.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Your payments stack almost certainly uses both encryption and tokenization already, possibly without anyone having made a deliberate decision about which does what. That's more common than you'd think, and it's not necessarily a problem, but it does mean you're probably not getting full value from either.

Encryption and tokenization protect payment data in fundamentally different ways, apply to different points in the transaction lifecycle, and carry very different implications for your PCI DSS compliance scope and the annual audit overhead that makes grown engineers briefly consider whether goat farming might suit them after all.

Knowing which tool belongs where is how you build a payments security architecture that holds up, rather than one that passes the questionnaire and quietly sweats the rest of the time.

What is tokenization of data?

Tokenization of data is the process of replacing a sensitive value with a non-sensitive substitute, called a token, that has no exploitable value outside the system that issued it. In payments, the sensitive value being replaced is the primary account number on a card, the PAN, a 16-digit string that has caused more security team insomnia than any other piece of data in modern commerce.

The token that replaces it has no mathematical relationship to the original. It isn't derived from the card number, doesn't contain any portion of it, and cannot be reverse-engineered by anyone who finds it, including people who are very motivated and have a great deal of time on their hands. It's a reference, not a record, the way a claim ticket at the DMV is a reference to your actual driver's license and not, in any meaningful sense, a document you could use to drive home. The actual card number stays in a secure vault. Your systems work entirely with the token. Everyone sleeps better, and significantly fewer people are positioned to ruin your quarter from the outside.

According to Juniper Research, tokenized transaction volumes are on track to surpass one trillion globally by 2026, which is the industry's collective way of saying this approach has been road-tested at extraordinary scale and found worth the trouble.

What is encryption, and what is it actually for?

Encryption transforms data mathematically using an algorithm and a key, producing ciphertext that is unreadable to anyone who doesn't hold the matching decryption key. It is, in the most architectural sense, a very sturdy safe: everything inside is protected, recoverable, and entirely accessible to anyone who walks in with the combination, which is precisely where the long-term storage strategy starts to show its limits.

The protection encryption provides is only as durable as the key management around it. Lose the key to the wrong person and every piece of data it was protecting becomes readable, in full, immediately, because the math runs both directions and has no interest in your feelings about it. This is not a criticism of encryption as a technology. It's a description of what it was built for, which is protecting data while it travels, not while it accumulates years of value as a stationary target.

For data in transit, encryption is the correct tool and PCI DSS makes this non-negotiable. The moment cardholder data crosses a network boundary, encryption is what protects it on that journey. That requirement doesn't change regardless of what else your stack does, and no volume of tokenization substitutes for it. Encryption owns the road. Tokenization, as we'll get to, handles the destination.

Tokenization vs. encryption: the distinction that actually matters

The most useful framing for the difference between these two tools is this: encryption conceals data, and tokenization replaces it. These are not variations on the same strategy. They produce different security profiles, different compliance footprints, and very different outcomes when someone gets into a corner of your infrastructure they were not supposed to visit.

Encrypted cardholder data is still cardholder data under PCI DSS, regardless of how strong the algorithm is or how carefully the keys are managed. The standard doesn't reward elegance. It only asks whether systems in your environment store, process, or transmit cardholder data, and encrypted card data absolutely qualifies.

Every system touching it stays inside your audit scope, which means your compliance perimeter is exactly as large as your data footprint, your questionnaire is exactly as long as it needs to be, and your QSA has a full dance card every year whether you like it or not.

Properly tokenized data is a different conversation. When a token contains no portion of the original PAN and cannot be derived from it through any reversible process, it can fall entirely outside PCI scope.

The systems handling only tokens step out of the most demanding compliance requirements, your audit surface shrinks to match what you actually control, and your engineering team gets to spend less of every year explaining infrastructure that no longer has anything sensitive to account for. PCI certification for large merchants runs between $50,000 and $200,000 before you count the engineering hours and the compliance team overhead. Scope reduction is not a footnote to that number. It's a direct reduction of it.

One clarification for anyone who searched "encryption token" expecting content about cryptographic hardware devices: a hardware encryption token is a physical or software object used in authentication workflows, which is an entirely different concept from a payment token. You've arrived at the right destination by the scenic route, and everything that follows is exactly what you were looking for.

PCI tokenization vs. network tokenization: same name, considerably different results

PCI tokenization and network tokenization both replace a PAN with a token, in the same sense that a studio apartment and a four-bedroom house are both technically places to live. The concept is shared. The experience diverges fairly quickly.

PCI tokenization lives inside a closed ecosystem. A gateway or processor vault issues the token, stores the original PAN internally, and manages the mapping between them. This is a solid compliance solution that delivers exactly what it promises inside its own environment, right up until the moment your business outgrows its original gateway relationship, which businesses do with the kind of reliability that would be admirable in any other context.

The token one gateway issues means absolutely nothing to another, which means every stored credential stays behind in the vault that created it when you want to move, expand, or diversify your acquiring strategy. It's infrastructure that holds your payment data the way a landlord holds a security deposit: technically yours, not quite in your hands, and more complicated to recover than anyone mentioned upfront.

Network tokenization is issued by the card networks themselves, Visa, Mastercard, and American Express, and recognized across the entire acquiring ecosystem. Network tokens are domain-restricted to your specific merchant context, meaning they work at your checkout and nowhere else, which is a deliberate fraud prevention feature rather than a limitation.

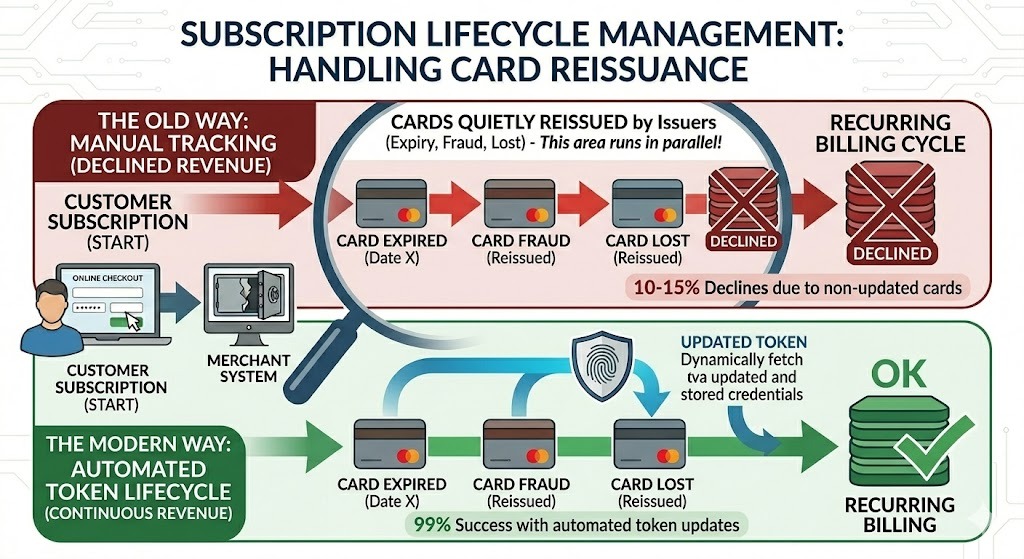

They're lifecycle-managed by the network, so when a card is reissued after expiry or replaced following a fraud event at some entirely unrelated merchant, the token updates automatically. Your customer gets a new card, finds the timing mildly inconvenient, and gets on with their life. Your billing system doesn't notice anything changed, which is the exact outcome you were hoping for and considerably rarer than it should be.

Universal issuer support for network tokens isn't yet complete across every market, which is why a well-designed vault stores network tokens, processor tokens, and vaulted PANs together, routing automatically to the best available credential for each transaction. Spreedly's vault is built exactly this way, so the credential that performs best wins each transaction rather than infrastructure inertia making that decision silently on your behalf.

The authorization rate argument, or: how tokenization pays for itself and then keeps going

Security conversations tend to live in the cost-avoidance column of the budget, which is a respectable neighborhood but rarely generates much enthusiasm in a room full of revenue leaders. The authorization rate argument for network tokenization lives in the revenue column, which is a different room with considerably better coffee.

Visa's 2024 data shows that a 44% year-over-year surge in tokenized transaction volume translated into a 6% improvement in approvals and a 30% reduction in fraud. Visa's card-not-present research documents a 4.6% global authorization rate lift for tokenized transactions compared to PAN-based ones. Mastercard's FY 2025 data, gathered with Checkout.com, shows a 10.3 percentage point increase in approval rates and a 7.2% lift in gross sales revenue for merchants using network tokens. Silverflow's whitepaper, presented at MPE Berlin 2025, puts the authorization improvement at 3 to 6%.

The reason issuers approve more tokenized transactions is structural. When a network token arrives at authorization, it carries credentials the issuer can actually verify: generated by the network itself, tied to a known card, and paired with a transaction-specific cryptogram that only the legitimate party could produce.

A static PAN arriving from the general direction of the internet carries considerably less of that reassurance, and issuers, being cautious institutions that have seen things, respond by declining a meaningful percentage of transactions that were entirely legitimate. On a business processing $10 million per month in card-not-present volume, a 4% authorization rate improvement is $400,000 in monthly revenue that was previously declining without ceremony and without anyone specifically deciding that was acceptable.

For subscription businesses, the lifecycle management calculation runs a parallel track. Every billing cycle, some portion of stored cards have been quietly reissued since the customer first signed up, because cards expire, fraud happens elsewhere, and issuers replace credentials with the cheerful regularity of someone who has never once considered what this does to a recurring billing stack.

Without lifecycle management, your system charges the stale PAN, receives a decline, dispatches a dunning email the customer will read sometime between immediately and never, and watches a subscriber who fully intended to stay become former revenue through no fault of their own or yours.

With network token lifecycle management, the credential updates when the card does, the charge completes, and the subscriber's only experience of your billing infrastructure is the complete absence of any friction whatsoever, which is a customer experience achievement that costs your retention team exactly nothing.

When to use encryption, when to use tokenization, and when to use both

Encryption protects data on the move. Tokenization protects data at rest. These describe different points in the same transaction lifecycle, which means the answer to "which should we use" is almost always "both, assigned correctly."

Data gets encrypted as it travels into your vault, because it is crossing a network and that is what encryption is for. Inside the vault, the original PAN is stored securely and a token is issued in its place, because tokenization is what you use when data needs to live somewhere and be referenced repeatedly without the underlying sensitive value ever touching another system. Every downstream process, your routing logic, your retry workflows, your reporting, works with the token. The PAN stays in the vault like an original document that everyone agrees is important and nobody actually needs to look at on a Tuesday afternoon.

The two tools are complementary, not competitive, and the payments stacks that treat them as such are the ones with the smallest compliance footprints, the strongest issuer relationships, and the least eventful audit seasons.

Spreedly's Advanced Vault is built on this model. It provisions network tokens from Visa, Mastercard, and American Express, stores them alongside processor tokens and vaulted PANs, manages the lifecycle automatically as cards are reissued, and routes to the best available credential for each transaction across 140-plus connected gateways. Performance reporting ties authorization outcomes back to credential type and routing decisions, so the impact of your token strategy shows up in numbers you can bring to a meeting rather than assumptions you have to defend without evidence.

The architecture decision that looks obvious in hindsight

Merchants who treat tokenization and encryption as interchangeable, picking one and hoping it covers both jobs, typically end up with audit scopes larger than necessary, authorization rates lower than achievable, and stored credentials that create friction every time the infrastructure underneath them needs to evolve. Merchants who assign each tool to the right job end up with a tighter compliance footprint, better issuer confidence, and payment credentials that keep working quietly as their provider relationships, regions, and business models change around them.

Building this correctly from the start is considerably less expensive than correcting it later, which is true of most infrastructure decisions and serves as useful context for anyone currently describing their token situation as "good enough for now."

Imagine Your Payment Data Belonging to You, Not Your Processor

Find out how you can gain tokenization independence and take control of your full payments stack.

Download the Tokenization Decision Guide Now >>

What is the main difference between how encryption and tokenization protect sensitive data?

Encryption converts plain text into unreadable cipher text using an algorithm and encryption key, which can only be decoded with a matching decryption key. Tokenization, on the other hand, replaces sensitive data with non-sensitive tokens that have no intrinsic value, while storing the original data securely in a separate token vault.

Does tokenization replace encryption, or do you need both?

You need both, assigned to the right jobs. Encryption protects cardholder data while it travels across networks, and that requirement is non-negotiable under PCI DSS regardless of what else your stack does. Tokenization protects stored credentials at rest, replacing the PAN with a token that your downstream systems can reference without ever touching the underlying card number. The two tools address different points in the same transaction lifecycle and work best when each is doing the job it was built for.

How does tokenization affect PCI DSS compliance scope?

Encrypted cardholder data is still cardholder data under PCI DSS, which keeps every system touching it inside your audit scope. Properly tokenized data, where the token contains no portion of the original PAN and cannot be reverse-engineered, can fall entirely outside PCI scope. This shrinks the environment your auditors need to assess, reduces the engineering overhead required to maintain compliance year over year, and lowers the cost of certification, which for large merchants runs between $50,000 and $200,000 before internal labor is counted.