 100k, 100k to 1m and finally from 1m to the maximum values for the top 10 currencies with highest failure rates and 5 popular currencies (Figure 3). k and m denote one thousand and one million, respectively.

For most of the currencies in Fig. 3, the failure rate increases for higher transaction amounts, confirming what we expected. This increase is, however, more evident for the currencies on the right side of Fig. 3, except AUD. This, in turn, could imply that declines in popular currencies are more likely to be related to fraud activities while in 10 currencies with highest decline rates, it will be due to other reasons including technical problems, gateways failure, lack of enough funds, etc.

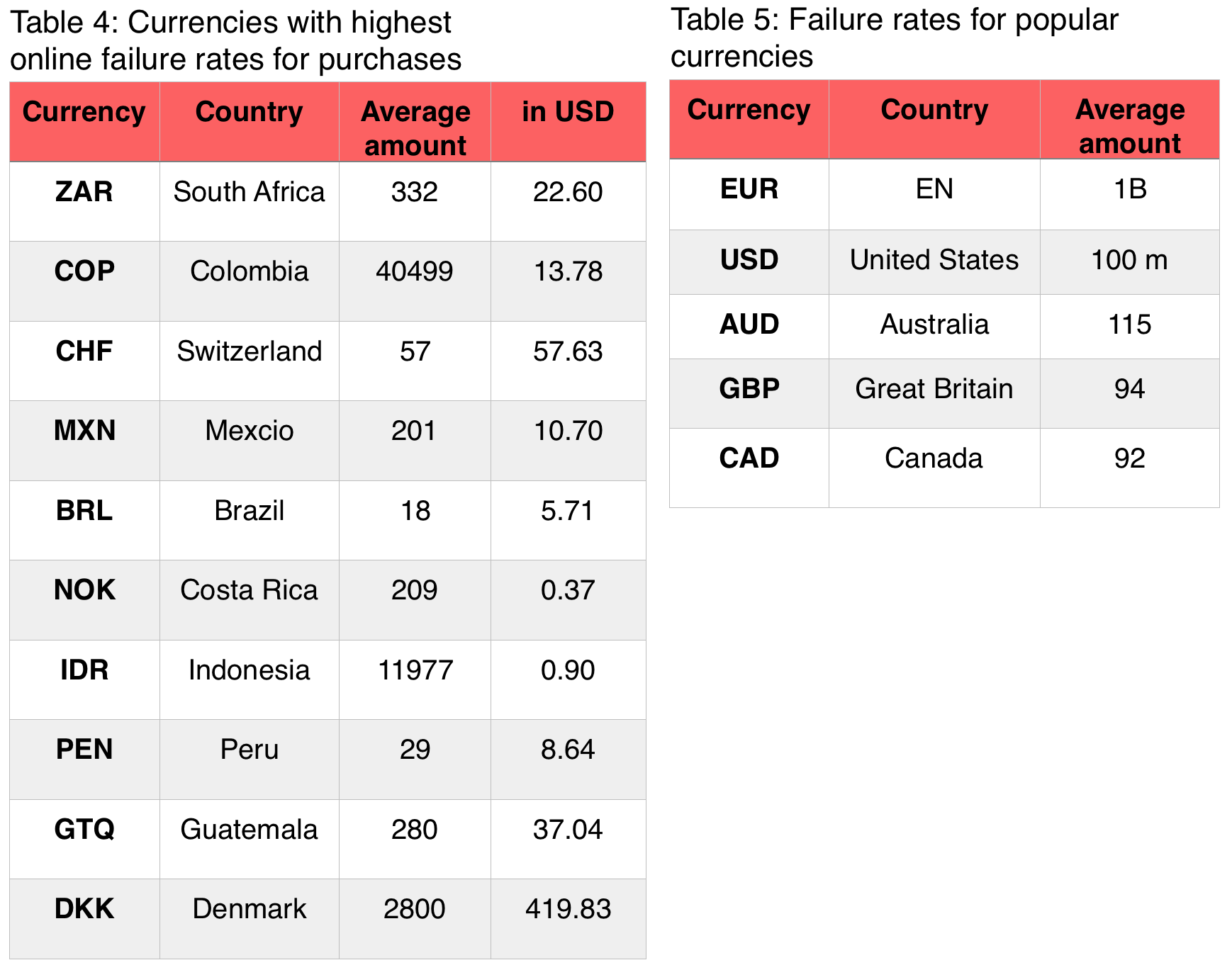

Finally, it is interesting to calculate the average amount of failed transactions in different currencies (Table 4 and 5). To get a better idea about the amounts in different currencies, the right column in Table 4 presents the average blues in USD. The amounts are well below 100$ for all the currencies in Table 4 except Danish Krone (DKK). In contrast, we have very large values for USD and EUR in Table 5.

By performing statistical analysis, and using methods like boxplot, we can show that these large numbers are most likely outliers. However, we keep them here to show the reader an idea about the range of values stored in the database.

In summary,

1. A variety of technical and non-technical reasons can lead to a decline of a transaction, after it is submitted to a gateway payment.

2. Most of the currencies in Spreedly's vault with high decline rates belong to countries in Central and South America.

4. The time evolution of decline rate diagrams of top-declined currencies is different from popular currencies. The former has more fluctuations and can be related to technical issues while the latter are mostly flat and can be related to fraud preventions. The average amount of declines provides more evidence for this hypothesis.

5. In general, AED, and among popular currencies in Spreedly's vault, CAD had the lowest decline rates.

6. In most of the currencies studied, the higher the amount, the more likely the transactions to get declined.

Expanding your prospective customer base by increasing the currencies you support is a great way to drive additional revenue. However, as you branch into new markets, your overall experience could be greatly impacted by such factors as which currencies you support and the average ticket size of your sales. Our recommendation is that when evaluating which new markets to enter, add a section around understanding the dynamics of online credit card processing in that region to the more commonly researched factors such as cultural fit, language support and customer support hours etc.

If you're a Spreedly customer, we're happy to help you with that research. If you'e not, hopefully your payment gateway can share some specific data with you.

Download the Payments Orchestration eBook Below

What was the key finding from Spreedly's first blog post about credit card expiration dates?

Spreedly observed that American Express and Discover cards have longer expiration dates compared to VISA and MasterCard in their vault. They suggested this longer expiration might encourage subscription-based companies to facilitate American Express and Discover cards despite their higher transaction fees.

What are the most popular currencies tracked in Spreedly's vault?

The most popular currencies in Spreedly's vault are United States Dollar (USD), European Euro (EUR), Great Britain Pound (GBP), Australian Dollar (AUD), and Canadian Dollar (CAD).

What are some reasons why a customer's first-time purchase might be declined during transaction processing?

First-time purchases from a new merchant can be declined due to fraud prevention systems. Common triggers include unusually large transaction amounts, international transactions, and transactions originating from high fraud zip codes, even when the transactions themselves are legitimate.