.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

By Shoresh Shafei, Justin Benson & Nathaniel Talbott

We are excited to start mining Spreedly's data - we have quite a lot of it - to surface interesting insights, trends, and if possible actionable results for merchants, payment gateways, and even consumers. While perhaps not as flashy as data science for luxury brands, we suspect there are a lot of kindred souls that find payments data as interesting as we do. Who doesn't like getting better at making money?

As an independent credit card vault that allows our customers to route payments to their preferred payment partners, Spreedly facilitates online payments via more than 100 payment gateways and third party API's in over 100 countries. With greater than 10 million credit cards stored, and working with hundreds of customers in different industry segments across the globe, Spreedly has unique access to a database of vaulted payment methods and executed transactions that can be used to start exploring important questions in the payment industry in order to help us all make smarter, data-supported decisions

In a series of blog posts, we will use data analytics to address challenges our customers face that might also be of broader interest to the e-commerce and payments industry. What is the average lifetime of a credit card? Should companies, particularly subscription or "one click payment" e-commerce services, care about card types (i.e. Visa vs. MasterCard)? What can companies do to keep their vaulted payment methods clean and up to date? How do you reduce credit card decline rates?

Our first foray is in an area near and dear to subscription-based companies: customer churn related to lost, stolen, or expired cards. Services like Visa's North American Account Updater can help with the problem, but they don't cover all brands in all regions. So, what measures can merchants take to reduce credit card declines to improve their churn?

There are a number of different approaches, but for this post we will focus on one particular area: the average expiration likelihood of a credit card once it hits the Spreedly’s vault. Expiring cards are a major driver of revenue churn and customer support/sales costs - no one likes chasing down customers for an updated card. Understanding how cards expire can help us design for renewal success from day one

As a startup, the pace at which cards are being stored in Spreedly is accelerating rapidly. In fact, 70% of all the cards stored in our vault have been added in just the last 12 months. That means we should represent a pretty "fresh" batch of cards when looking at our vault. One notable exception is that we do imports from other payment providers on behalf of merchants; in such cases we're inheriting a set of data into our vault that is of unknown age.

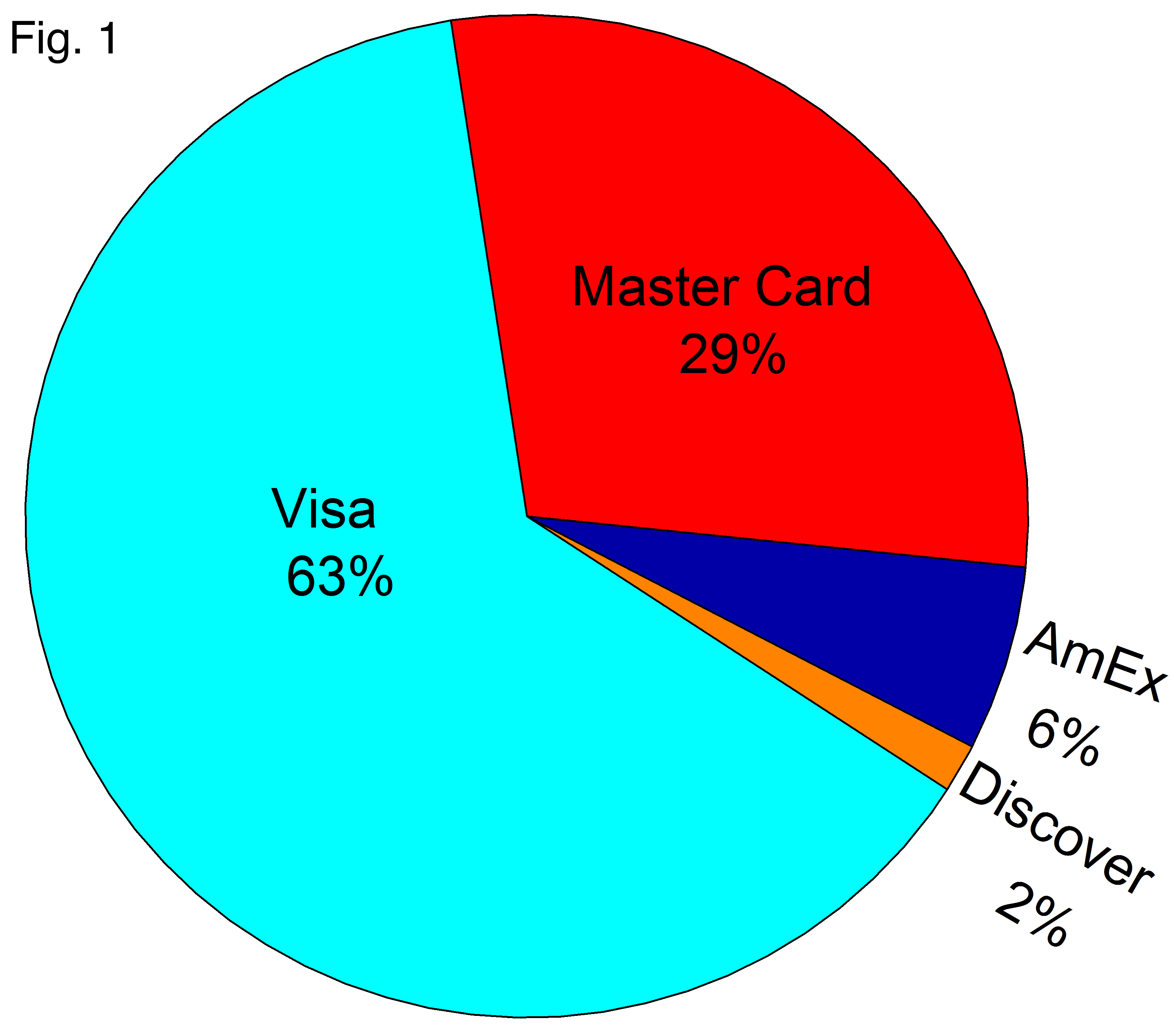

In Spreedly's vault, Visa is the dominant card type (Figure 1). Visa cards comprise 63% of credit cards stored. MasterCard has 29% with American Express (denoted as AmEx in figures) at 6% and Discover card 2%.

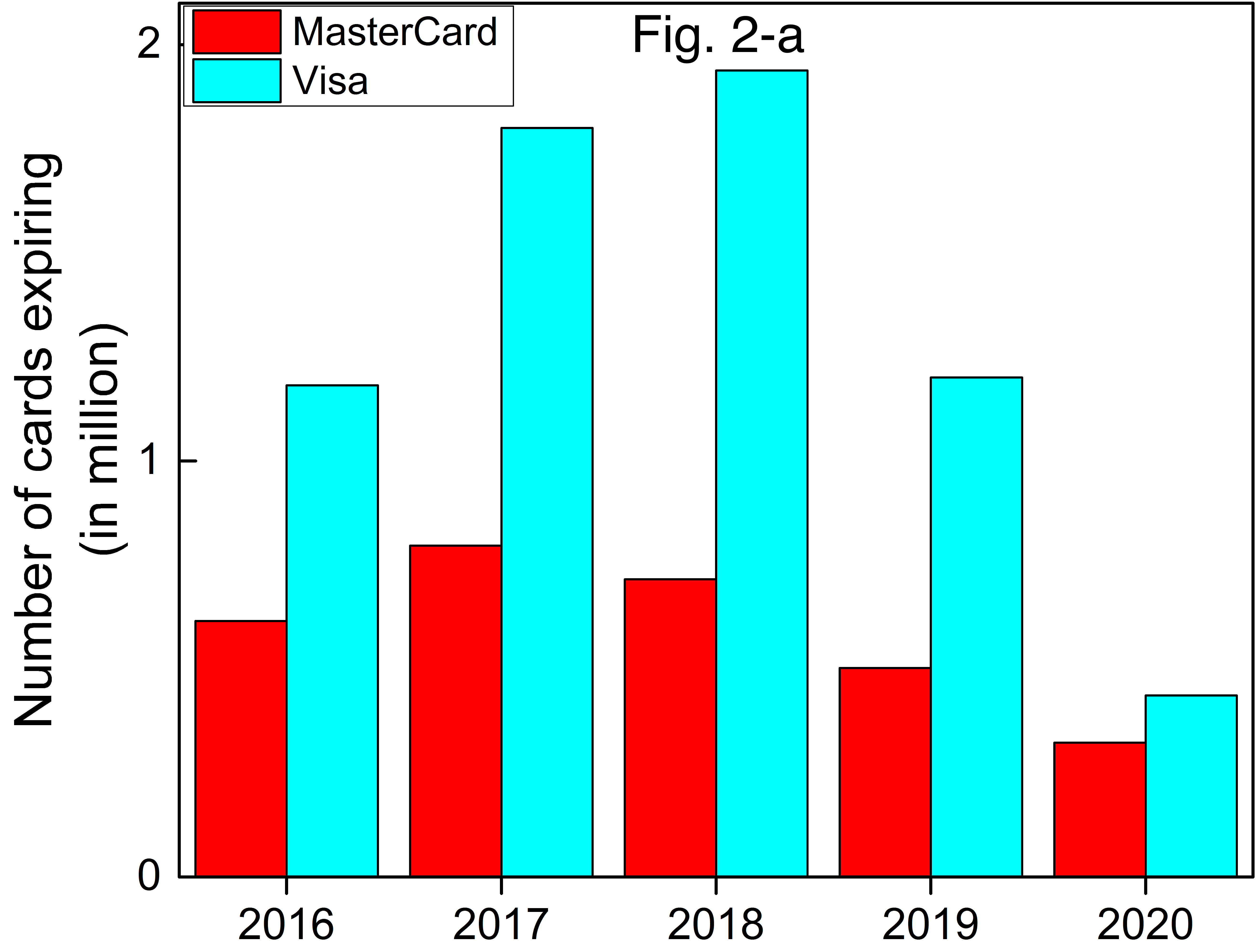

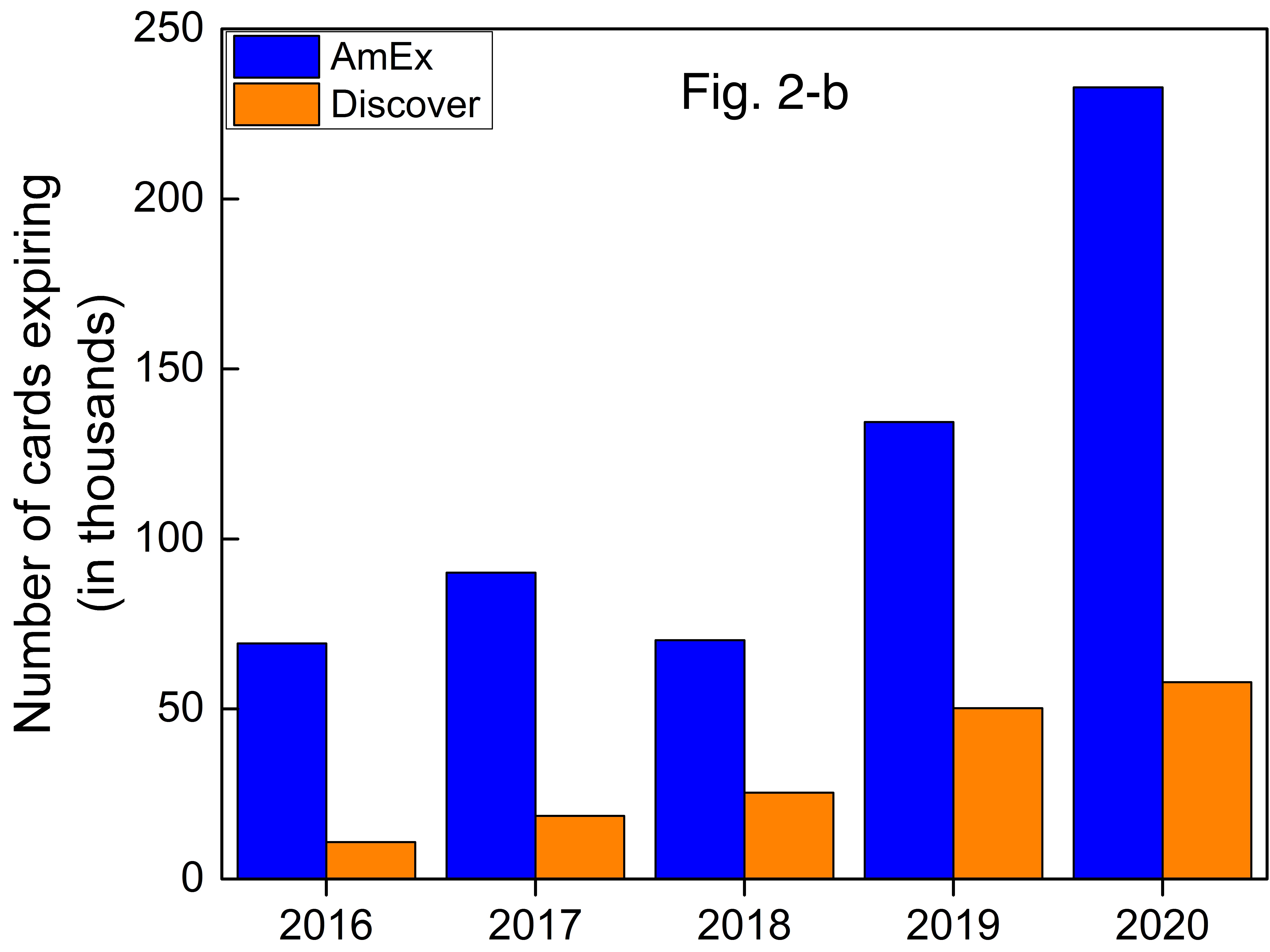

Even with our "fresh" vault, millions of these cards will expire in the next 24 months. Figures 2a and 2b demonstrates the total number of cards in the next 4 years: just in in 2017 and 2018 alone more than 4 million cards in Spreedly's vault will expire.

The bad news for our merchants is that not all cards are created equal! The bulk of Visa and MasterCard brands in our vault expire in 2017 and 2018. MasterCard expirations peak in 2017 while Visa peaks in 2018. So, the expected lifetime of a MasterCard stored in Spreedly is ~14 months while for Visa it's ~ 21 months.

We can see a much longer expiration window for the other brands we're evaluating: ~ 34 months for American Express and ~35 months for Discover. This indicates that merchants should be less concerned about interrupted subscriptions due to expiring cards for customers using those brands. Meanwhile, merchants with more Visa and MasterCard branded cards may want to consider action to guarantee continued and uninterrupted service to their customers.

One of the most interesting insights from this analysis is that it calls into question the common belief that merchants should encourage customers to use credit cards with lower fees. For example, many merchants discourage usage of American Express cards due to the higher processing fees associated with those cards vs. the more common Visa and MasterCard. Subscription or repeat commerce services that have employed that strategy may wish to revisit it - after confirming with their internal data - since those lower processing costs could be coming at the expense of customer churn.

We think it's important to point out that to the best of our knowledge there is not a fixed range between issuing and expiration dates and the expiration dates for credit card companies are determined based on a variety of parameters including the applicant's credit worthiness. Consequently, one cannot deduce a general rule that American Express and Discover have longer life expectancy than the other two; rather, we're only noting interesting trends in Spreedly's data set.

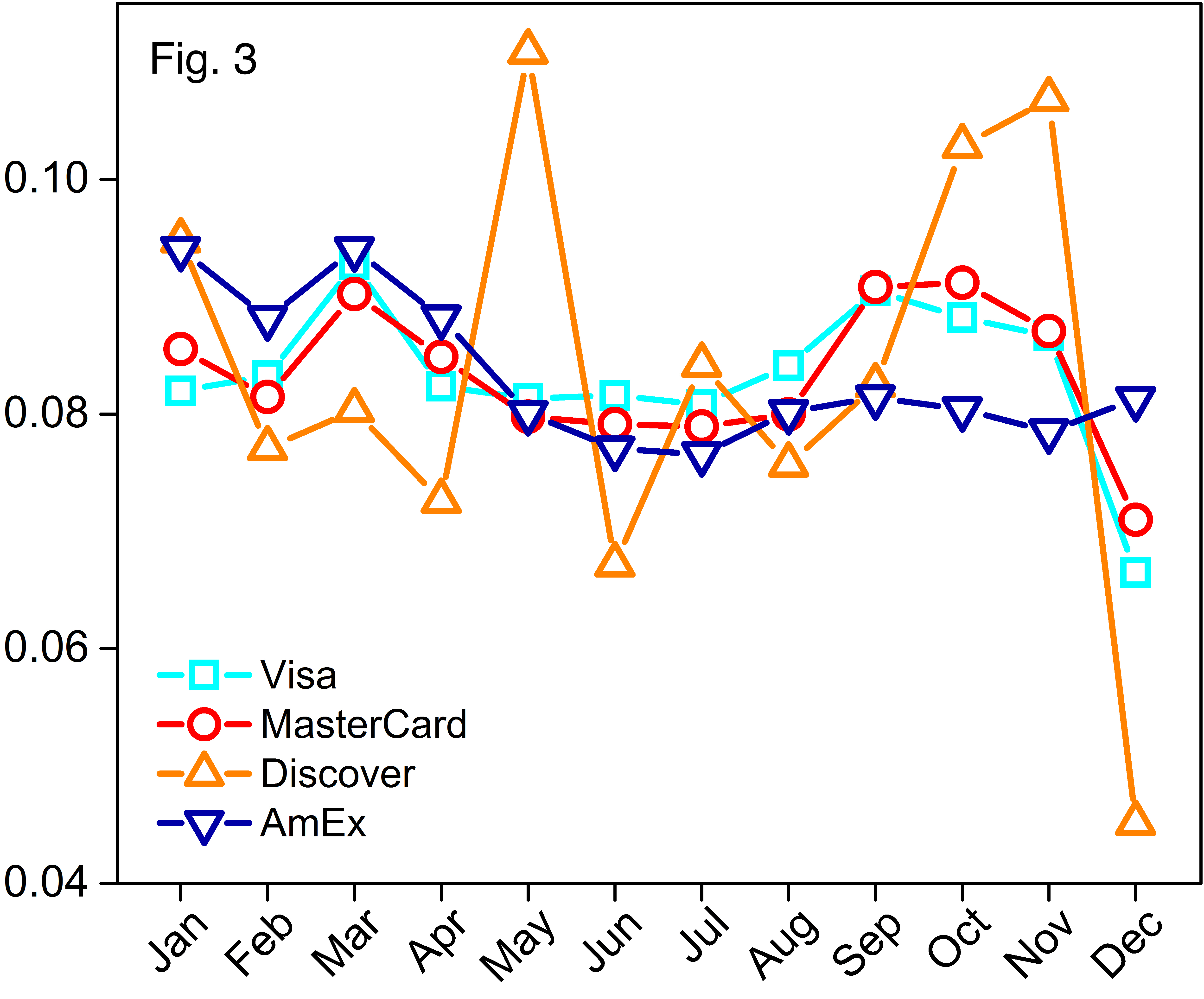

Having looked at how long until an average card expires, we wondered if there might be any other trends around expiration that could help merchants better manage their vaults. What we found is that there are distinct patterns around which months cards expire in. For each credit card type, figure 3 shows the ratio of the total number of that type expiring at a particular month per its total number in Spreedly's vault.

It appears the expiration months tend to peak twice a year at 6 month intervals: Visa and MasterCard both peak in March and October, while Discover peeks in May and November. The least fluctuation in expiration month belongs to American Express which drops down from ~9% per month for the first couple of months to less than 8% for May to December.

Another noticeable fact is the downward trend of cards expiring in December. While 11% of Discover cards expires in May, this ratio bottoms down at 4% in December. We observe a similar trend for Visa and MasterCard: the smallest percentage of expirations takes place in December. Does this reflect a credit card issuer strategy to avoid masses of expired cards in the biggest shopping season of the year? We hope to further examine this question as Spreedly's dataset continues to grow.

The data in Figure 3 suggests two potential action items. First, subscription businesses, particularly venture funded startups and public companies, should consider seasonal and/or monthly adjustments to their churn based on the underlying activity of expiring cards. Second, services that proactively work to reduce churn should consider allocating resources differently. For example, in the month of March vs. July. Both of these points are particularly true if there is a large percentage of Visa and MasterCard data within your vault.

If you enjoyed this post, please do share it on social media!

Download the Payments Orchestration eBook Below

What percentage of credit cards stored in Spreedly's vault are Visa cards?

Visa cards comprise 63% of credit cards stored in Spreedly's vault, making it the dominant card type.

Why is understanding credit card expiration important for subscription-based companies?

Expiring cards are a major driver of revenue churn and customer support/sales costs. Understanding how cards expire helps merchants design for renewal success from day one and reduces the need to chase down customers for updated card information.

How fresh is the batch of cards currently stored in Spreedly's vault?

Approximately 70% of all cards stored in Spreedly's vault have been added in just the last 12 months, representing a relatively fresh batch of cards, though imports from other payment providers may include cards of unknown age.